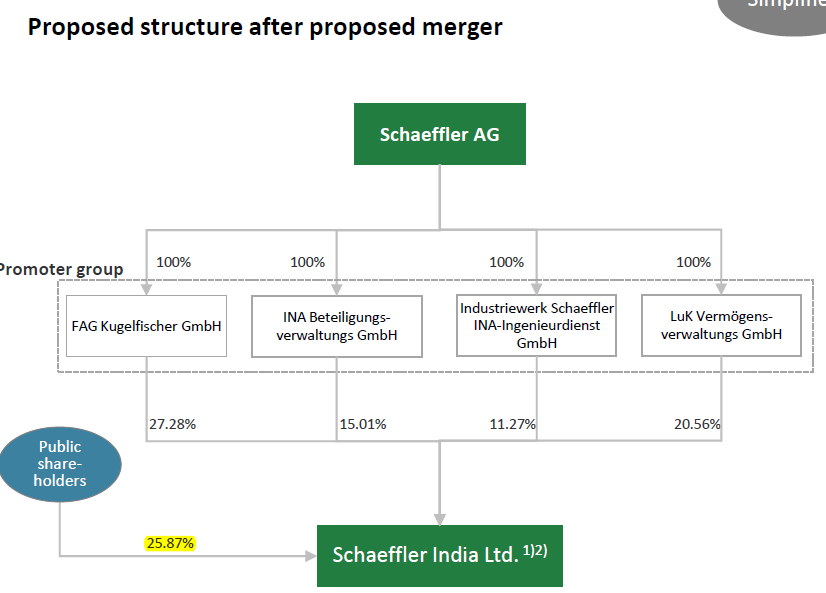

Schaeffler India Ltd is one of the three subsidiaries of its German parent Schaeffler AG. The other two ( INA Bearings Pvt Ltd & Luk India Pvt Ltd are unlisted ).

As part of its “One Schaeffler India” plan - it recently proposed to merge the 2 unlisted entities into the listed one ( Schaeffler India). It has put out an investor presentation giving out the details which can be found here

The Schaeffler subsidiaries in India are well known and supply bearings & other auto components to the who’s who of the Indian auto industry.

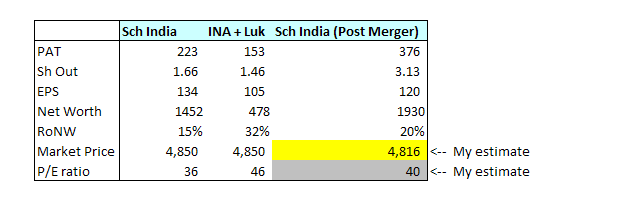

The return on net worth of the listed entity (Schaeffler India) is b/w 13%-14%. Post merger the workout i have done suggests that not only the RONW will increase to 18%+ but the growth rate of the combined entity will also increase significantly and will probably be between 15% to 17% from the current 7% to 8%.

The reason being that the other two unlisted companies are growing at a rate that is much faster and have a better high value product mix. Of particular note is INA bearings which has a lucrative RONW of 34% based on CY16 numbers and Luk India with a RONW of 22% is also doing quite well. These are industry leading numbers & both are very well run & managed companies.

Timken recently announced a purchase of ABC bearings at an earnings multiple of ~45 ( based on current Timken prices 25/09/2017 & ABC EPS as on March 17) - ABC bearings has RONW of 8%. It stands to reason that the earnings multiple of both Luk & INA should be better than 45 given superior return ratios & for that matter even Schaeffler at RONW 13% should be higher )

Post the merger the revenue mix will change significantly & new look Schaeffler India which was earlier having a revenue supplying bearings mainly to the industrial sector will now have a new & improved mix where 55%+ will come from the automobile sector. All the revenue mix details can be found in the investor presentation. However , based on the current financial statements, 53% of the operating profit will come from Sch India, 27% from INA and 20% from Luk.

The number of shares post merger will increase to 31,260,734 from 16,617,270. The details of the share distribution can be found here

A linear calculation produced a EPS of Rs 121 per share ( CY17) post dilution from the current 134 per share however, post the merger, the debt in INA bearings & Luk will be retired from the cash rich Schaeffler India & will add Rs 5-6 per share. INA bearings has a total debt of 185.4cr & Luk has a total of 34.4cr. The total cash reserves of the combined enitity are 793 cr.

I expected the blended PE multiple to be about 46-47 of the combined entity ( given the 52-27-20 mix of Sch India, INA and Luk + based on the valuation paid by Timken for ABC) on an EPS b/w 121 to 130 giving a probable valuation b/w Rs 5566 to Rs 5980 per share. At the CMP of Rs 4810 ( on 25/09) it gives an estimated upside of 20%+

The merger will take 12 mths to conclude. There is a decent 11% arb opportunity in ABC & Timken as well

The workout i have prepared isSchaeffler.xlsx (13.7 KB)

. Data has been sourced from the Sch India investor presentation.

Risks

-

the valuation paid by timken for abc is expensive going by industry reactions. Since the expected value of the merged entity is based on the valuation of abc there is a risk that market will recognize the overvaluation and auto correct to saner levels.

-

The merger may not happen as shareholder & other approvals are still required

Thanks

Bheeshma

Disc invested in the correction today.