AMEX vs SBI is again an apple to orange comparison. AMEX has grown at 7% in the last 10 yrs in both revenue and net profit whereas SBI cards grew at 30%. Hence valuations are not comparable.In future also, SBI cards will grow at a much better rate (not 30% but at least 12%) than AMEX.

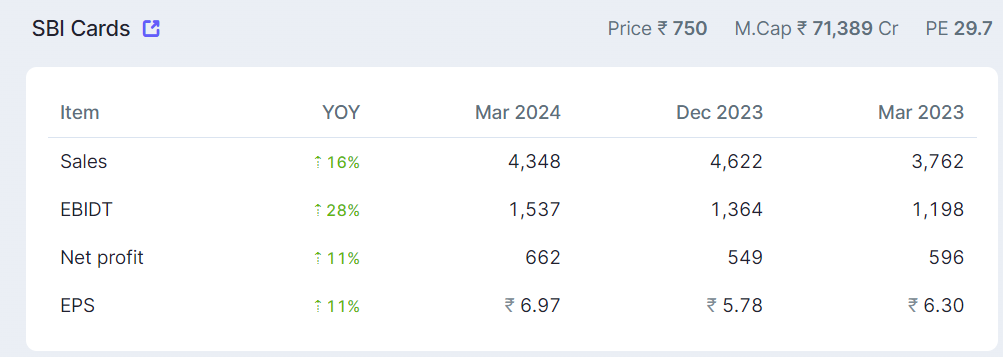

I guess market in in a shock due to reduced profitability and growth in FY24. Hence a PE of 29.

Even if growth is drastically down from here onwards (unlike last 10 yrs), the sustainability/longevity of this nominal growth is the critical factor that will decide returns from current level.

Question is “Does market overestimate the bad news of FY24?”

Amex has completely different model from SBI Cards as the spread is completely different between the two making Amex much more profitable.

Amex has moat through its marketing & customer service due to which customers are very sticky.

Basic issue is currently with the increasing use of UPI we are becoming less reliant on credit cards except for big ticket purchases(ex: TV, Mobile, Refrigerator)

a. Merchant try to charge the discount rate from customer itself when paying from credit card then we pay from any credit card.

Any credit card makes money

With the consumers making more transactions through credit card (industry standard discount rate is 1% while for Amex it is 3%)

AMC charges which is quite low in case of SBI Card

Being a business owner (father one) we need to pay some charges over 2000 payment via upi based credit card and at least in Paytm and Phone pay have an option.

90% shopkeepers don’t enable it and I think most money from transactions can be earn using it.

So if UPI stays a big transaction then most card company will not earn much as their main business of transaction money is gone so main money from loans and annual fees only.

Will say it’s still a evolving story so how it shape out is a blurry picture.

Main bear story atleast for mid to short term for cards is UPI plays may be totally not accounted so will it benefits (i will say yes) , second is credit cost at least in mid term would be high and that will result in less profit growth rate.

Even if the card space is good but SBI cards is not the best bet overalls it’s just the only bet we can take directly as the growth and aggression is the least in all of them.

One big investor problem is that finance has to many problem right now and is actually a sector that no matter how fast it grow will not be rewarded as the picture in future is not that clear at least in mid term basis

I think its a mixed bag. While revenues and profit increased some key metrics are in a downtrend

GNPA up 12 bps at 2.76% (QoQ)

NNPA up 2 bps at 0.99% (QoQ)

Expenses surged 15% YoY to Rs 3,586.41 crore. Of these, finance costs rose the most by 42.6% year-on-year to Rs 723.8 crore

Gross credit cost for Q4 stood at 7.6%, up 7 bps quarter-on-quarter and this is expected to remain elevated in the future as well, at about 7% for FY25

Also a big increase of 50% in impairment losses and bad debts expenses of ₹944 crore in Q4 FY24 compared to ₹630 crore in Q4 FY23

Did Credit cards loose its shine upon arrival of Google Pay etc? No company is offering freebies etc … Some kind of incentives used to be there for CC purchases… Its better to invest in SBIN than SBI Cards .

I am holding SBI Cards however never made profit yet… I will sell off once it reaches 850 - 950 levels

Hi guys, I’m studying this company and wanted to understand the role of interest rate cuts on credit card companies.

If repo rates are cut, will the finance cost decrease? How will the cost change considering NCD, etc will also have change in their interest rates.

If cost of borrowing decreases, will they be forced to lower their interest rates which they charge as well?

Another question I’ve is regarding cashback. How does one make money in such scenarios? Are the cashback cost bore by the credit card or by the seller? Or it’s just a tactics?

Interest rate on a credit card does not decrease irrespective of repo rate. So yes, their NIM will increase by a few points. Although it will be a small increase as the spread is already very high.

Credit card companies bear the cost of cashbacks. They earn from these ways:

a. Merchant fees

b. Interest from consumers who default or do minimum payment.

c. This is slightly newer for Indian cc ecosystem. No cost emi. In this scenario, interest on emi is paid by the merchant.

I see credit cards going very big in India. Literally everyone I know (salaried, 25) in my circle is having 3 or more cards. And always applying for more. Now how will SBI Cards hold up is a different matter.

Merchant is not the bank. It is the entity client purchases product from. For example if I purchase Iphone 15 using sbi card from amazon using no cost emi, the emi will be borne by the distributor selling iphone 15 on amazon.

What is the interest rate on that emi and this interest rate policy is same for other buy now pay later options are this cost is only charged my credit card companies

I am not aware of the specifics. But I know one instance. Bought a macbook air on no cost emi of 9 months. The interest rate is being shown as 15%.

The typical interest rate on normal credit card dues are 25-40%. So if I would have to guess, I would say IR on no cost emi is much lower.