This company which used to be a BIFR case has recently become debt free**.

Capacity 1.5 Mtpa (expandable to 3 Mtpa at low cost of Rs 250 Crore)

Enough limestone reserves for next 40-50 years.

Located close to Porbander port (exports 30%)

Can import coal or petcoke when required.

FY 2014-15 highlights

Revenue 570 Crores

PBT Rs 48 Crores, before exceptional items

Depreciation 35 crores

Long term debt zero.

Short term debt 4.4 crores

Receivables 19.3 crores

NCA -15 crore.

Market cap Rs 342 crores (at CMP of Rs 64)

Market cap Rs 442 crores (at CMP of Rs 64) after promoters bring in additional Rs 18 Crore at par as per BIFR order.

**Debt of Rs 392 crores in 2006, now zero. Plus over 2006 to 2014 they paid cumulative interest of Rs 304 crores. With zero debt status, cash flow to equity will be very high.

Disclaimer: As on date of writing this I own this scrip and may trade, get in or out anytime. I am not making any recommendation to buy or sell this stock.

Your disclosures are non-conducive. You need to mention whether you hold that stock as on the date of starting the thread. Please edit and make clear disclosure.

It looks very interesting to me as the downside seems to be limited with good possible upside. But I found that the promoters had some issue related to non disclosure in the past and there was some SEBI action on them. In any case I have taken a small position in it considering that the price seems to be very low compared to the cash flow etc.

Thanks Keshav. I had read this yesterday and was not fully convinced with the negatives mentioned in it.

Company is very small and won’t be of interest to fund managers - True. that’s why the company may be cheap compared to the intrinsic value. I am not sure if that’s really a negative for the buyer.

2.The management is not aggressive as it didn’t expand the capacity or sell it in the past many years - The company was in trouble for last many years due to the large debt they had taken trying to expand at a wrong time. So I am not surprised that they were very careful. Now that they are debt free, I hope they will do something as they hold majority share holding. I think selling it now will not be a big problem considering the major battle that happened for its ownership many years back.

Looks very interesting. Trades at EV/ton of US$40. An year or so back Orient Cement was a in similar position post demerger @ Rs40 levels at similar valuations. Today stock is at Rs154 supposedly after Rakesh Jhunjhunwala bought it and others noticed it. The only difference is Orient Cement has much higher capacity.

2QFY16 debt has gone to zero. Hopefully the pledges will unwind in the near future. That should be a trigger for the stock.

@utkarshpatel. Can you please highlight the warrant bit. I cant see it in the annual report. Who has these warrants and what are the details. I see optionally convertible preference shares. I don’t see warrants.

Here are the details below. Extract from FY15 annual report

The Company has only one class of preference shares referred to as 13% Optionally Convertible Cumulative Preference Shares (OCCPS) having a par value of `100. These preference shares do not carry any voting right. However, as per the provisions of the Companies Act, 2013, if the dividend on such preference shares has not been paid for a period of two years or more, the holders of such preference shares shall have a right to vote on all resolutions placed before the Company.

OCCPS carried a fixed cumulative dividend of 13% p.a. from the date of issue. The holders of OCCPS carry a right to dividend ahead of equity share holders.

In the event of liquidation, the holders of OCCPS carry preference over equity shareholders in respect of repayment of capital.

OCCPS were redeemable at par on March 31, 2003.

**Of the total Preference Share Capital of Rs687.60 lacs,the holders of 1,74,557 OCCPS of ` 100 par value, aggregating to Rs174.56 lacs, have surrendered their right in the redemption, including the preference dividend thereon for the benefit of the Company. Based on the advise received, pending the availability of funds / distributable profits for the redemption of capital, the beneficial ownership of these OCCPS has already been transferred in favour of a trust of which the Company is the beneficiary. The accounting effect of such waiver (only in respect of these OCCPS) shall be made as and when such shares will be redeemed.

For the balance of OCCPS, the right of conversion lapsed on August 22, 2003.

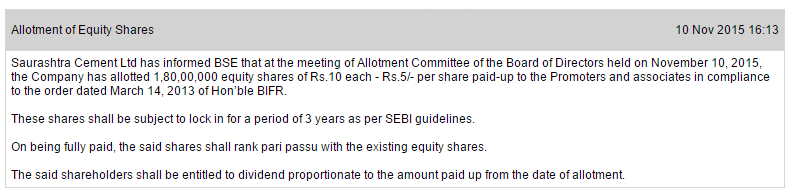

Not exactly warrants, these are new shares alloted to the promoters of the company.

Post the lock in period, shareholding of promoters would increase from 64.63% to 73.83%.

@utkarshpatel

But this will infuse cash into the company right? That will reduce the net debt (rather increase net cash). That will decrease EV = market cap + net debt. So EV/ton should fall even lower rather than increase?

And yes promoters increasing stake in company is +ve confidence booster. Yes minorities get diluted as this is done at a lower than market price. But this was mandated according to BIFR in Mar 2013

As per my interpretation, Cash infusion would be limited to ~9 cr (Rs 5 per share) compared to market cap of 500 cr.

Hence, it won’t have much impact on the EV.

Hi buddy , thanks for creating this topic … Saurashtra cements came up with rocking results esp yoy and not to miss , qoq … Though operating profit is a concern just for qoq , it is washed out when we consider the consolidated results . Any idea how this would be from a fresh entry perspective , provided that Industry pe is 37 and stock pe is 7 , making it once again a highly attractive bet … shp is also kool thing .

Trying to revive this old thread. This looks like the cheapest cement company out there. The profitability too seems to have improved drastically in the recent quarters. Any thoughts on the current valuations?

Mehta group has merged Gujarat Sidhee and Saurashtra Cements.

Company is now sitting on Net Cash and FY24 should be strong YOY given power cost (50% of revenues) has come down relatively.

Concerns around promoter continuity is still there specially because MS Gilotra has been gradually selling his shares in the last 2 weeks.

can this become an acquisition candidate?