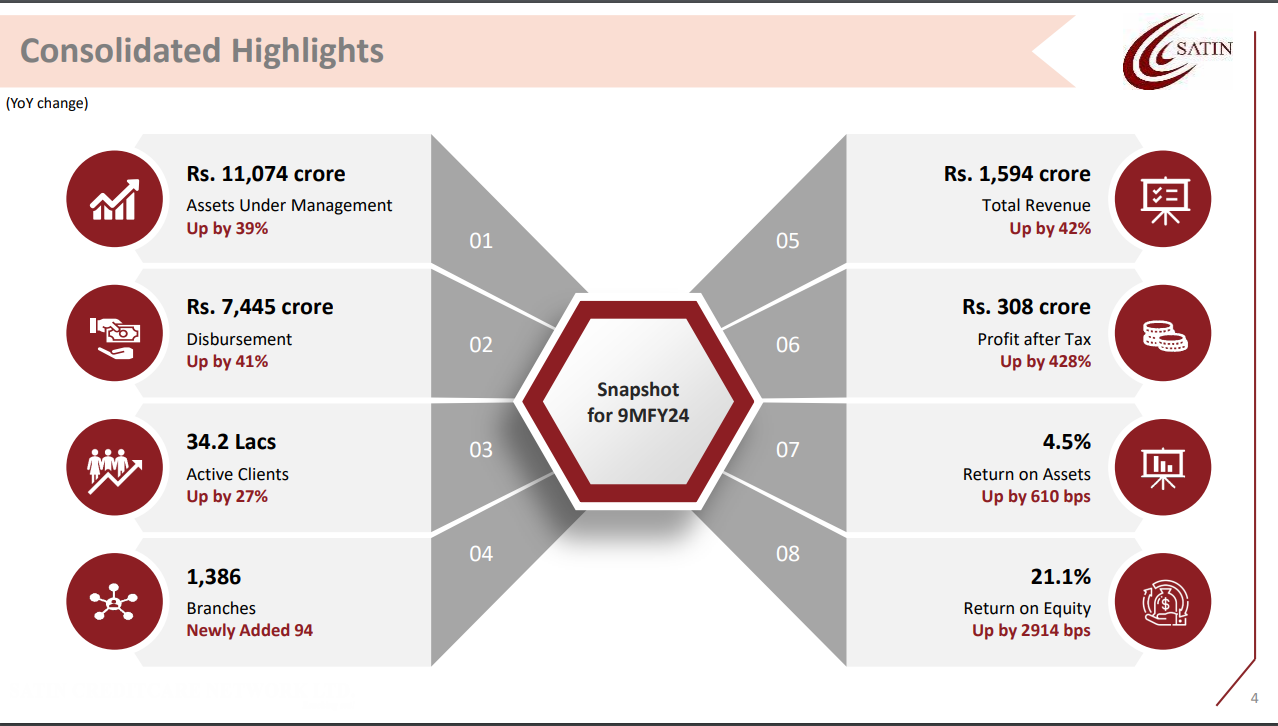

Satin came out with banger Q3 numbers, with RoA and RoE at 4.5% and 21%, a few more quarters of sustained profitability should help re-rate the stock to a minimum of 1.5-2x book (current BV is 205/sh)

Impressed with the management as they cleaned up the book and now are at historic profitability metrics, they not only delivered the projections before FY24 ended.

Invested and biased