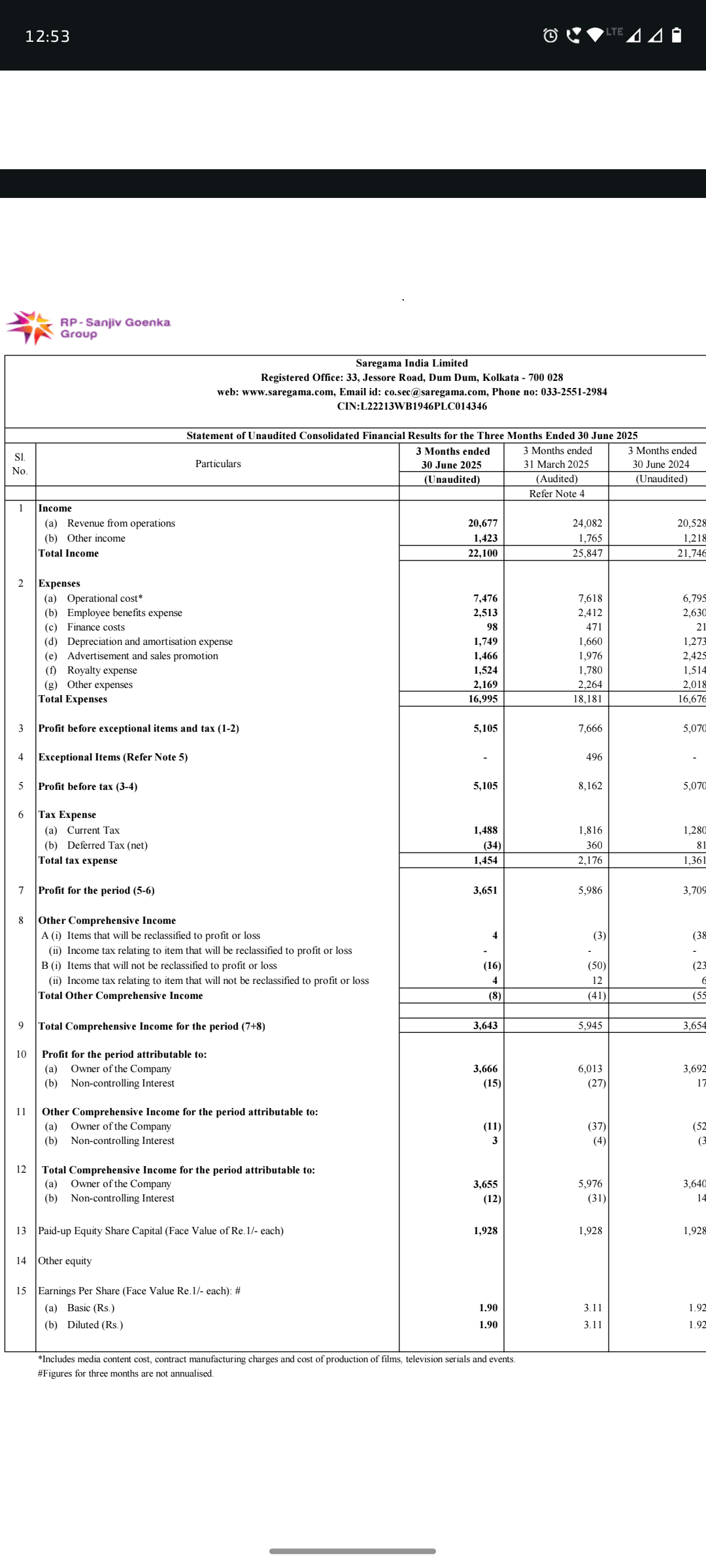

Q1FY26

Sales flat, profit flat ![]()

Heard earning call. Vikram Mehra was more interested in tellling investors how to think long term rather than explaining why most of the numbers were flat.

12 month rolling basis view and timing of last year Q1 being good and this year Q1 not being good was the reason for flat performance.

Also four major free streaming platforms in India including Wynk (Airtel) shutdown was the reason.

i think in heydays of music streaming and video streaming, numbers coming flat is big issue which management was covering by exuding confidence in the earnings call.

Revenue for whole year is projected to grow at 22-25%

Other points mentioned

- Music Vertical (Licensing and Artist Management): This grew 12% year-over-year, but Mehra noted it was impacted by:

- Postponement of major movie releases, which delayed associated music albums. He contrasted this with the prior year’s Q1, which had hits like Tauba Tauba, Chamkila, and Kalki. Upcoming releases Love and War, Dhurandhar and are slated for Q3/Q4, suggesting a back-loaded year.

- Lingering effects from Airtel Wynk’s shutdown (November 2023), which shifted users from free to paid models. This “cycle” is expected to normalize by mid-Q3.

- Temporary YouTube ad revenue dips due to reduced spending during the India-Pakistan tensions in May, though it normalized by June. He emphasized that Q1 is typically weaker for YouTube ads due to IPL competition on TV.Despite this, guidance remains optimistic: 22-23% annual growth in music on a medium-term basis, with new content spend of ₹350-380 crore and a 5-year payback period for investments.

- Video Vertical: This was described as a “softer quarter” with a small loss from one Malayalam film release and a digital series. Mehra explained the cautious approach—capping capital employed at 18% of total—to avoid big swings. He projected full-year profitability, driven by upcoming titles, but acknowledged it’s still an experimental area with limited management bandwidth.

- Live Events and Retail (Carvaan): The new Capmania tour with Himesh Reshammiya started with initial losses due to high upfront marketing, but is expected to turn profitable as it expands. Carvaan retail strategy was streamlined (team cut from 150 to ~20), leading to lower volumes but improving margins toward mid-single digits by year-end.

- Overall Company Guidance: Adjusted EBITDA is maintained at 32-33%, with confidence in steady medium- to long-term growth fueled by India’s digital consumption boom (400 million internet users) and Saregama’s cash reserves.

1 Like