Strong outlook:

a. Revenue and margin: Overall company level, revenue to grow upwards of 30% (exc. Carvaan) in FY25. Revenue to grow at 25-26% CAGR for next 3-5 years. Music licensing shall grow in 30% range. Music+Artist management revenue to cross 1,000 crores from 540 in next 3.5 years.

Adj. EBITDA at 32-33% to be maintained for next 3-4 years. This guidance does not include paid subscribers growth, that will be upside if it takes up.

b. Music content cost: 1000 crore will be invested in new content for next 3 years (includes marketing money). Will be funded internally (QIP money raised in 2021).

c. Carvaan to turn profitable – single digit mid-level profits

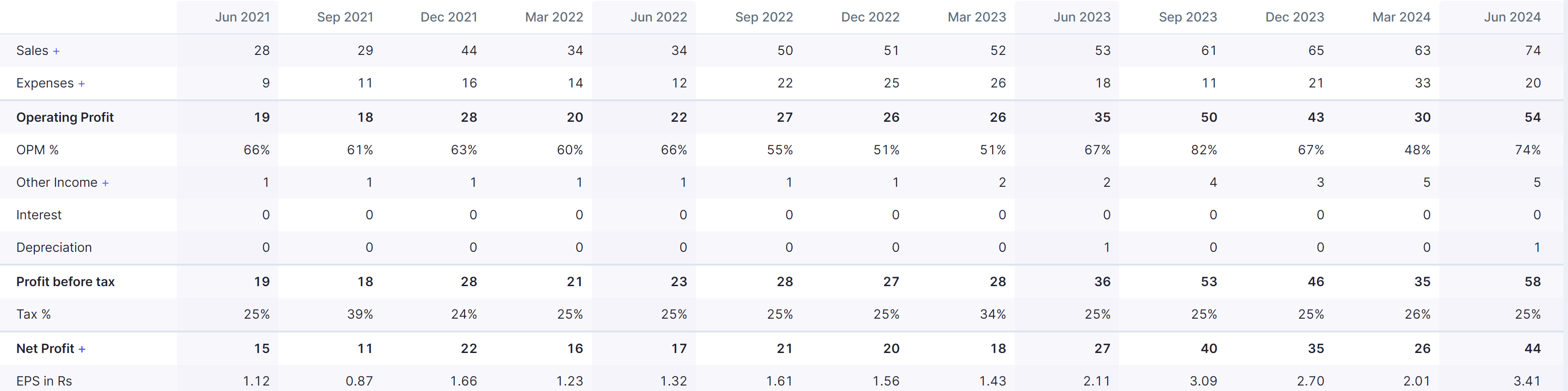

d. Video – Pocket access to grow at 25% cagr. Was loss making when acquired, in FY25 to it will break-even. Cost structure synergies, no synergy on topline.

e. PBT will double in 3 to 3.5 years.

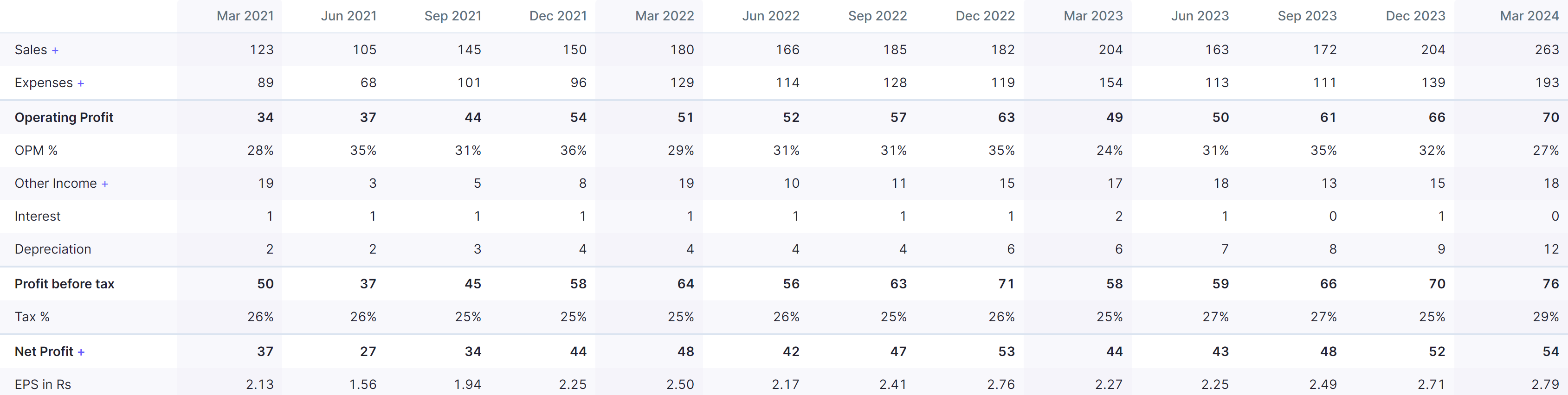

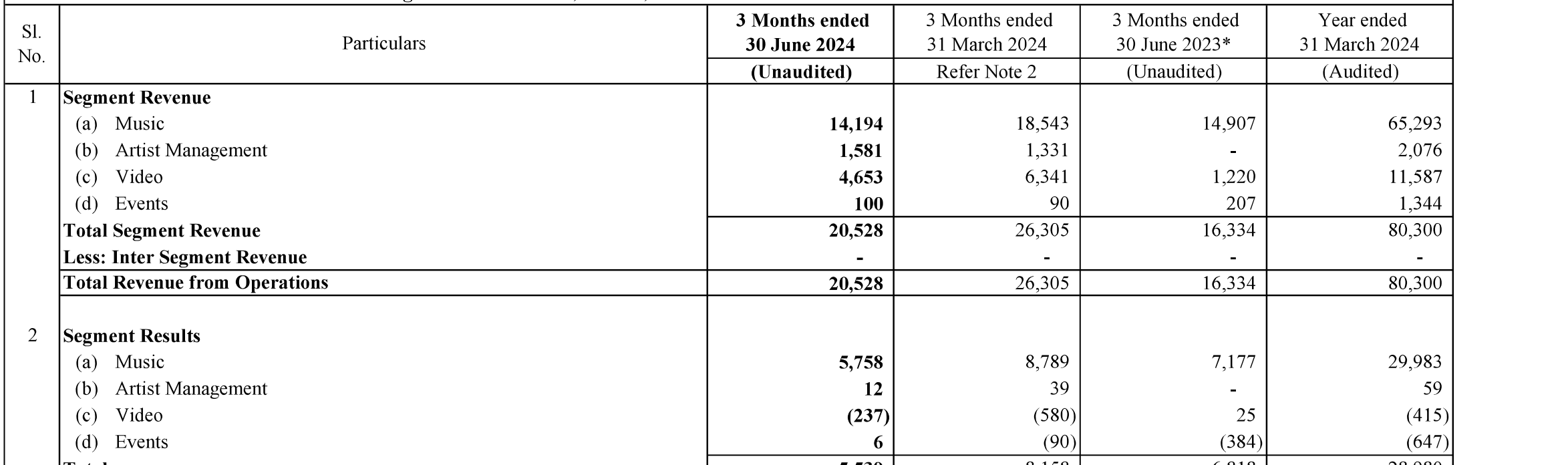

Revenue break-up FY24: Music licensing and AM: 544 crores, carvaan: 130 crores, video (pocket aces): 116 crore, events: 13 crores.

Monetising artists also. Precondition for long-term contract.

Music: OTT revenue negatively impacted by MG going away. This was offset by youtube and artist management.

Charge of content 37% YoY.

New investment in music content 200 crore in FY24 (80% jump vs. FY23). Intensive investment in new content.

Content charge off will grow linearly going forward. So bottom-line will grow much faster after 18-24 months.

Catalogue may grow in 16-18% range post pay (subscribtion) mode.

Filter copy hit 1.2 billion views in FY24. To benefit from advertising growth.

Audio and Video gives negotiation power.

Need one more year for live events to take call on it.

AI music learning app, changes will be made if required.

Carvaan flattish revenue, taking away on-store resence of emlpoyees (not very sure on this part). Single digit mi-level profitability in carvaan targeted.

From Q2, shall be back to old rates in OTT.

In Q4/Q125 election impacted youtube advertising due to political campaigning.

Music licensing revenue: Management: There is no one-off (no overflows).

A&P cost (17-18 past run rate to 27 crores+ from now on) increased due to newer content and marketing related to that.

Artist management: pre-condition to artist for a long-term contract.

Netflix vs. theatrical: cost is lower in OTT vs. Theatrical (also count of screens taken into account). Chamkila example.

513 crores intangible assets on balance sheet: goodwill 300 crore+ due to pocket aces. Liability increases due to commitment. 100 crores for music.

New trend in USA: Gen G. 9 different LPsby Saregama so in line with global trends. Remains on top of whats happening across markets.

Any film right re-sold: 3 movie licensed to second platform. That time making 1-2 crore movies so re-sell will not have much impact.

Shift to paid from free: Saregama paid non-youtube subscription in India % grown by 40% in FY24. Now revenue for Saregama touched in double digit in crores.

Charge off policy: life of content is 10-years. Marketing (~20%) gets charged immediately, remaining 80% - FY-20%, SY-15%, remaining spread over remaining years.

Strategy for pocket aces: advertising moentisation. Digital advertising is huge growth factor. It chases eye-balls. Use both pocket aces and Saregama for negotiations. Use Saregama song through influencer. Use filter copy to advertise, product/services company don’t need to make separate ad for brands.

Paying subscribers were 25lakh (bundled by telco also). 125 million cable and dth paying so paid subscriber is good. Within 3-year 50-75 million paid subscribers possible for industry – need to confirm this data.

New content making money that’s why making profits. Payback period is 5 years. Last 4 years doing better.

Discloure: own around 3.5% of portfolio. Bought today in personal portfolio.

Disclaimer:I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation . Also note that I recently joined a investment advisory firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.

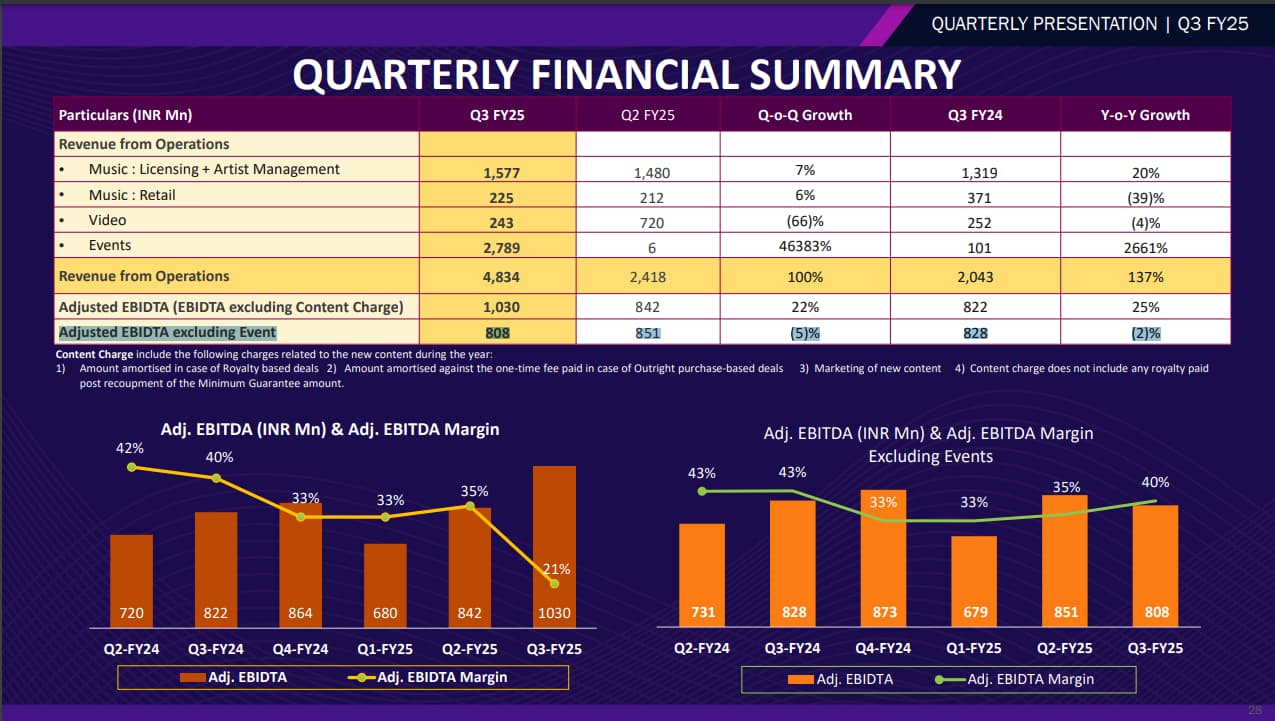

Even the impact of elections is there for other company as well, dont know if the execution is something lagging. the maring is at 25 % down from 37 % YoY.

This will hit bad if the results are in similar way going forward, wating for insights from concall. Also Stock is trading at 52 P/E and ROE at 14 and ROCE is at 19.

Why he has been saying that they are using predictive model to select songs than ear.

And AI to select songs, doesn’t this seems too fairy to hear. Adding AI and predictive modelling so that it feels so tech savvy. This kind of things make you feel that you are pitching things to please investors.

Many business are using predictive AI . It’s not like it’s a very new phenomenon what earlier used to be various data models , machine learning algorithms etc. now it’s predictive AI.

Predictive AI is not some hi-fi thing it’s very basic nowadays. So, very well they could be using it extensively. So i don’t see what wrong in using the term.

I have a sense that the management is attempting to provide an optimistic commentary, but the reality is that they themselves are uncertain whether their ₹1000 crore investment will actually yield positive results. Ultimately, these investments are all risks.in an entertainment industry

Perhaps the right way to look is to see the Music Licensing revenue growth - everything else including video, live events etc. are very low value components and just noise IMO.

Live events may be low value and also low margin but looking at the trend (Diljit and recent Coldplay), this may turn out to be a good segment albeit low margin.

With Diljit Dosanjh’s “Dil-Luminati” tour selling out within minutes, backed by Ripple Effect Studios (organizer) and Saregama India (label/partner), how do you think the revenue-sharing model is structured between the artist, promoter, and label in such large-scale global tours?

Key questions on my mind:

Does Diljit take a fixed fee, a share of ticket sales, or a combination of both?

How does Ripple secure profits after covering massive tour logistics?

What’s Saregama’s angle — direct revenue from the tour itself, or indirect gains through catalog streaming and sponsorships?

As Saregama is primarily a music rights and content company, I’m curious how they monetize such tours.

Potential drivers could be:

Increased streaming and catalog plays (especially Diljit’s tracks they own)

Exclusive rights to live recordings, documentaries, or behind-the-scenes content

Brand partnerships and sponsorship integrations tied to the tour

Long-term brand positioning as a player in live events, beyond just recorded music

Given that most operational costs sit with Ripple, is this a material revenue opportunity for Saregama, or more of a strategic brand and artist relationship play to strengthen their music IP over time?

Would love insights from anyone tracking Saregama’s evolving business model and the broader economics of global music tours.

In the recent concall the CEO was bullish on the event segment (as in the industry too) but not very margin lucrative. As per him even if this segment (which is very miniscule aat the moment but showed massive growth in the kitty much due to Diljit concert) grows going ahead, it’ll be diluting margins on blended basis.

IMO, this is a trend and may generate decent revenue going forward. TIPS did also sound postitve about it in their concall.

Theme park is also gathering steam (Discretionary spending would improve going forward,though subdued in near term).

Big update - Saregama India Ltd acquired a massive Haryanvi music catalogue (6,500+ tracks) from NAV Records Pvt. Ltd. This includes popular Punjabi, Ghazals, Devotional, and Indie Pop music as well. The deal also encompasses popular YouTube channels with over 24M subscribers, strengthening Saregama’s digital presence. This acquisition positions Saregama as the leader in Haryanvi music. Finally… big music acquisitions taking place!