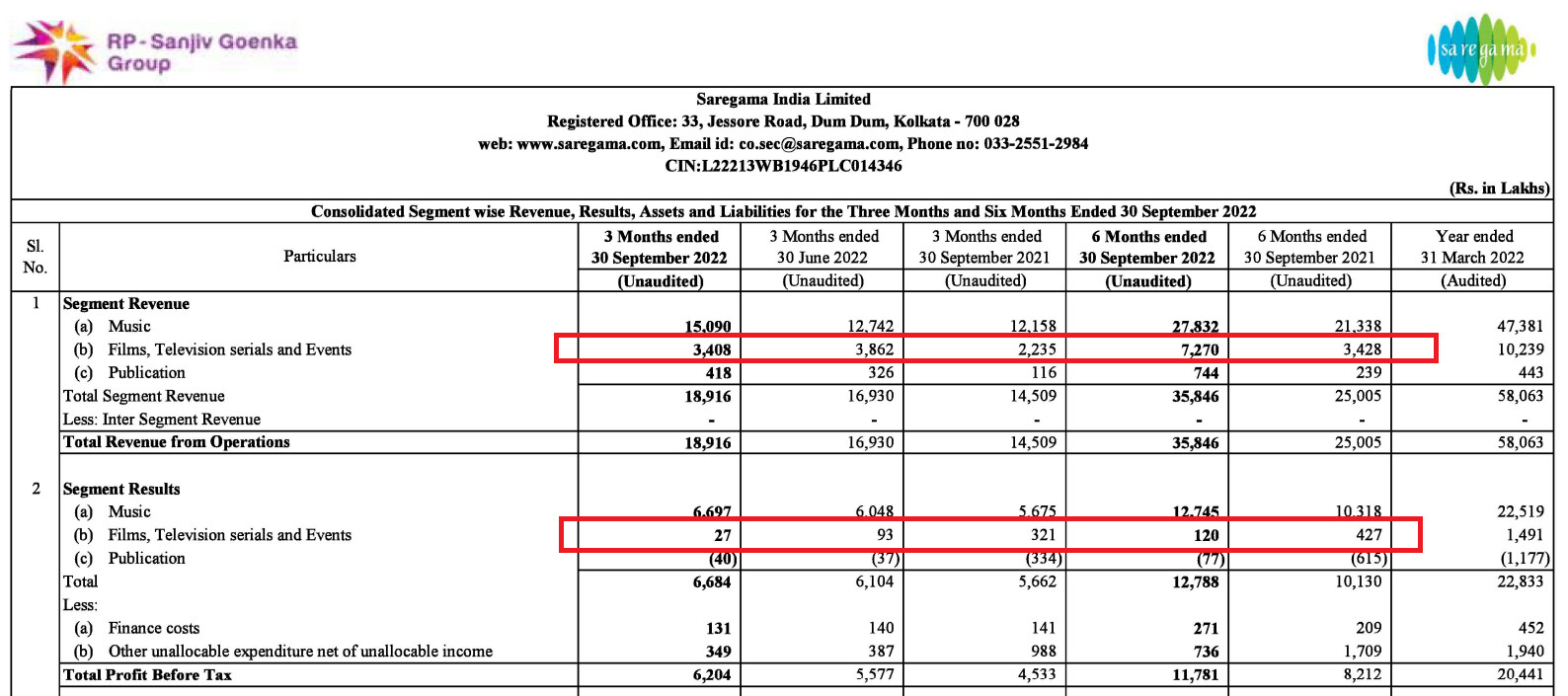

Profitability of the films and web-series vertical (Segment EBIT margin) has dropped steeply in H1 FY23 compared to H1 FY22. It is probably related to timing issues but worth asking Management about in the concall

Overall, judging by the Q results of Netflix, Spotify and now Saregama doesn’t look like OTT consumption of media has taken a hit yet, although YouTube’s ad revenue has fallen a bit QoQ and YoY. Many had feared that recession fears and the end of WFH will cause significant reduction in OTT consumption. This remains a data point to be monitored in the upcoming Qs.

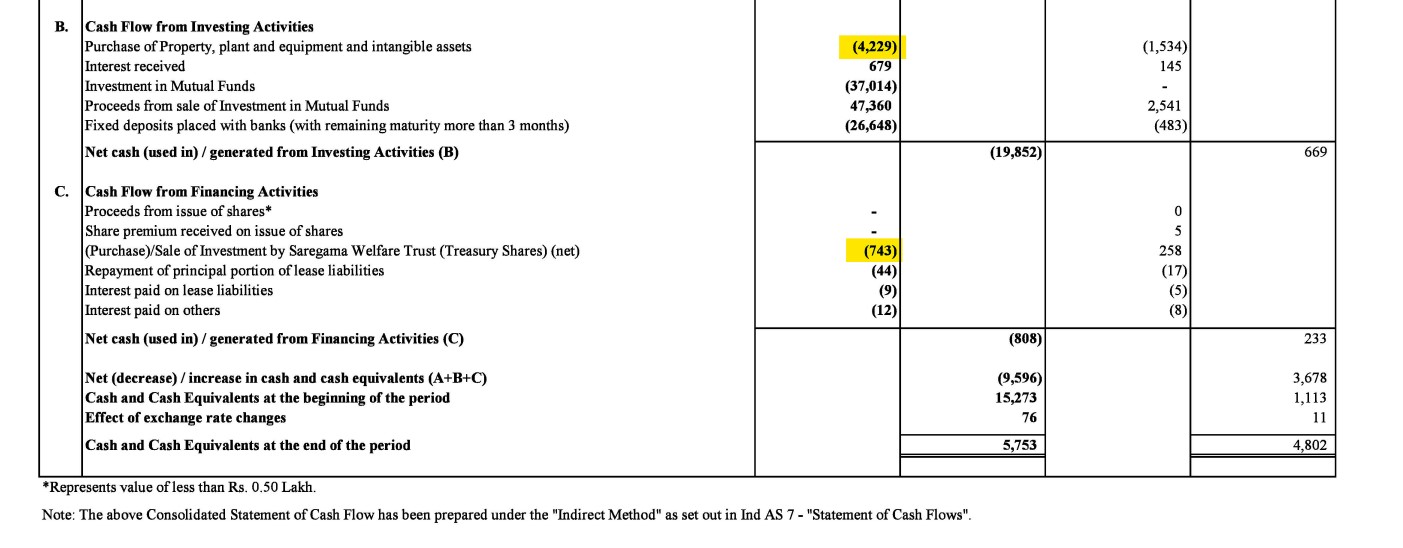

Investment in Property,Plant & Equipment and Intangibles @ 42.3cr

Investment in Saregama Trust @ 7.4cr

Total of above @ 49.7cr (Spent on low ROI assets)

Quarterly PAT @ 46.1cr (a little more than entire quarters PAT gone on unproductive Investments)

How did you deduce the 42 crore as low RoI assets? It says ‘P,P,E & Intangible assets’, where would they show their investment in new music catalogue otherwise?

I actually see it as investment in ‘New music catalogue’.

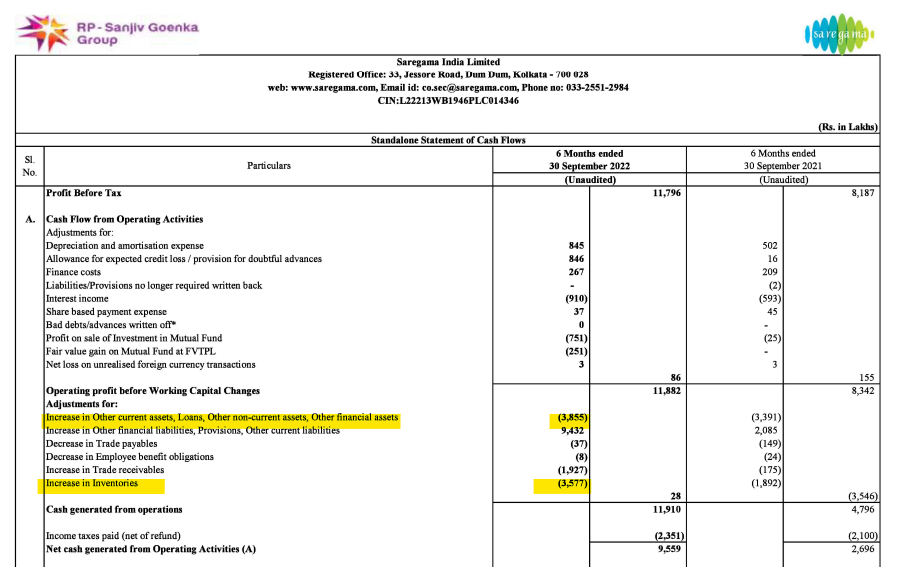

Any addition in music catalogue would be under Cash flow from operations- under the head changes in inventory.

Investments under “Investing activities” are supposed to be non-Operational investments.

This could be an intangible- The Investor presentation doesnt talk about any acquisition hence assumed theres no deal/takeover that accounts for intangibles.

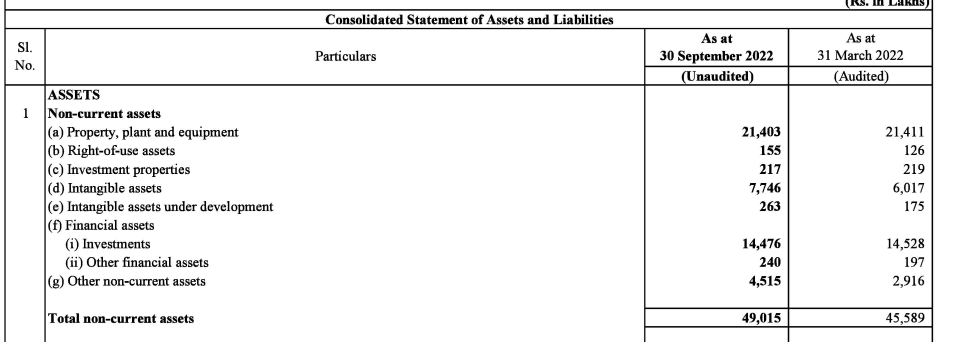

I am looking at non-current assets only, total increase is 35 crores, intangibles (mainly music rights) increased by 18 crores.

Increase in Other non-current assets is 16 crores, significantly higher than March 2022 but total no. of 45 crores is still not very high compared to total non-current assets base of 490 crores. But I guess it doesn’t hurt to ask the reason for this increase.

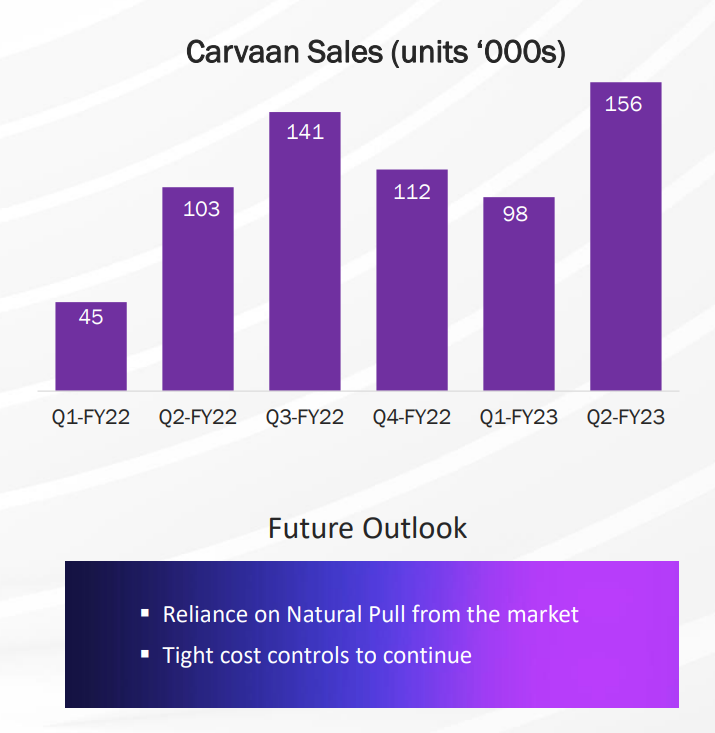

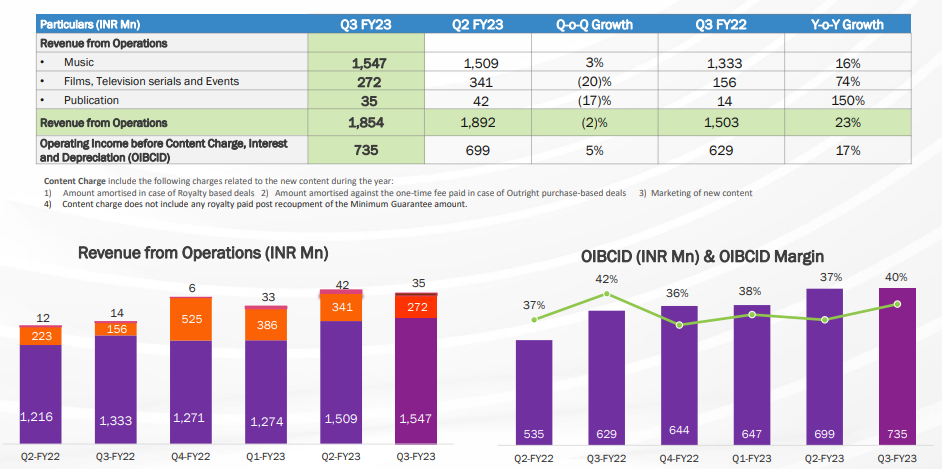

Music Licensing business has again grown at a rate of more than 20%. ASP of Carvaan has fallen thus previous ASP not valid for computation.

Very big Quarter for Bhojpuri Division of Saregama, 2 massive hits this Quarter.

Regional music like Bengali, Gujrati, Punjabi, Bhojpuri- all 3 have done well.

Announced a long term tie up with Arjit Singh this Q.

On QIP Money: only acquired Mango music catalogue. Money kept aside for inorganic purchases, This capital will only be used for the music business.

Many of the films for which they have acquired music will start going live in Q4 this year, and spill over to Q1 & Q2 next year. (Rocky rani Karan Johar etc etc). This is the lag between content acquisition and release.

Carvaan had an upswing this Quarter, latest variant is carvaan mobile. Which replaced Carvaan go. Price point is at 2000-2500rs. 50% increase in units sold. ASP has fallen here, due to smaller variant products. All sale is through customer pull and no advertisement. Revenue increase isn’t as much as 50% as you need to sell 2-2.5 mobiles to get to 1 carvaan realisations. Not spending at all on Carvaan.

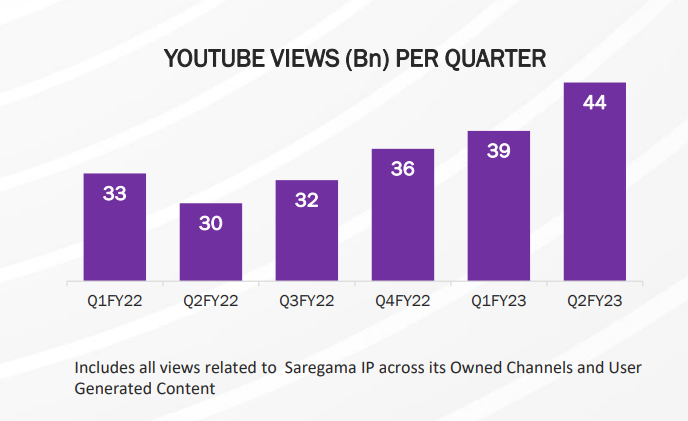

YouTube numbers are globally different vs Indian. YouTube views for Saregama has increased QoQ. Over last 4 Quarters, own channel numbers are growing much faster than user generated content. Views are growing faster than any other label.

YouTube shorts deal was a part of this quarter. (Instagram deal wasn’t- what I understand)

Deals are becoming better, due to better quality of content and newer content. Gives them better position to negotiate.

Got approval for demerger from SEBI and filed in NCLT, will take 4-5 months. Will complete by March 23.

Guidance for 22-25% growth remains in music licensing business. Music business hasn’t experienced any type of slowdown.

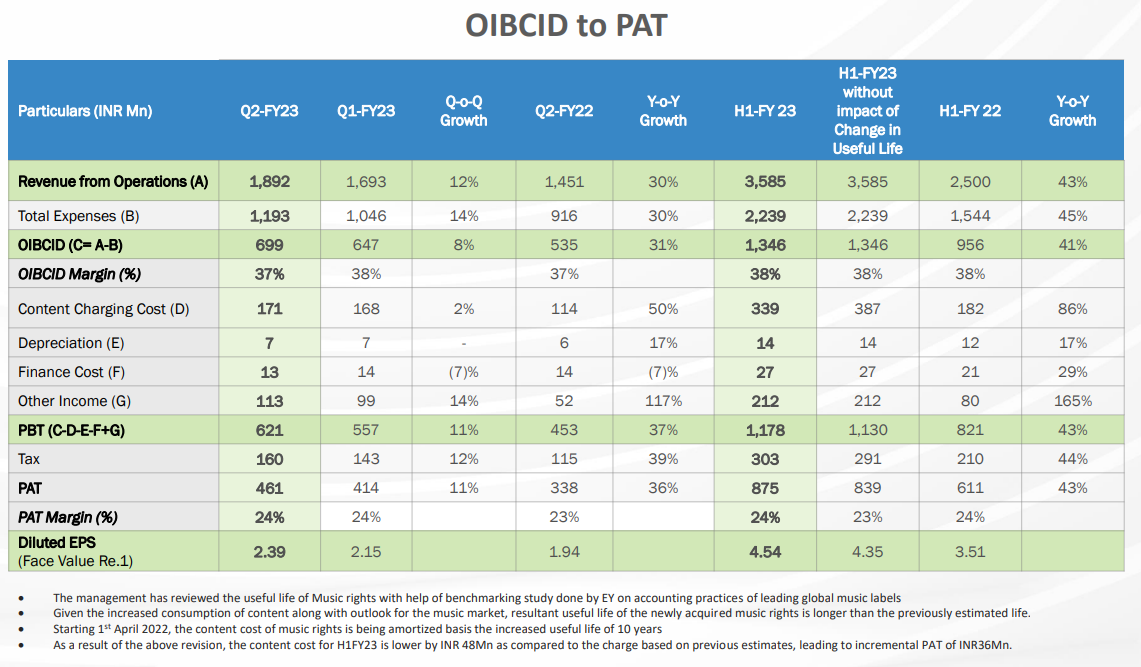

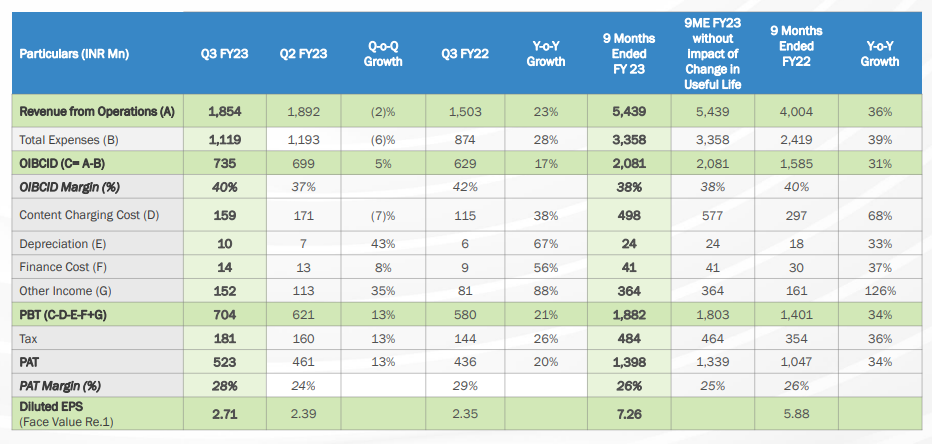

Bonuses to employees are given in Q2. Improved employee expenses to 11% in Q2 vs 13% last year in the same Quarter.

Events business is currently combined with Films & TV. Is a low margin business. This is an essential business to manage to build relationship for music business. eg: Events for Diljit and then doing music with him.

Sticking to 32-33% OIBCID margin guidance. Even though this quarter they have done 37-38% OIBCID margin. Due to event business, possibility of having a large event business of 30-40 crore business coming in. If it was purely music, would have done 37-38%.

Retains growth guidance of 20-25% in the medium and long term for the music licensing business

Disclaimer: invested.Fears of a slowdown have been misguided it seems… Remains one of the cheapest consumer stories… given the margin profile and being a play on the internet growth story.

for every Rs100 change in avg realisation price of carvaan the licensing music revenue growth goes up by 2%.

If the avg realisation for carvaan is Rs2400 then the q-o-q & y-o-y growth for licensing business will be 15% & 23% respectively.

As per my understanding the realisaiton of 2500 is on the higher side. Even at that price the growth rate looks very healthy.

Please note: My assumptions here is that in the last qtr the avg realisation was ~Rs 2850. The whole calculation depends on my assumption.

Heard Saregama’s concall in the afternoon, broad takeaways:-

Reiterated Growth guidance of 23-25% in Music licensing business.

Major Hindi Launches coming up, if you check the main channel. Then views have barely grown due to no launches. Its the regional channels like Bhojpuri and Punjabi which led to growth.

Music Licensing Business grew at more than 20%+ again this Quarter. Carvan realisations have fallen

.

They have announced Rs3 dividend per share.

Will only invest QIP money when a suitable opportunity comes up and won’t do acquisitions just for the sake of it.

Near term risk:-

Margins might come down a bit due to lower margin business like events, movies etc increasing. I think events here are joined at the hip with licensing business to drive growth over there.

These were the short notes in a nutshell. Might have missed a few points, will keep updating.

Disc: no reco to buy or sell. Added in last 30 days. Not an Advisor.

Answer for SAREGAMA entering low margin business of Films

Source - Concall

One, we are in the larger business of

entertainment, and not just music.

Second, even to protect our music business, we need to be

there in these segments. Films is something that every competitor of mine is working on. And

you can go and check that almost every Indian player who is into music business is also into the

film business.

It gives us a very secure way to secure music of the films because we start getting into the

funding of it. Secondly, when we talk to these digital platforms, almost all of them are now

licensing both music and films from us together. So, it improves my negotiation position to a

very great extent.

Thirdly, as long as these are positive value accretive, I can’t grow at a rate beyond 23% to 25%

unless I’m ready to take a big hit on my margins. This is because to grow at a rate faster than

that, I’ll have to acquire music at a very, very high cost, which will have a dent on my bottom

line.

Further, we push for additional growth

from other areas, which have a synergy with music and still are positive margin businesses.

Answer Regarding Low Margin Business of Live Events

Source Concall

What it does is that when an artist

comes to know that not only can he sing songs for Saregama, but he can also do Live Concerts

with Saregama, then the artist wants to work with the company that much more than he wants

to work with the competition.

The competition may be offering only songs and nothing else. That’s our main edge. So multiple

artists are now reaching out to us and saying, listen, we want to give you our songs, maybe at a

discount, but can you also do something on the live business with us.

First instance of a deal failing between an Indian music label and a streaming company? The ecosystem while heavily loaded in the favour of labels, also benefits from a network effect of more labels and more songs being present on the streaming platform. If this is not resolved, not only is it bad for Zee and Spotify, it can also be bad for other labels like Saregama as the streaming network becomes less valuable to a user.

IMO, both the parties need each other. There is a precedence of renewal talks falling off and deals being struck eventually. Saregama-Meta is one instance.

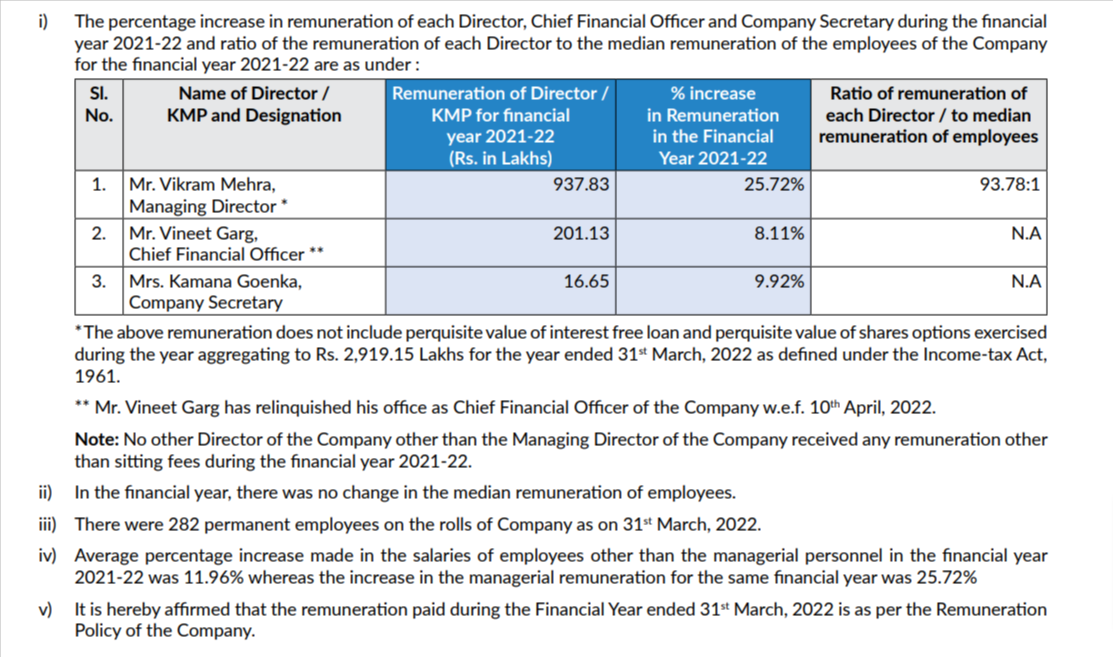

Hi All, I was looking at Saregama’s ARs and found a few things which struck out as oddities. I wanted to understand this groups’ perspective on this. It would be super helpful if you all could throw some light on this

Salary hike % mismatches

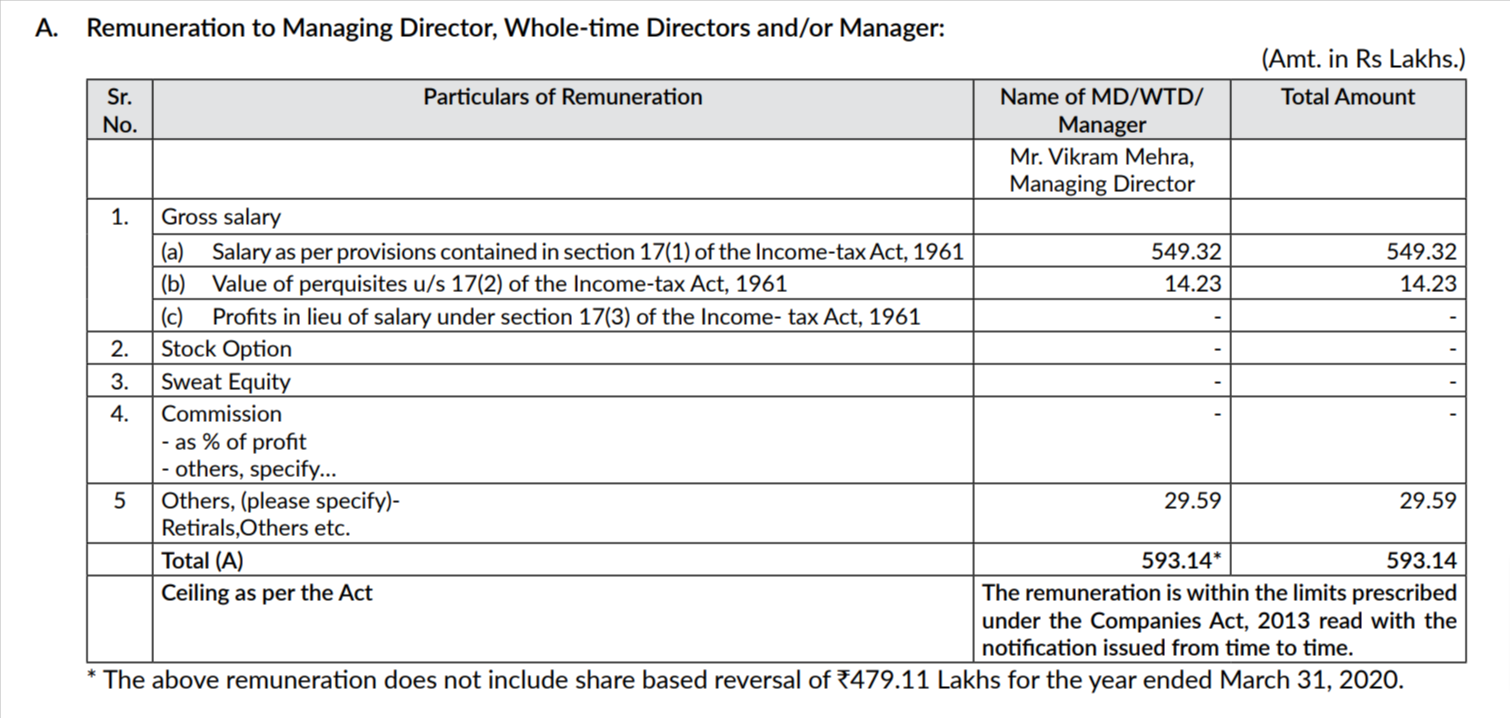

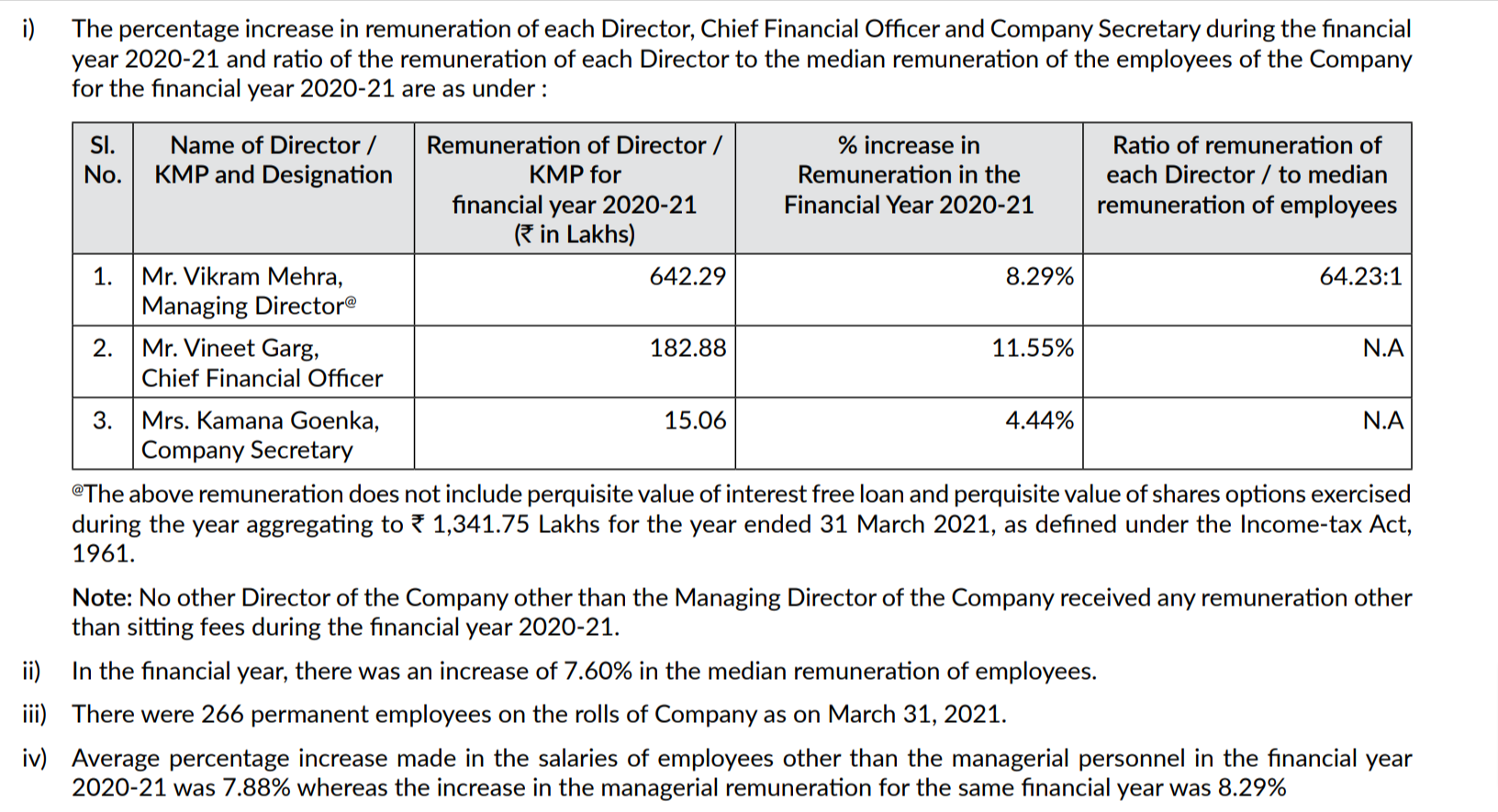

I am seeing a few aberrations in how the remuneration hike % has been calculated for Mr. Vikram Mehra across the financial years.

However, this is where I didn’t understand the hike %. Mr. Vikram’s salary has increased from 6.42 Cr to 9.37 Cr, a 46% hike. However, the table shows 25.72%. What am I missing? I tried adding the interest-free loan mentioned below the table and still, it doesn’t add up. Any thoughts on this?

While Mr. Vikram got a hike in FY 22 for the company’s stellar performance, the other employees didn’t. Any articles that can be shared which allude to why this might be the case?