I am talking from the perspective of the minority shareholder. To a CA everything looks like a tax matter.

2 Likes

Lol… If there is tax planning which can be done - then why not

On a serious note, the ratio is decided on the basis of valuation and I think the valuation prescribed is not fair (Spin-off’s are always investor neutral so nobody looses anything)

And valuation is a very opinionated term and people may think otherwise…

1 Like

Can somebody please explain the meaning of this? Will I also get shares of demerged entity as a Saregama shareholder? What if I don’t want to get shares of demerged entity and want all my invested money in Saregama itself. How this transfer of shares happen in case a demerger?

Please pardon me asking such basic questions.

You will get shares of demerged entity. You can sell it once you get it.

If you don’t want shares you will have to sell saregama before record date

1 Like

Demerged Company means the original Company viz. saregama minus hived off Digital distribution business… Your investment in Saregama will stay as it is. . Because of demerger it is called demerged Company. After the Stock split, your Saregama qty will be increased to 10 times because of face value Change. Because of demerger you will get new shares in the new Hived off company which you can sell or retain as it is getting listed separately. Hope it clarifies your query.

5 Likes

Mr. Vikram Mehra, Managing Director, Saregama India interview

4 Likes

1 Like

First concert was attended by approx. 18000 people.

10 new dates announced for Canada and the US.

2 Likes

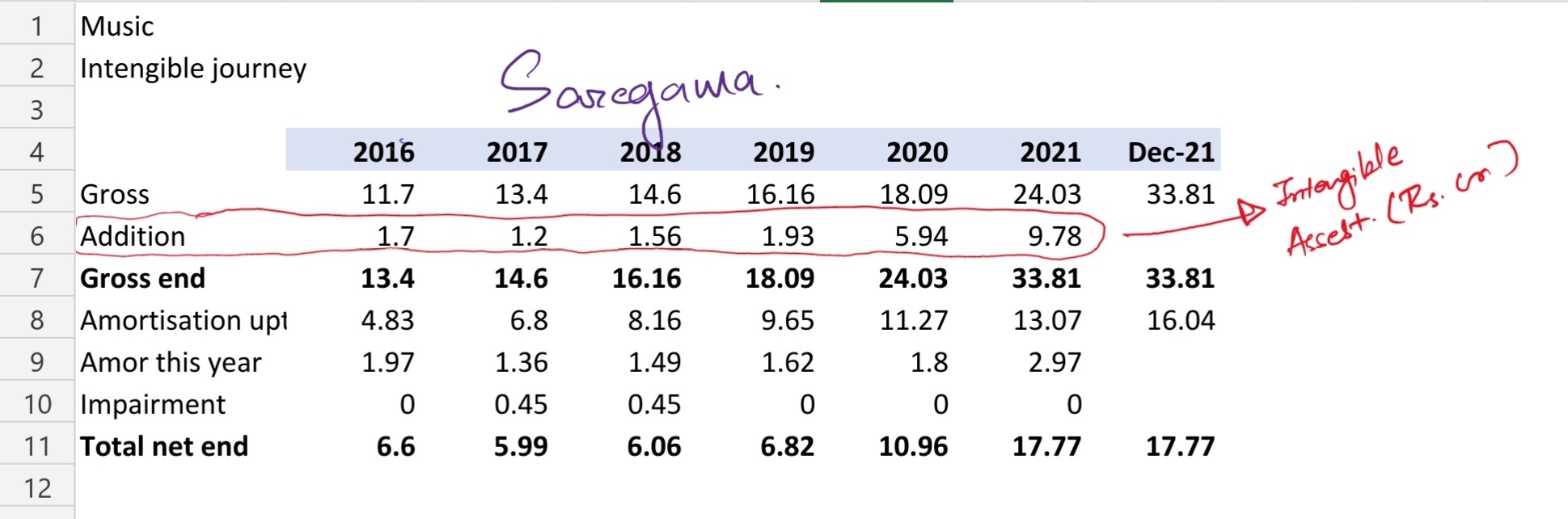

Can someone please explain how where does it show music acquisition on balancesheet? As per their annul report its intengible assets. I have calculated all additions in intengible assets for last 5-6 years. the figure seems very small. Against that content charge they are showing is very high.? Does anyone know how this accouting works? Mnay thanks

for example, content chanrge in FY20 is 17.6 Cr, but net addition is just 5.9cr

2 Likes

Was very disappointed to see SAREGAMA using funds to hike its stake in group companies.

Isn’t this contradictory to what the management has been saying about the usage of QIP proceeds? Why did they raise money and dilute equity when they evidently don’t need it for their core operations?

13 Likes

Well if I am calculating correctly about 25 cr would have been used to increase this stake across two companies given their Mcaps. Proportionately small amount

I am more concerned about the strategy than the amount. Even still, the amount is still more than half their quarterly profit.

3 Likes

They are hiving off these investments in a new entity so it won`t be the case going forward. Refer to latest demerger announcement

3 Likes

2 Likes

Good article but I think it is more relevant for developed markets like US where OTT growth is reaching saturation…

This could be one of the reasons for the 10% fall in the saregama stock in the past few days but I think the fall is uncalled for (not sure though if this is the only reason or is it just a co-incidence)

Lets see how what quarterly numbers the company reports and a lot of things will get clear…

7 Likes

Nice conversation on digital music industry

6 Likes

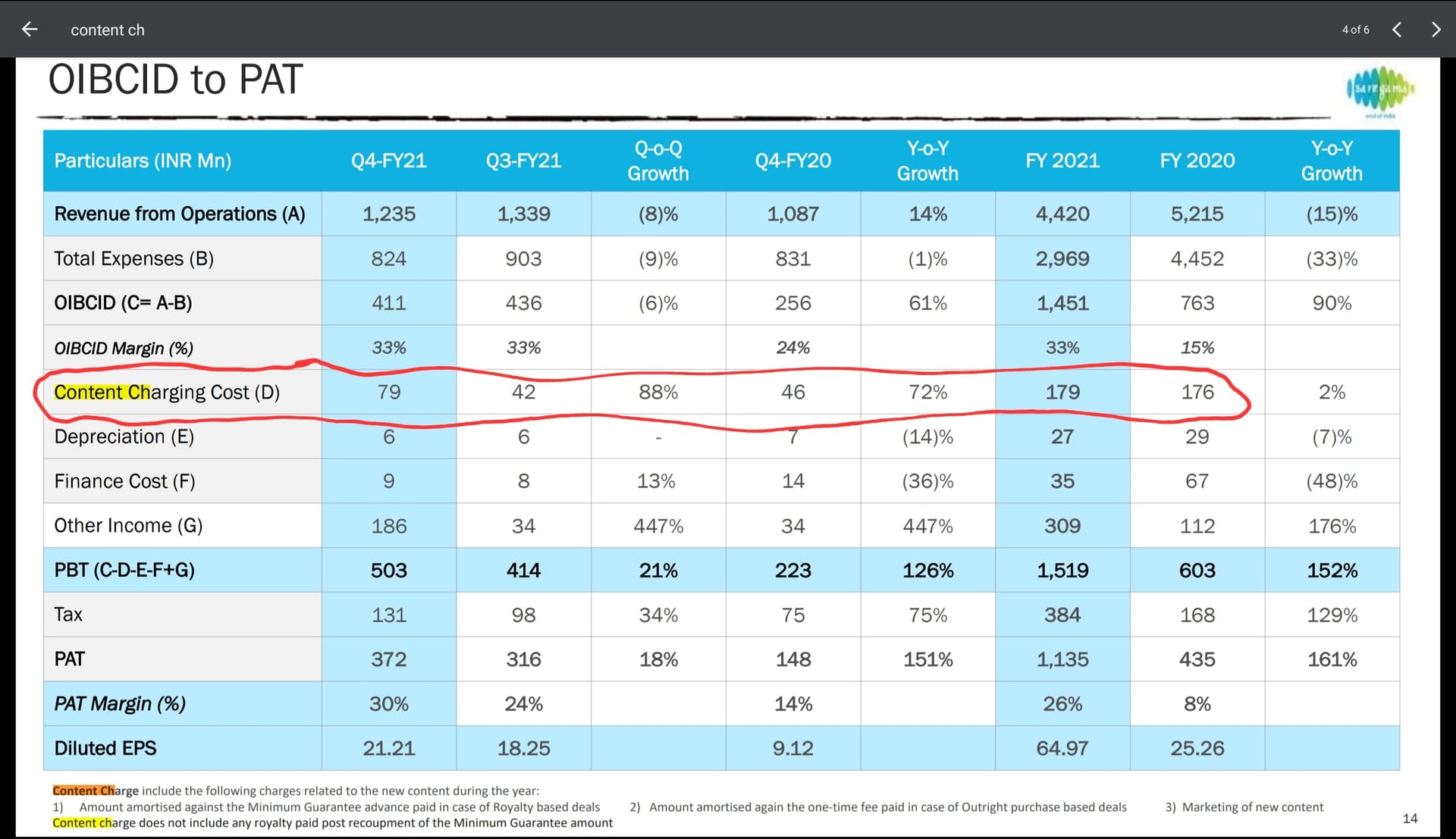

Concall Highlights:

Commentary:

- Story is going to bullish going forward.

- Music License growing at >20%, four years in row.

- Content chares are 46cr in FY 22.

- OBICID will be between 32% to 33%. This year is exceptional.

- Acquiring of Mango music with 1500+ songs give boost to telugu music business, more pricing and negotiation power with TV channels.

- 10000 more songs digitized under “ Atmanirbhar” project. Now catalogue is at 142000+ songs.

- PBT is less due to higher contribution from film business which is 15%.

- Gangubai Kathiawadi + Sarkari Vari Patta touch 1B views combined in approx. 3 months. Paani song touch 2B views.

- Carvaan have breakeven, Zero marketing and man power spend.

Competition:

- Industry grow at 11%, company grow at 26% due to market share increase.

- Company achieves it by marketing power, influencer marketing, data analytics, balance sheet ( money and royalty paid on time is huge edge), predictive models.

- 80% of time, it is proved right that based on predictive models, company walk away from deals due to higher amount of project.

Public Performance:

- Muted due to covid wave in new year.

- IPRS going strength to strength, it is mutually benefit to company as well as artist.

Carvaan:

- Demand is increasing, supply is issue due to chip shortage.

- No marketing, man power spend will continue.

- Breakeven this year.

Pricing Power:

- Expect subscription model for audio OTT to grow in next 18 to 24 months, which brings pricing power.

- Not affected directly by de rating of platforms such as Netflix, as company have deals with minimum guarantee.

- Music companies keep status Quo.

De merger:

- New company will market goods from all companies, not only caravan.

- Non-core business such as OPEN magazine, investment in group companies etc. will be hived off.

QIP:

- Spend money only on QIP charges and mango music. In advanced talk for in organic growth but only when opportunity arrives. Money is safe in FD.

- 27 Cr. Paid to Kolkata Metro Rail, which is saregama subsidiary to get shares in other group companies, it will be back when company is merged with saregama.

- No money is invested in group companies.

Artist Management and Live performance:

- Not required large investment, it can sustain by money rotation.

- Initially have 5 to 7% margin, once established can have more than 10% margin.

- It only look at music related shows, not like fashion shows.

- This vertical gives access to artist, convince them to do songs for saregama, bundle deals like doing a song with few performances etc.

Audio/Video OTT:

- Views from US/EU have higher revenue due to high advertisement rates.

- Download button on OTT is called offloading. When subscription ends, downloaded songs also go away. Eg. If person download a song and listen 10 times during flight, when person connect back to app, it is counted and company get paid.

- More money coming to digital advertisement then TV.

- Sustained increase in views/listen with increase in revenue.

Piracy:

- Carrot and stick policy worked well.

- More people use Youtube/Audio OTT as it is easily available.

- Piracy is difficult to control in web browser (WWW.) In APP it is very low. When any APP found using IP without license, reach out to google and apple as they own stores, they remove that APP.

- Going forward piracy in smaller town will also come down.

Disclosure: Invested

40 Likes