Focus on regional music is visible.

So, till today I had a perception that International music will keep on taking away market share from Hindi and Regional Music, and thus becoming an anti-thesis for Indian labels.like Saregama. However, today I came across an article which has a quote from the MD of Warner Music India which shows the reality.

"The market share of international music is decreasing but its consumption is increasing in absolute numbers. According to Jay Mehta, the MD of Warner Music India, “Right now, international music contributes to approximately 13% of overall audio music consumption. Over the last three years, the contribution in percentage terms has gone down but in terms of sheer volume it has only gone up. With every new expansion into Tier-II [and] Tier-III cities, a new user consumes either Hindi or a regional language as their primary languages and English as a secondary language. There is an increase in consumption but not at the same intensity as it used to be.”

This is the link to the article:

https://musically.com/2021/10/14/india-music-industry-all-about-music-2021/

A very good experiment you can do is to check the song views on Saregama Bhojpuri and Gujarati channel. I was taken aback with the sheer number of videos with a million+ views on last 6months. It was close to 46+ for Gujrati and 50+ for Bhojpuri.

Disc:- invested.

Paani Paani Bhojpuri launching today… Will further confirm the regional language hypothesis…

Yet to go through it but should be great.

Where does Saregama make more money per song- through YouTube or if someone listens to it on a streaming App?

Chaitanya_Motani

In youtube per view rates changes from country to country. Approx. 20 paisa in India to 5 rupees in America. All are very rough estimates. In music apps they get 10 paisa per stream ( there are many music apps).

Hope this clarifies.

Disclosure: Invested.

Streaming is the bulk of revenues as mentioned in Q2 call

Yes, but they have much higher margin when someone sees it on YouTube, right?

They also get some money upfront from the streaming platform… need to double check…

Hoopr uses AI to find royalty free music for content creators. Using Hoopr, content creators don’t really need to pay music license fee to music labels like Saregama & TIPS.

Definitely super small in grand scheme of things but very interesting anti-thesis.

It won’t work in a country like India where most views are garnered by film music. Might work to some extent in America.

Thoughts?

Interview - Mr. Bhushan Kumar – Chairman & MD (T-Series)

T-Series has been the most popular channel on the world’s largest OTT, YouTube, for a long time. Earlier this month it crossed 200 million subscribers, bringing in roughly 10% of YouTube’s global users.

Q. Do 200 million subscribers reflect just T-Series or all its channels put together?

A. This is just for T-Series. We have 29 channels across languages and genres. The total subscriber base for the T-Series network is over 383 million and these get over 718 billion views.

Q. What does it mean for T-Series?

A. It took us 10 years to reach 100 million and within two years we have doubled the number. Our job is to serve music. This kind of love from our audience shows that our music is working.

Q. What changes did Covid bring for T-Series?

A. Since there were no film releases during the pandemic, there was no film music. So we did a lot of non-film songs, about 100. Of these, 80-85 worked. Sad songs worked more during the pandemic, now (as things opened up) party songs and romantic songs like Chaka Chak (from Atrangi Re) or Kusu (Satyamev Jayate 2) are doing well. The music market is booming, there are lots of streaming apps and opportunities to monetise.

Q. How is T-Series placed?

A. We have the highest number of streams on all platforms. The short video market has been giving us licence fees. The consumption of music in short format is rising day by day. There are so many apps — Reels, Moj — with mass audience consumption. And what works is not necessarily a new release. The majority of consumption on short video apps and streaming platforms comes from our library (more than 207,000 songs and 62,000 videos). The size of the business remains small (the Indian music business is just about Rs 1,500 crore in revenue overall), but the valuation is rising because there is lot of opportunity from platforms such as YouTube, Amazon Prime Music, short video apps; these are helping increase revenue.

Q. You have been investing a lot in films. What does it bring to the T-Series top line and bottom-line?

A. Both music and film bring in roughly half-half of our business. Music does better because of our catalog, especially the devotional songs are a huge revenue earner. Hanuman Chalisa alone has got over 2 billion views. We are adding 50-100 songs to the devotional catalog. We will be co-investing in/producing 40-50 films in the next 18 months. That involves Rs 1,500-Rs 2,000 crore in (overall) budgets. Just ‘Adipurush’ directed by Om Raut (due for release in 2022) is a Rs 400-crore film. (It has been billed as the most expensive Indian film).

Q. Is all this film investment happening to feed the music business?

A. The perception is that T-Series does films only for the music. Now, so many films we do have no music or just have a background track or title song. Parallelly during the pandemic we invested in a lot of non-film music.

Q. Do you raise money for films or acquiring music?

A. We never raise capital. All the money comes from T-Series.

Q. Are you planning on launching an audio or video OTT?

A. We are exploring the idea of a video OTT but no plans for an audio OTT. There are some great music platforms already available.

Good insights from the T-series interview and they seem to be betting big on YouTube. Even though they have mentioned that they don’t have any plans for Audio OTT, what does this mean overall for listed companies such as Tips and Saregama as these too have a good and growing presence on YouTube? Thanks.

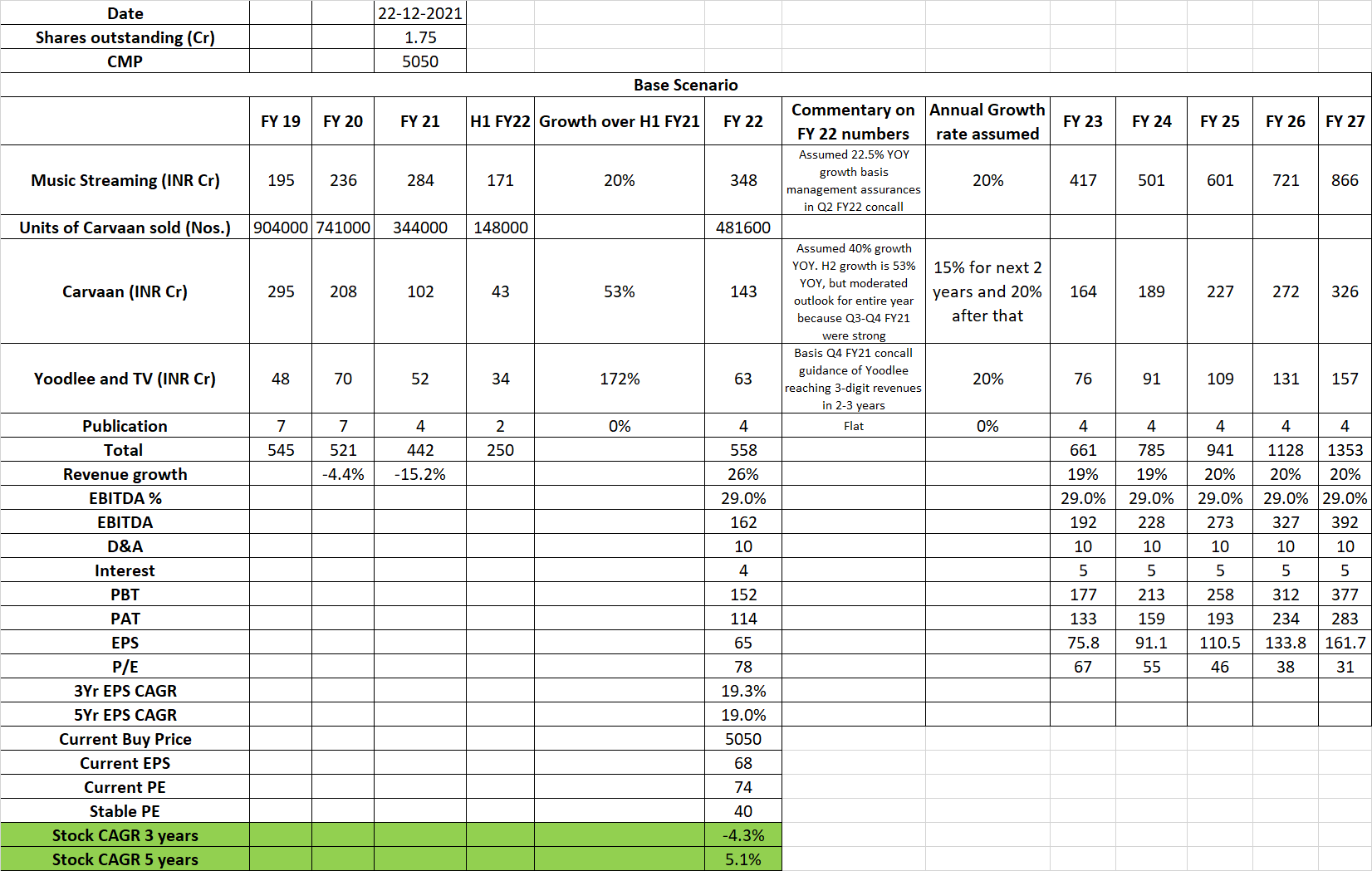

Hi guys! This is my first post on this thread. I went through almost all the messages on this thread over the last 2 days. I am a late comer to the Saregama party and yet to take a position. But I have been tracking the stock closely for the last 1 month or so and am more or less up to speed on the company and its growth prospects.

I am waiting to take a position, but I feel I won’t make any returns in 3 years if I buy the stock at current prices of INR 5000. My assumptions for this calculation are as follows:

-

I have assumed a stable state PE ratio for the business at 40x (digital business based on IP monetization with good gross margins should be able to command such a PE ratio I believe) - I want to understand from you guys if its reasonably possible for Saregama to command a higher PE, say 50x, 3 years from now?

-

I have assumed revenue growth @ 20% YOY (Equal growth rate of 20% assumed across music licensing, Yoodlee and Carvaan which has a low base due to Covid) - I think this is a reasonable base case assumption?

-

I am making the risky assumption that EBITDA margins will remain stable at 29% over the next 3-5 years. I hope Management will not invest capital in publishing or Carvaan if better returns are possible by investing in music streaming or Yoodlee/TV.

With the above assumptions, 3 year CAGR return on investment in Saregama stock at current prices as per my calculations are about -4% and 5 year CAGR returns are only 5.3%. Even if I bump up the stable PE ratio to 50x (Which is very risky in my opinion), 3 year and 5 year CAGRs are 3% and 10% respectively.

Attaching my projections below for reference.

So has the stock run ahead of its potential for a 3-5 year timeframe and therefore should I wait for the stock to correct to 4000 levels? Or am I missing something in my forward projections for the base case and 4000 levels may never happen?

Some comments on this from long term investors in Saregama will be very valuable!

PS: Is anyone aware of segment wise gross margins for Saregama? That info would make forward projections more accurate. I think management mentioned Carvan is running at EBITDA breakeven levels since Covid. But not sure what kind of GMs are there in Yoodlee or streaming

Revenue growth will be much higher than 20% as you havent factored the upside from the 750 cr QIP money which will be deployed to buy out smaller labels and also Caravan is coming up with optionalities, thats why market is giving it a higher valuation. Thanks