Saregam QIP, discount of 100 Rs per share as per the last closing price

5 Likes

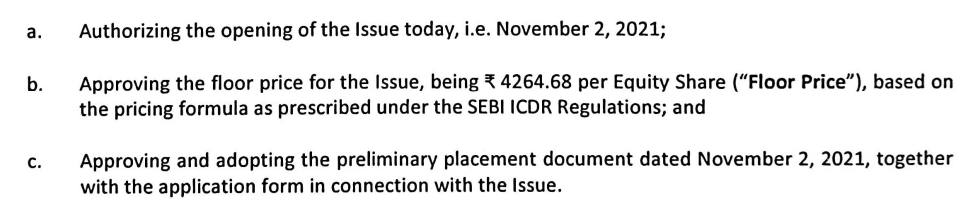

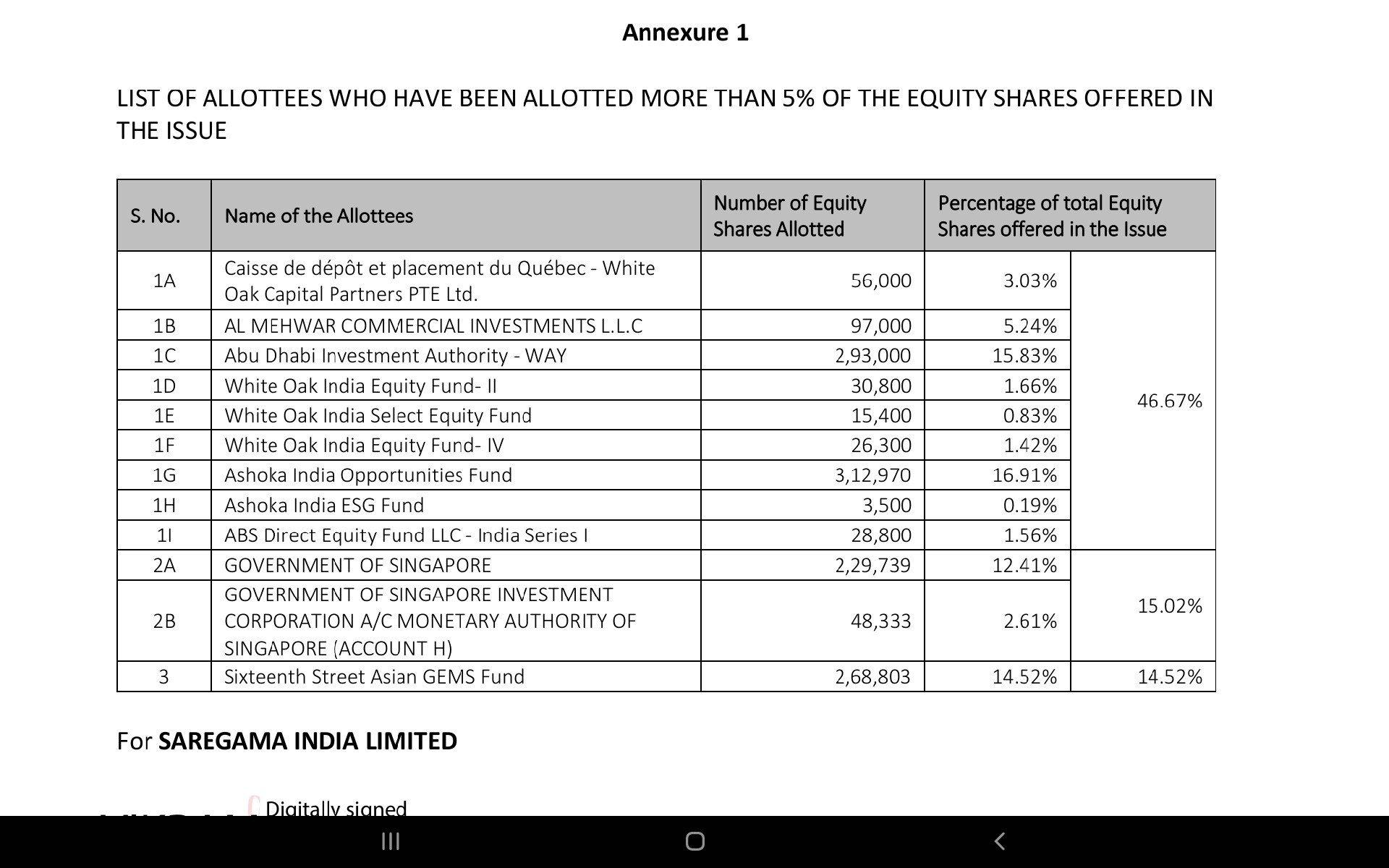

allotment of 18,50,937 Equity Shares to 27 qualified

institutional buyers at the issue price of ₹ 4,052 per Equity Share (including a premium of ₹ 4,042 per

Equity Share), aggregating to ₹ 74,999.97 lakhs (Rupees Seventy Four Thousand Nine Hundred and Ninety Nine Lakhs, Ninety Seven Thousands only), pursuant to the Issue. The Issue opened on November 2, 2021 and closed on November 10, 2021 and the same was intimated to you through our letters dated November 2, 2021 and November 10, 2021, respectively.

Pursuant to the allotment of Equity Shares in the Issue, the paid-up Equity Share capital of the Company stands increased from ₹ 17,43,00,120 consisting of 1,74,30,012 Equity Shares of ₹ 10 each to ₹ 19,28,09,490 consisting of 1,92,80,949 Equity Shares of ₹ 10 each.

Good quality investors, Approx 10% Equity dilution, 750 cr + cash in hand, deployment next monitorable.

7 Likes

Nearly 20% is with Ashoka and White Oak, strong hands.

2 Likes

Ashoka and White Oak are basically the same BTW. Ashoka is the name of the funds and Whiteoak is the India based advisory for those founds. So all are sub accounts of the same account.

4 Likes

Hello everyone. I have some questions in case someone can please answer them:

- What is meant by takedown rate in piracy?

- Manufacturing of Carvaan is in-house or outsourced?

- How is it determined which music label gets the IP for a particular song? Is it an auction mechanism between music labels and the highest bidder gets?

- When Saregama had 120K+ songs, they said time to replicate for a new entrant acquiring 1000 songs a year will be 120 years:

When Saregama had 130K+ songs, they said time to replicate for a new entrant acquiring 1000 songs a year will be 100 years:

Is this a typing error or am I missing something?

Thank you.

Disc- no holdings but researching and tracking closely

I have a question regarding recent Equity raised by the company. Company has a RoE of 25% over last year and it has now raised 750 crores. Even if I consider 15% RoE on this additional equity (mgmt guides for 5 years’ time for IRR), does that mean we will see profits increase by approx. 110 crores in next 1-1.5 years i.e almost double the current level?

6 Likes

Saregama Latest Analyst Call - Highlights - Please feel free to add on to this

Will grow at 25-30% for next 5 years

750 cr QIP will be used to acquire new content + Smaller labels- 35% of the new content will be acquired with this money + small acquisitions(500-5000 songs) and with that library, Saregama can monetize it in a better way

Internal accruals can fund 15-20% of the new content, to acquire content aggressively, needed QIP, from year 4-5, internal accruals would be enough, no need of fresh capital then

Foreign markets- Deals are mostly with artists, in India deals are done with producers where industry contacts help, so entry barriers are quite high, that`s why foreign players would have a tough time

The next round of growth will come from Tier 3 and Tier 4 cities and small towns. Making the right investment in different languages and growing market share. They have gained a significant market share ~50% type in regional language as big players are not present and it`s easy to compete with small players ( For e…g Gujrati, Bhojpuri)

Caravan - Turning into a proper platform- Launched New caravan just before covid so it is yet to be seen how it plays out. Avg listening time approx 6-6.5 hours. they have got all the analytics of what people are listening etc, introduced podcasts and other cool stuff along with pre-loaded songs, Caravan optionalities are huge, looking at tie-up with auto players for preloaded systems and various other things like this

Data Analytics- Have a team in acqusition side to do all the data analytics. For e.g Combination of actor/artist or artists/ composers etc how it has played out in the past and then building models around that to figure out what could be the potential outcome of new releases, ROC etc and then bid accordingly

Risks- Streaming players chasing valuation game by getting more users and offering free music. Indians pay a lot for DTH, OTT, etc, sees no reason why they willl not pay for music. Currently, they get 10 paise, if subs numbers go up, it can result in anywhere between 2-5x more growth

So 25% growth will be accelerated to 30% with aggressive content acquisition, Caravan could contribute meaningfully, regional market share gain is quite encouraging.

22 Likes

Hi Kashish,

Can you post the link to this call.

I want to know if the management was questioned on its open magazine business.

1 Like

Thanks for sharing. This is the Q2 earnings call right?

For someone who is new to this thread or wants to understand music industry. Good basic coverage for both saregama and tips.

Disclosure: Invested

3 Likes

This is from the RPSG virtual investor conference

1 Like

Hi, Kashish

Can I get conference call as I do not find it in public forum. Thanks.

https://www.rpsg-ic2021.com/

register yourself and then click the tab titled “Agenda”

1 Like

Good quick watch on what owned content vs Others content can mean - apparently it has created survival & growth challenges for Netflix - gives a good idea about importance of Content ownership over longer term.

While Music being highly profitable business and excitement around possible kickers with Subscription picking up is a prime thesis for Saregama, Yodlee IMO is equally exciting optionality though not as glamorous as Music piece Yet.

And it may never be as exciting. Squid games, even though a blockbuster hit, may not be consumed more than 2-3 times ( I rarely watch any series or movie twice ), on the other hand, a super hit song / album have the potential to be consumed for infinite nos of times and for very very long period of time. Decades in some cases.

Time and resources required to create a video content vs an audio and the potential ‘recurring’ revenue from audio, makes it an exciting play.

Consider this, you wouldn’t mind having multiple OTT subscriptions for your video consumption but for audio, all one needs is a Spotify or an equally good alternative, and he/she will have all requirements met. Very different dynamics IMHO.

9 Likes

Kind of Disagree here and content relevance is very subjective - wouldn’t Quality Content on Video have substantial life as well - Seinfeld/ Everybody love Raymond and many more will appeal to one or two generation forever as well. Next generation will develop own taste - be it music or video. Hence continuous and aggressive refresh of content needed as evident by Saregama QIP.

As investors we are attracted to higher return profiles that is projected for Music, question is do we have data on long term returns for both keeping in mind acquisition refresh spends?

Squid games return profile (in crude way - present value of money made can sponsor many such series productions at nominal Bank interest for forever)

Squid Game, Netflix’s biggest original series launch, is estimated to be worth almost $900 million (roughly Rs. 6,770 crores) for the streaming giant, as per a report citing figures from an internal Netflix document.

In comparison to its estimated net worth, the showcost just $21.4 million (roughly Rs. 160 crores) to produce, Bloomberg said.

Point is IRR for fresh investment will probably will not be hugely different for both segments for Saregama, If one calculates on fresh content and forward basis only. Why else Saregama bother create and scale this unit?

Given low Fixed asset base of music acquired long back - returns ratio look extremely attractive , 750 cr QIP once added will increase that capital base as well( current Fixed asset base bring 244 cr only). At the same time Yodlee which is in infancy will have content library being built offering better returns over life.

Not to mention the New lables coming up in game, Desi music factory already has crossed them with 31M YT subscribers being way younger than Saregama and much smaller content base.

While we all have music as core investment thesis, As investors we need to keep anti thesis pointers in mind as well and having Yodlee provide a nice optionality if executed well.

3 Likes

6 Likes

4 Likes

Fair to say the company & the management have done a phenomenal job over the past few years. I get the whole story, potential of the music licensing piece, the entry barriers & underlying free cash flow generation potential.

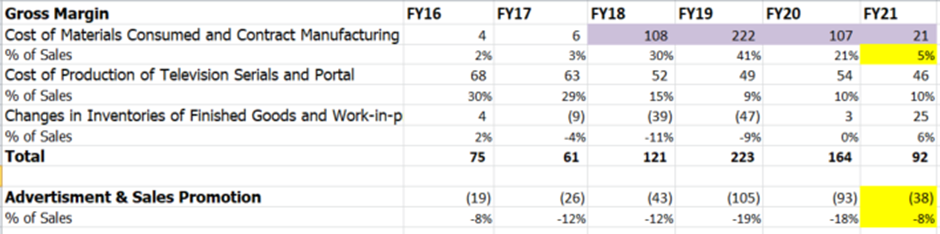

Looking at drivers of earnings which have played out post FY20, need to be cognizant of current profitability.

Stripping away oci/exp items(bulk is Changes in fair value of equity instruments designated at FVOCI), very roughly bottomline moved from ~30-50cr in FY18-FY20 to ~115cr in FY21. 1HFY22 vs 1HFY21 too has been strong 61cr vs 45cr.

The post FY20 big move in margins has been on account of 2 line items:

- Cost of Materials Consumed and Contract Manufacturing Charges – Primarily this. As per historical trend this is a bumpy line item. Very low acquisition of content post FY20 has curbed spends here. At some point, this will reverse, esp with the management’s stated strategy of acquiring content aggressively. There’s a big swing in reported margin on account of this.

- A&P – Lower promotions on carvaan. This may go up in the future at some point when the co resumes spends, but the key line item to watch out for earnings would be Gross & its impact.

Current adjusted PAT margins post FY20 of ~26-28-30% look bloated to some degree. When the co starts acq content aggressively, there can be a drag on margins vs today. Some mean reversion on account of Gross. These margins may sustain for some time, just need to be mindful of the possibility of the lumpiness in profitability here.

& accordingly estimate fair valuation & possible entry prices.

13 Likes