Background & History

Sanwaria Agro Oils Limited was incorporated on April 22, 1991 having its registered office and corporate office at Bhopal, Madhya Pradesh. The family had been in commodity trading and milling of pulses since the 1950s. They set up a solvent extraction plant with crushing capacity of 200 tons Per Day of Soybean & other minor oil seeds at Industrial area, Kheda Itarsi and commenced commercial production from Dec 5, 1993. Since then, Sanwaria Agro has grown on the back of a series of acquisitions of sick or closed units which it turned around successfully. Subsequently the soya crushing/refining capacity of the company has been expanded further which is 2,500 Tons per day as on date. The expansion of the capacity was wholly financed by internal accruals.

SAOL garnered many accolades but the high came when Motilal Oswal in their study titled ‘16th annual wealth creation study (2006-2011)’ named Sanwaria Agro, alongside stalwarts like Reliance Industries and Kotak Mahindra Bank, the ‘Fastest Wealth Creator between FY06 and FY11 adding INR43b to its market cap at a CAGR of 119% per annum.

Director Anil Agrawal’s father, R.N. Agrawal, set up the company in 1991 when Ruchi Soya and Prestige Foods were already established players in the market. By 2013, Sanwaria pipped industry leader Ruchi Soya on financial parameters like return on capital employed, operating margins and earnings per share. Speed thrills … but also kills! Till 2013, Company was happy with its traditional business enjoying good growth. But thereafter the Agro Oil business went into consolidation, with small units selling or renting out facilities to large ones for manufacturing value-added products. With sustained fall in oil and elevated seed prices worldwide, domestic crushing units faced a disparity of $40-50 a ton. This means imported oil will be cheaper by $40-50 a ton than through domestic seed crushing. All the big names, Ruchi Soya, Sanwaria, faced survival issues. Ruchi Soya, incurring operational losses, sold its stakes in Gemini Edibles and Fats India (GEFI) to a Singapore-based Company. Since the edible oil crushing and refining business faced trouble, large players shifted focus on value-added segment, where business potential was quite high. Anil Agrawal, MD, Sanwaria Agro Oils had then said in an interview, “Producers of value-added products enjoy a different ball game all together. While primary edible oil producers face disparity, margins are high for producers of value-added soya products”.

Rebranding – A matter of survival

In adversity lies the opportunity. With a lure to get into high-margin business, Company, from being a Soya Processor, turned itself into an FMCG player with a range of agro-based products in 2014. They did not limit themselves to Soya-based value-added products, but also launched basmati rice and salt. They extended their edible oil portfolio by getting into sunflower, mustard and rice bran oil. Since 2014, the product portfolio saw several additions like Suji, Maida, Dalia, Besan, Chakki Fresh Atta, Poha, Soya Flour, Sugar Pulses and packaged food, etc. Their upcoming products Tea, Mustered oil, Soya Pasta would cater to the tastes of global consumers.

That was not all - Company also realized that the branded players were able to derive higher margins in the market. Anil Agarwal towards the end of 2013 stated, “Margins are low in the pure processing business. With the rising cost of finance and operations, we need to focus on branding and getting into packaged products not limited to edible oil. This segment ensures higher margins and better visibility for the company”. It prompted him to go for a full-fledged rebranding exercise.

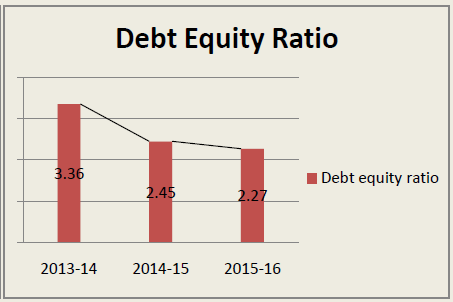

Although the plan looked promising, but the execution was laden with risks. Its easier for a company to expand if their traditional business is in good shape. However, when the current product lines are stagnant with profits on a downward trajectory, it was a matter of survival for them. Restructuring with your back against the wall never comes easy. The debt component increased drastically in the balance sheet with limited outlook for future cash inflows.

On Apr 28, 2014, when Company launched its premium Basmati Rice with an aim to enhance 40-50 per cent contribution to the company’s revenue from its branded products in 2-3 years period, little did they know that either they are underestimating or probably understating the extent of impact it would have upon their topline.

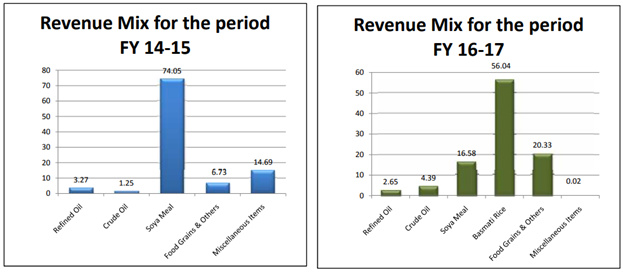

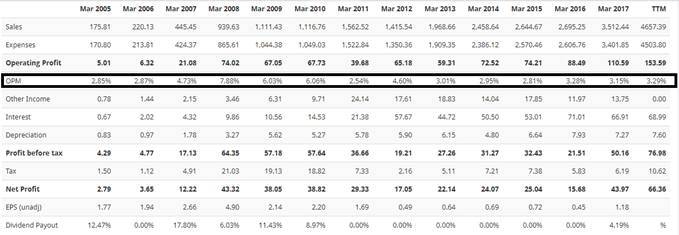

In less than three years, company’s revenue mix had a tumultuous change. Their traditional stronghold Soya based products were now third largest contributor to revenues with just a little over 16% in FY16-17 (down from 74% in FY14-15). Basmati took the lion’s share of 56% (Insignificant in FY14-15) and Food Grains & Others contributed nearly 20% (up from 7% in FY14-15). The rebranding was successful and the business was back on the growth path.

Sanwaria Agro Oils Limited is now ‘Sanwaria Consumer Limited’. With improving financials, the company is now gearing up to service its fat debt. But that’s not going to stop them from taking bigger stage in the business.

The rebranding marks a change not just in the name but a shift in strategy from its core focus Soya Oil to a gamut of staple foods. Company plans to increase its product portfolio from 25 to 50 and then, finally, to 100.

The current set of products include:

• Basmati Rice (Exotic & Premium- Raw/Sella)

• Refined Soyabean Oil, Refined Rice Bran Oil/ Fortified with vitamins

• Chakki fresh Atta fortified with Soya Flour

• Chakki fresh fortified Protein & Iron rich Atta

• Maida, Suji, Besan, Daliya, Pulses (Dals),

• Soya Flour, Soya Chunks (Bari)

• Salt, Sugar, Poha

• Soya Meal, Soya Meal High Protein

• Rice Flour, Lecithin

• Aqua Feed

• Poultry Feed and others

Retail Expansion

Company distributes its products through Patanjali, D-Mart Hypercity, Reliance Big Bazaar, Vishal and ITC Choupals, apart from smaller retailers. It is also getting into direct retailing. Company is opening own retail outlets under the brand name ‘Sanwaria Kirana’. The Company has already opened up 11 stores at different locations of Madhya Pradesh. Further, they plan to open 100 stores in MP and Maharahtra. Thereafter, they have ambitions to cover other parts of India with 500 stores.

Geographic Expansion

• They are raising USD100 Million for global expansion which they would be using for following initiatives:

- A brand building and marketing exercise world over

- Introducing new products like Spices, Mustard Oil, Soya Pasta and more

- Setting up of a Maize Processing Unit

- Setting up a refinery on an Indian port

- Setting up Cattle Feed manufacturing facility

- Setting up soya-based value added product mfg. facility

- Opening 500 stores in UK, Europe, US, Middle-East and Africa

- Company plans to open 100% subsidiary in Dubai to get access to Middle East &

Africa, where especially its Basmati rice will have a steady growing market - Similarly, they have expansion plans in Singapore through its 100% subsidiary which will get business from rest of the world along with cheaper finance facilities.

The Patanjali Tadka

It wasn’t the best way to announce Company’s connections with the FMCG Powerhouse Patanjali when during an income tax raid on Sanwaria’s premises, on charges of tax evasion (which I’ll be covering in detail under risk factors), documents highlighting close relations between MD Anil Agarwal and Baba Ramdev came to surface. The extent of closeness in relations can be understood by the factoid that during his visits to Itarsi, Baba Ramdev used to stay in the farmhouse owned by Sanwaria Group. The documents revealed that Sanwaria Group was producing many products for Patanjali Trust. However, now in the company’s AGM proceedings dated Sept 29, 2017, Company has formally disclosed that they are supplying to Patanjali and are increasing the extent of their association with more products and Pan-India presence as we speak.

Financials

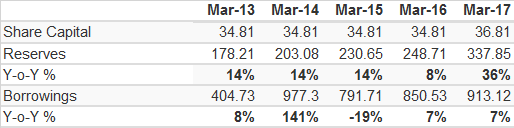

- Sale growth is picking up good pace. They had set themselves a target of 5000cr sales in 3 years in 2014 which they will achieve by FY18. Next their target is to grow the sales to 10000cr in next 3-5 years

- Interest expense reducing and is expected to further reduce as the cash flows improve facilitating repayment of debt. For further expansion, company plans to raise foreign currency debt which in all likelihood would be cheaper compared to domestic debt.

- Operating Margin, however is a big concern which I’ll further elaborate under risk factors

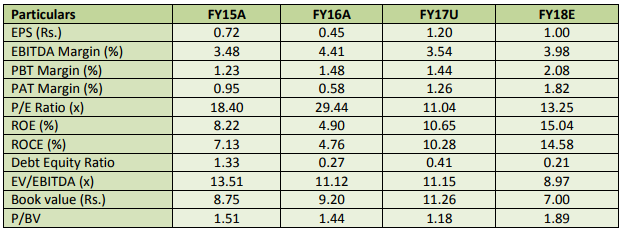

FY 2017 highlights

• Revenue increased by 30%

• Operating profit grew by 25%

• Net Profit increased by 180%

• EPS more than doubled from 0.45 in FY16 to 1.19 in FY17

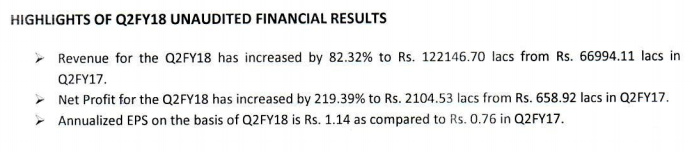

Q2FY18 highlights

• Revenue Q-o-Q increased by 82 %

• Operating profit grew by 65%

• Net Profit increased by 219%

• EPS increased 55% from 0.09 in Q2FY17 to 0.14 in Q2FY18

Source: BHH Securities

Positives

- Company uses the health benefits of Soya Based products in its marketing pitch, which can help it grow well in global markets where health consciousness is high

- Higher control in Value Chain activities with Procurement, Processing, Production, Distribution & Marketing under direct control of the Company

- Promoter holdings have now increased to 71.68% from 70.05% in 2016

- Company claims that Net Sales and PAT of the Company are expected to grow at a CAGR of 13% and 35% Over 2015 to 2018E, respectively. Also, EBIDTA Margins are expected to increase due to improvement in manufacturing efficiency, increase in sale and change in product mix

- Brickworks Rating India have upgraded its credit rating from BBB- to BBB

Rewards, Recognition & Certifications

- The Company is recently ranked 336th in amongst 1000 India’s finest Companies on the basis of Turnover by the “The Financial Express”

- In 2016, Sanwaria Agro Oils Limited was featured among India’s top 500 Companies by Dun & Bradstreet

- It was ranked in top 500 companies in 2014 for income, 318th in 2013 and 389th in 2012 for its Net Profit; 428th in 2013 and 439th in 2012 for Net Worth by “Manappuram Finance Limited”

- In the wealth creation study done by Motilal Oswal, Company was adjudged as the ‘Fastest Wealth Creator’ between FY06 and FY11

- In 2008, the Company was awarded “Global India – 2008” as the fastest emerging company in the Northern India

- In March 2005, Sanwaria Agro Oils received “Outstanding Achievement Award in Export” by FMPCCI

- The Company received ‘BEST CAPACITY UTILIZATION AWARD’ from SOPA from financial year 98-99 to 2001-2002 had achieved 103% capacity utilization as against the Industry average of 35%

- It is ISO 14001, 22000, Halal Certified, “ Good Manufacturing Practice” (GMP) as per the norms laid down by WHO and has been certified by U.K. Certification and Inspection Limited, and Government Recognized Trading House by DGFT with Star Trading House status.

- It had been honored with ‘THE NIRYAT SHREE SILVER AWARD’ for the financial year 2001-02 by the President of India, Mr. K.R. Narayan organized by the Federation of Indian Exports Organization for Export excellence

Industry Overview

- India is the world’s second largest producer of food products next to China and has the potential of becoming the largest producer in the near future

- In India, the food sector has emerged as a high-growth and high-profit sector due to its immense potential for value addition, particularly within the food processing industry

- The food industry, which is currently valued at US$ 39.71 billion is expected to grow at a Compounded Annual Growth Rate (CAGR) of 11 per cent to US$65.4 billion by 2018

- Food and food products constitute ~35% of the wallet spend. Out of this more than 50% comprise of staples like wheat, rice and edible oil

- Current per capita food expenditure in India is 1/6th of China and 1/16th of US

- Spending on processed food is likely to surge 4x by 2020 as the segment has grown at a CAGR of 18% in the past five years

- Going forward, the adoption of food safety and quality assurance mechanisms such as Total Quality Management (TQM) including ISO 9000, ISO 22000, Hazard Analysis and Critical Control Points (HACCP), Good Manufacturing Practices (GMP) and Good Hygienic Practices (GHP) by the food processing industry offers several benefits. It would enable adherence to stringent quality and hygiene norms and thereby protect consumer health, prepare the industry to face global competition, enhance product acceptance by overseas buyers and keep the industry technologically abreast of international best practices.

Going Forward

Post rebranding, Sanwaria is standing at the cusp of growth. The increase in product portfolio, backing of strong FMCG players (like Patanjali, Dmart and ITC), direct retail selling plans and global expansion sounds like all growth levers have been unleashed simultaneously. If they play their cards well, the business could see exponential growth in next 4-5 years. Also if the margins improve in coming quarters, as has been claimed by the company, quite surely the rerating in company’s Price to Earning multiple would happen. From a single digit levels (9.82), it can grow to more comparable PE valuations with its peers like KRBL (28.87), LT Foods (13.8) and Chamanlal Sethia (12.23).

Risk Factors

-

Governance is an issue - According to Watchout Investor, in 2009 Company did not submit the shareholding pattern for Dec 2009 to BSE. Then the company again failed to submit its Corporate Governance Report for March 2015 Quarter. However, in recent times, the company has shown urgency in compliance with reporting matters. In June and September quarters of the current FY, they have been among the first three companies to declare results

-

Generous bonuses/Splits and SEBI Issue and the connection between the two - Firstly, Company has announced bonus shares generously (2005- 1:4, 2008 – 1:1, 2011 – 1:1, 2017 – 1:1). Similarly split happened frequently too (2002 – 10:5, 2006 – 5:2, 2008 – 2:1). Secondly, In 2013, as per a news article, the company and the director of the company, Anil Agarwal were fined Rs. 1 cr. by SEBI for creation of artificial market and price manipulation in Shares of Sanwaria. Company wrote a clarification dated Dec 19, 2013, stating that neither our company nor any of our directors were involved and we have not received copy of any order of SEBI and as we receive we will take proper legal recourse. The probable connection is that if the insiders are involved in manipulating shares then it can be easily managed with a high shares outstanding and low share price which has been managed through regular splits and bonuses

-

Low Profit margins and Tax Evasion and the connection between the two - Firstly, food companies generally command decent margins. All the peers of Sanwaria – The Basmati Players – LT foods (12.19%), KRBL (21.79%), Chamanlal Setia (12.89%) are having good double digit operating margins while Sanwaria enjoys obnoxiously low EBIT margins of ~3% - Almost Unacceptable! Company has direct sourcing from producers with no middleman which does not explain why the costs should be so high. Secondly, In Dec 2015, Income Tax authorities raided 12 offices of Sanwaria Group accusing the company of evading taxes to the tune of Rs. 200 cr. MD Anil Agarwal went underground during the proceedings. Now the connection between the two could be that Sanwaria Group has an associate company in Singapore where the irregular related party transactions have been reported. Company purchased the raw material at high costs to evade taxes. And this explains the high cost of goods and low margins too.

-

In future, if people stop taking staple diet, Comp. may find it hard to sell its products.

Disc: Invested 10% of portfolio. All transactions in last 3 months between Rs. 7 to 7.5

Source:

www.sanwariaconsumer.com/news/research-report.pdf

Sanwaria Agro launches premium basmati rice, soyabean oil - The Economic Times

Sebi slaps Rs 4.5 crore fine on nine entities in Sanwaria Agro case - The Economic Times

www.business-standard.com/article/companies/consolidation-in-edible-oil-industry-small-units-face-the-heat-114121000573_1.html

www.businesstoday.in/magazine/cover-story/anil-agrawal-sanwaria-agro-among-fastest-wealth-creators/story/201069.html

www.bhaskar.com/news/mp-bpl-hmu-ramdev-from-saawariya-close-links-to-create-a-product-of-patanjali-5185535-nor.html

www.moneycontrol.com/stocks/reports/sanwaria-agro-outcomeagm-9078441.html

http://www.moneycontrol.com/stocks/reports/sanwaria-agro-oils-limited-750912.html

www.ibef.org/download/Food-Processing-June-2017.pdf

List of Industries in India: Top, Small, Large Scale Type, Growing Industries

www.assets.kpmg.com/content/dam/kpmg/in/pdf/2016/11/Indias-food-service.pdf

Posting random allegation won’t help anyone.

Posting random allegation won’t help anyone.