I am starting a thread on Sankhya Infotech and to save my time and energy I am taking data from a 4-5 days old interview of the chairman where he has detailed good background and future plans of the company.

Sridhar N, Chairman and Managing Director, Sankhya Infotech Limited,

is a graduate in Computer Science and has nearly 30 years of experience

of providing leadership direction for the growth of the company.

Starting with a mere Rs 20,000 investment, he has spearheaded the rise

of Sankhya as a global name in the field of simulation and training.

Sankhya Infotech Limited is a leading cloud based

learning and training management solution provider across nine domains

that has empowered over 1.5 million users across 50 global locations

spread in four continents. The company has a unique distinction of

offering the complete range of technology-based solutions for eLearning,

simulation and training management system that includes learning

management and online assessment systems. Sankhya has strong Aerospace

& Defense focus and caters to Energy, BFSI, Medical and

Manufacturing domains.

Sankhya is set to launch two technological breakthroughs that would

herald a new dimension in the way professional training is imparted and

we strongly believe that we ride on the strong surge of Internet of

Things.

Give us a brief overview of the training and education solutions industry?

Globally, self-paced training and education has become the key to

success of any industry. To address the four goals of improving

competency, rapid scalability, reducing cost and improving compliance,

industry has adapted eLearning and other training and simulation

solutions. Simulation and technology-based training have cut the

barriers of high tech aerospace industry and they are getting adopted in

Medical, Manufacturing, Energy and even Education sectors at a rapid

pace.

Many corporations report that e-Learning is their most valuable

training method which they use. This is no surprise, given that

businesses save at least 50% when they replace traditional instructor

based training with e-Learning. Not to mention that there is a 60% cut

down on instruction time.

Market size of self-paced learning is US $ 56 billion, and is seeing

23.5% CAGR. Market size of modeling and simulation industry is US $ 9.6

billion and it is moving at a 29% CAGR. The military simulation market

will continue to be led by the US and major European states, however,

their position as leading national markets will be challenged by

emerging powers in the Middle East and Asia in the years to come.

What are the trends in this industry and how are you poised to capture the benefits?

Technology is profoundly influencing the way people educate and train.

Further, concepts of just-in-time learning are enabling creative

solutions for trainees and trainers. Sankhya is the only company in

India that has solutions that address the four goals through eLearning,

Simulation, Learning & Training Management System platforms. We are

at a stage to launch two technological breakthroughs that would herald a

new dimension in the way professional training is imparted and we

strongly believe that we ride on the strong surge of Internet of Things.

Therefore, we strongly believe that the timing to reach out to

investment community at large is right.

Sankhya is different in many ways in comparison to its domestic and

international competitors. The fact that the company happens to be the

only one to offer an entire range of products and services makes it

unique. The company is working very hard to keep the gap of technology

and features of its offering so large that none of its competitors can

replicate its strategy within a three to five year horizon.

What are the opportunities and challenges being faced?

Sankhya’s philosophy has been to provide comprehensive cutting edge

technology based training solution to its customers in diverse sectors.

The company has earned marquee Fortune 500 customers from diverse

sectors of industry by successfully implementing this philosophy.

Opportunities are abounding for Sankhya as it offers a blend of

products and services that fulfill the end to end requirements of

customers. New and unexplored sectors beckon at the company creating a

unique market place for Sankhya.

As the company charts to grow, presence of marketing and sales in

multiple geographies is a one of the challenge, however, the company is

planning to expand its foot print by appointing resellers rather than

having direct presence.

Artificial intelligence (AI) is gaining prominence. Are your courses providing any inputs to update skill sets to deal with such changes?

Two areas are emerging to disrupt the technology market space.

Analytics and Artificial Intelligence. These two areas offer to bridge

the space of reactive technology to predictive and going forward

proactive or adaptive technologies.

In 2003, Sankhya earned Emirates as its customer, and in April 9, 2004

there was an incident to one of Emirates aircraft. Way then Sankhya’s

flagship product “Training Management System” had an analytics tool that

helped the airline to understand the key cause of the incident.

Therefore, the company had the clairvoyance to identify Analytics as a

key to success in future nearly 14 years ago.

Similarly, over the years the company worked hard to adopt Artificial Intelligence in the simulators that we have built.

Till now, the company provided Analytics and AI through its software

products, now the company is seeing the immense scope in providing

services in Analytics and AI in a big way

What is the revenue break-up from various segments?

The company has three business models under the B2B Category, they are

product license, Master Services Agreement, and Annual maintenance

services. Master Services Agreement contributes to 70% followed by 20%

in product license and 10% in Annual maintenance services of overall

business.

What would be the triggers for growth in this industry?

Gartner identifies simulation based learning as the Top 10 Strategic

Technologies. Over 41.7% of global Fortune 500 companies now use some

form of educational technology to instruct employees during formal

learning hours, and that figure is only going to steadily increase in

future years.

Global trends indicate that learner patterns are more demanding than

the past, appetite to learn is seen to grow as technological

advancements are rapid. To stay ahead of the curve, people would demand

more predictive and adaptive learning.

This surge is what companies such as Sankhya have as the biggest opportunity for growth.

**What kind of expertise have you acquired to design the course material and keep it updated with the **

**changing times and requirements. How many hours of training material do **

you have?

We are in the business of enabling organization to achieve that goal by

keeping its associates well-trained and skilled using technology and

ingenuity of simulation and virtual training. Sankhya has a unique

distinction of offering the complete range of technology-based solutions

for eLearning, simulation, and training management system that includes

learning management and online assessment systems.

We have developed high fidelity courses of over 14,000 hours for

diverse fields, we developed over 20 different types of defense

simulators; our virtual reality lab has developed four products in

immersive simulation technology.

The best of Sankhya is yet to be unveiled in the area of Analytics and

Artificial Intelligence based immersive simulation technology.

Which are the verticals you cater to? How is the course structure? Does it differ drastically across verticals?

Sankhya has strong aerospace, defense focus, and caters to energy,

BFSI, medical and manufacturing domains serving Fortune 500 customers in

over 50 locations, spread in four continents. We take pride in serving

the Indian Army and Indian Navy by providing training solutions.

The company also serves the defense forces of three large nations and

some of the best defense organizations in the world. Our training

technology covers energy, medical, aerospace, defense, banking,

education, and such diverse domains.

The company’s training technology is being used by every airframe

manufacturer in the world, large defense organizations, ultra large

energy companies, medical companies and over 53% of all Bank employees

in India use the company’s solutions.

Share some anecdotes on the work you have done with International and domestic customers?

When Etihad Airways had to adhere to the strict regulatory compliance

requirement of “Evidence Based Training” across nine of its partner

airlines covering nearly 50,000 crew, we solved the challenge with our

TMS (Training Management Solution). Emirates was able to conduct blended

training and do extensive training data analysis. TMS was able to show

the highest ROI against all other products considered by Emirates. TMS

was selected against products like ORACLE HRMS.

The State Bank Group’s challenge in transition of nearly 400,000

employees to digital learning was a complex task as a single system

covering five banks and twelve subsidiaries was to be set up and

executed. Sankhya solved the challenge with its online learning and

assessment systems by offering a world class solution that is installed

on an IBM Z10 main frame and can handle over 25,000 concurrent and

375,000 registered users.

Who are your top 5 clients? How much do they contribute to the revenue?

For nearly past two decades, Sankhya has won and maintained enduring

relationships with some of the Fortune 500 companies such as Airbus,

Boeing, Emirates Airlines, Etihad Airways, Embraer by providing

admirable technology based training and simulation services through

repetitive contracts and renewal of Master Agreements. They contribute

to almost 80% of the topline

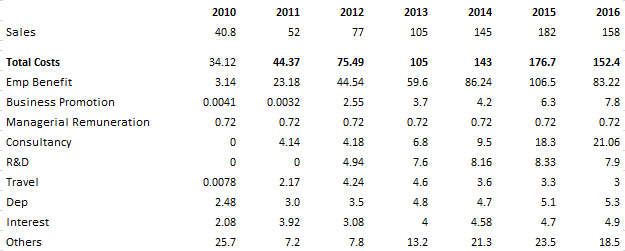

Brief us on your financials. What is the outlook?

In fiscal year ended March 2016, Sankhya witnessed a topline of Rs

152.93 crore with EBITDA Margin of 7.02% and PAT margin of 4.53%.

Whereas, in 9 months period ended December 2016, Sankhya’s revenue is Rs

116.08 crore with EBITDA margin of 10.70% and PAT margin of 3.37%. We

are expecting better growth in terms of revenue from here and expect our

EBITDA margins to improve to at least 15% to 17% by FY18.

You have a host of offerings via simulations. Could you briefly touch upon the same?

Sankhya offers three categories of Simulation solutions, and they are

covered in three industrial areas. The first set is desktop based

simulation solutions these are essentially called as procedural

trainers. The second set is a full motion platform based training

simulations, these are used both as a procedural trainer and for

experimentation of several real-life scenarios. The third category is

Immersive VR simulations, these are asset light, but highly immersive

and provide tremendous user experience.

What are your capex plans and how would they be funded?

We are preparing a Capex / Opex plan for raising US $ 10 million.

What is the shareholding pattern of the company? Any plans to sell stake?

The promoter holding is 24.12% as on Dec 2016. Promoters would be keen to increase their stake in a number of ways.

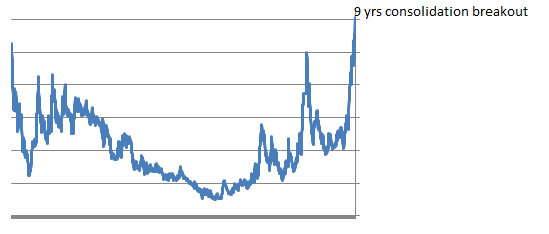

I am personally very excited about the technicals of the company which has given a breakout after 9 yrs of consolidation on back of huge volumes.

I also think the last two answers in the above interview suggests a potential upside in the business cycle.

screenr link.

Disc: Invested from significantly lower market cap.