2GW already done, with rains almost behind us, heading for a fantastic year… should bode well for sanghvi. LT bullish bias ahead.

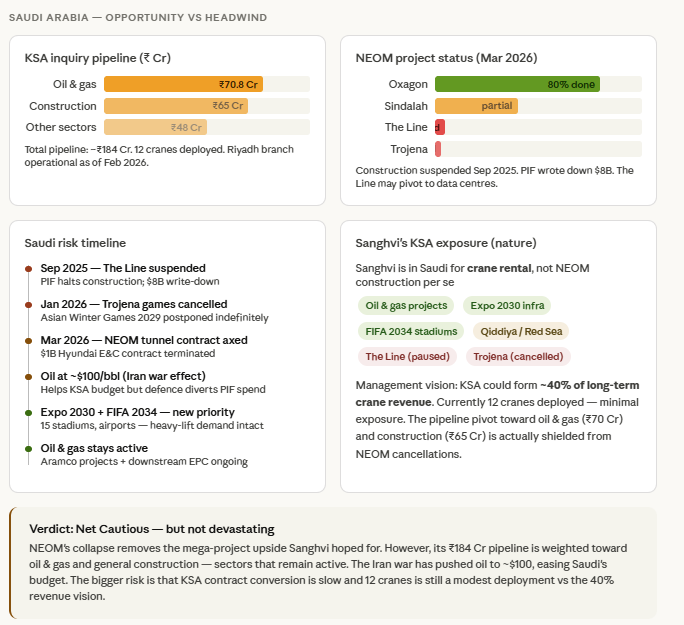

Sanghvi Movers; Saudi Arabia operation as per Q2/2026 con call

Operations in the Kingdom of Saudi Arabia officially began in Q2 FY26.

Market Size: The annual crane rental market in KSA is estimated to be approximately $800 million to $1 billion per year.

Saudi Arabia is going to spend upwards of $500 billion in the next 5 years so Saudi Arabia is an expanding and booming market and in Saudi Arabia there are $2 trillion worth of construction project.

The boom is fueled by major construction projects, including giga-projects, and preparations to host the FIFA World Cup, the Winter Games, and the World Expo.

The company reported 100% capacity utilization in Saudi Arabia as of the time of the earnings call.

Management said that every single asset has moved directly from the port to the site.

The company has deployed more than 30 cranes on site in KSA, and they are all deployed at the customer job site earning revenue.

First Billing: The first meaningful operation or the first billing occurred in September 2025 (within Q2 FY26). Prior to this, in the first quarter (Q1 FY26), the KSA subsidiary did not have revenue, although it did incur fixed costs, primarily employee salary costs for hiring the Saudi team.

EBITDA Margin: Due to the higher operating costs, the resulting EBITDA margin in KSA is currently on par or slightly below the EBITDA margin achieved by the crane rental business in India.

Over the long run, their operational experience and technological capabilities will allow them to improve the EBITDA in Saudi Arabia and bring it on par with the India business.

The company has committed roughly ₹225 crore to procure approximately 55 cranes.

10 Likes

Just started to look at the company. I feel that the stock price is in a value territory.

PE - 15

Forward revenue growth rate: 25 to 30%

Margins likely maintained, though EPC biz will have a bit lower margins.

EPS growth of about 20%, giving PEG < 1

QoQ slowdown is seasonal. Q3FY26 will see a jump as seen in previous years.

The planned capex might have an impact on the EPS if the utilization doesn’t pick up. However, based on the mgmt commentary, this should not be much of a problem.

No promoter pledges or share sale.

No fraud or corporate governance issues that I can see.

No negative audit remarks.

Next generation management in place, US returned and at helm now.

In recent meltdown, the market is giving good discounts on valuations (also similar discount available for EPC companies with clear growth rate like Transrail Lighting). Looks like a nice opportunity here.

Disc: Might slowly accumulate.

9 Likes

Stock coming down as margins are going down.

this is high capex business and go down sharply - it was in losses few years back when Wind power had declined. (wind power is a major business segment).

While Saudi business could be doing well India business is risky.

2 Likes

Management guidance of almost combined capex of 1000 crore(sort of close to 370 crore or may be more in FY27 with final board approval in Feb,2026) for FY26 and FY27,New Cranes moving from port to Site directly

Strong demand from various sectors

Saudi to breakeven in H1 FY27 as operations started in Nov,25 and major Crane deliveries in Feb,2026

Wind Epc margins are premium at around 15% , Cash conversion will improve from 120 to 100 days

Disc : Invested

2 Likes

With increasing oil production in KSA due to the Iran–US war, Sanghvi’s cranes will now be in huge demand

1 Like

What does employees immediate relative mean? Is it some random employee or top management?

Disc: no position

1 Like

Employees’ immediate relative in insider trading disclosures is not some random junior employee’s cousin buying 10 shares.

It usually indicates someone close to management is buying.

This includes:

Promoters

Directors

Key Managerial Personnel (CEO, CFO, etc.)

Senior management

Certain finance/legal/strategy employees

Anyone specifically classified by the company as having insider access.

It does not mean every employee in the company.

1 Like

She is the daughter of the CFO who works for a different company.

1 Like

Stock falling sharply this is due to iran-usa war situation causes the oil price rise sharply but even they are saudi arabia is market player. here is the key the big business is in India if they couldn’t procure oil at this level then the company gonna suffer other than that Saudi may give you the share revenue but the india is the business player.

disc:Invested

Qatar entry was not talked about, no mention in exchange announcements as well.. Opens another market for sanghvi

3 Likes

Hi everyone, sharing my notes and key takeaways from the recent Q4 and FY26 earnings call of Sanghvi Movers Limited. The company has posted its strongest year yet, driven by high asset utilization and a very promising pivot to the Middle East.

Here is a breakdown of the business economics, sector tailwinds, and management guidance.

1. Financial Performance (FY26 & Q4)

The company has shown excellent operating leverage as utilization levels peaked.

-

Revenues: Q4 stood at ₹351 Cr (+31.4% YoY). Full FY26 revenue crossed the four-digit mark at ₹1,020 Cr (+36.9% YoY).

-

EBITDA: Q4 EBITDA was ₹143 Cr (+25.7% YoY). FY26 EBITDA stood at ₹429 Cr.

-

Margins: Blended EBITDA margins are exceptionally healthy at ~40.1% for the full year.

-

Profitability: FY26 PAT came in at ₹184 Cr (+17.7% YoY).

-

Balance Sheet: Remains robust. Net Debt is at ₹612 Cr, translating to a comfortable Net Debt to Equity ratio of 0.47x. The average cost of borrowing is very competitive at 8.12%.

2. Operational Metrics & Business Mix

-

Asset Utilization: Fleet utilization averaged 79% for FY26 and jumped to 87% in Q4, indicating a very tight supply-demand environment in the heavy crane market.

-

Yields: Blended yield stood at 2.12% per month for the year (2.24% in Q4).

-

Segment Mix: * Core Crane Rental: 65%

-

Renewables / Turnkey EPC: 31%

-

Project EPC: 4%

-

3. The Middle East Kicker (High Margin Growth Engine)

The most interesting trigger for SML is its international expansion, specifically its subsidiaries in Saudi Arabia (KSA) and Qatar.

-

Massive Yield Arbitrage: While Indian crane yields hover around 2%, KSA yields are coming in at >4.5%.

-

Utilization: Cranes deployed in the Middle East are operating at 85% to 90% utilization.

-

Future Capex: Out of the planned CapEx for this year, a significant chunk (₹200+ Cr) is being aggressively routed to the Middle East to capture this high-margin demand. Operations have also recently commenced in Qatar to take advantage of regional shortages.

-

Management confirmed that the Middle East business has started generating positive monthly EBITDA and will be cash-flow positive soon.

4. Sectoral Tailwinds (Demand Drivers)

SML acts as a proxy for the broader heavy infrastructure and energy CapEx cycle in India. Management highlighted unprecedented visibility across sectors:

-

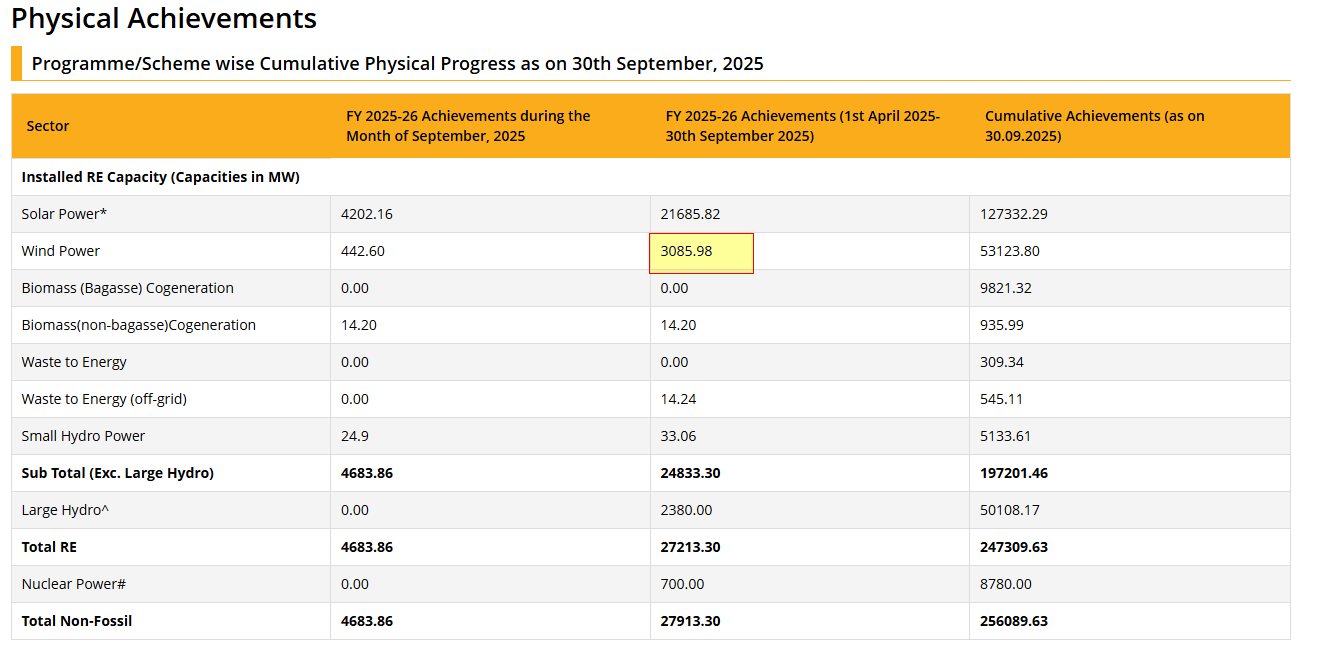

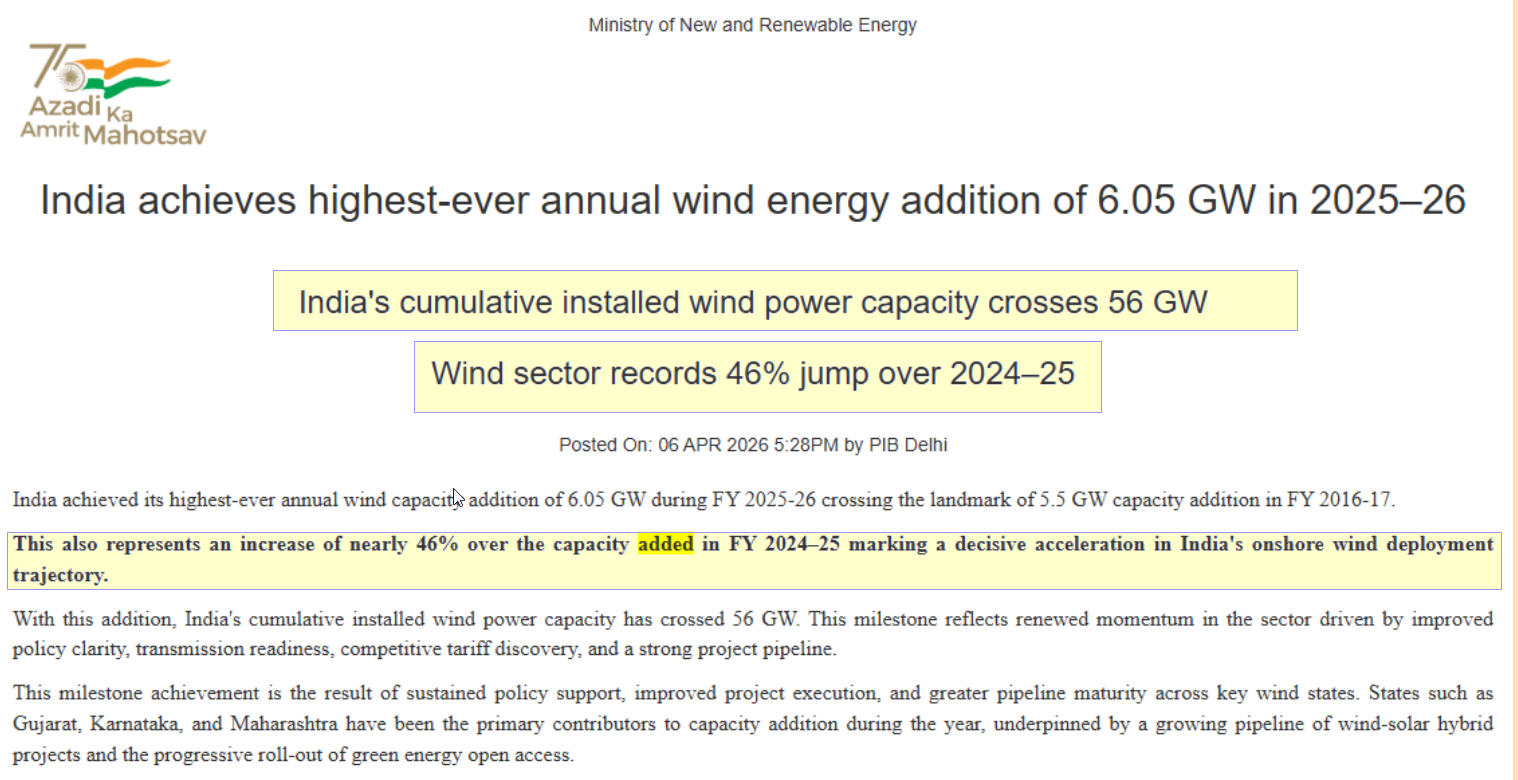

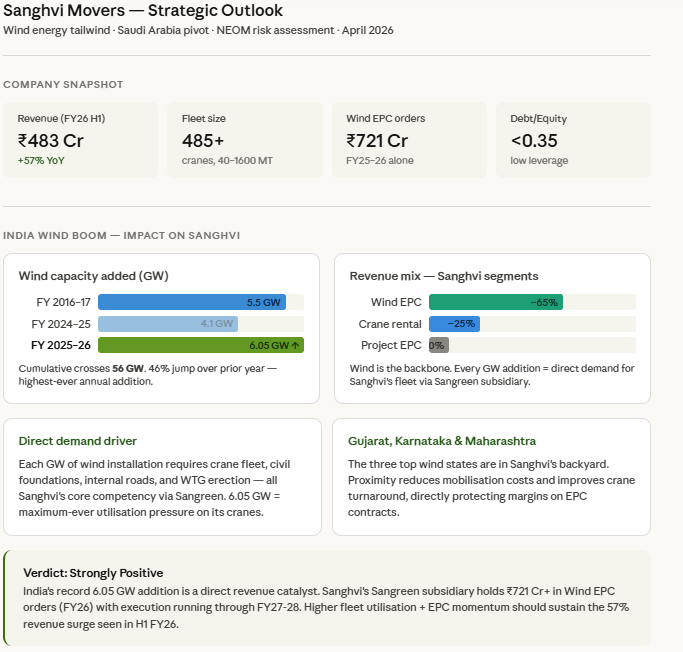

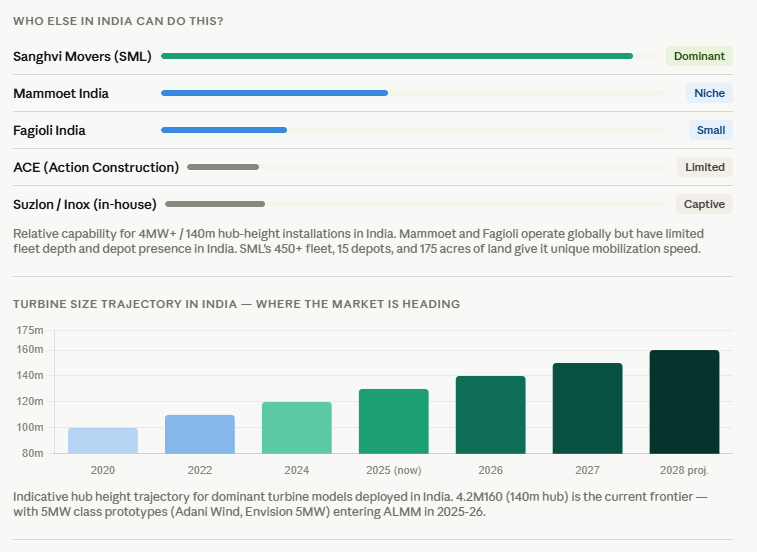

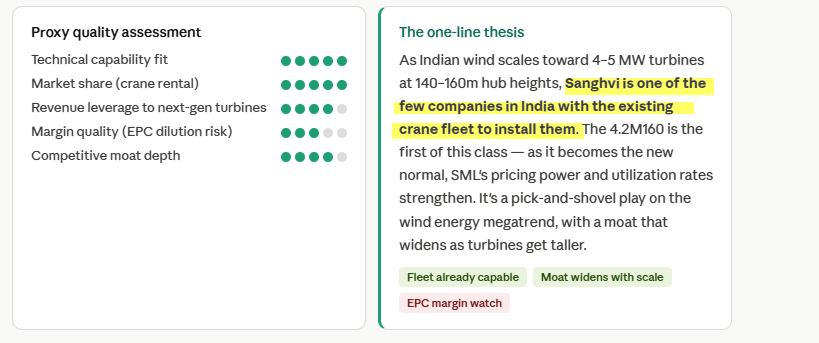

Wind Energy: India added 6.1 GW of wind capacity in FY26 (a 46% jump). The government target of 100 GW by 2030 guarantees multi-year visibility for heavy crawler cranes.

-

Thermal & Nuclear Power: Thermal capacity is expanding from 223 GW to 300 GW. Furthermore, the government has announced a ₹20,000 Cr mission for 5 indigenous nuclear reactors by 2033.

-

Refinery & Cement: Significant brownfield and greenfield expansions are underway, including major capacity additions targeted by 2030.

5. Order Book & Management Guidance

-

Visibility: The consolidated order book stands at ₹1,053 Cr as of May. The live inquiry pipeline is massive, at nearly ₹4,000 Cr.

-

Growth Target: Management is confident in maintaining the current ~30% YoY growth trajectory for both the top line and crane rental business in the upcoming year.

-

CapEx Execution: Total CapEx for FY26 was ₹474 Cr. Moving forward, the focus will remain on high-RoCE assets and Middle East deployment.

6. Key Monitorables & Risks

-

Margin Dilution from EPC: As the Renewables/EPC segment grows, blended EBITDA margins might optically compress (EPC is a lower-margin, asset-light business compared to core crane rentals). However, management noted that absolute EBITDA and RoCE will continue to improve.

-

Execution in KSA: Sustaining 85%+ utilization and collecting receivables efficiently in a new international geography will be a critical test for management.

-

Sector Concentration: While diversified, a significant portion of revenue is still heavily tied to the cyclicality of the Wind Energy sector.

Disc- Invested

2 Likes

Sanghvi’s middle east business is gaining momentum

1 Like