ICRA revised outlook from stable to negative…

Sanghi Industries -R-14022019.pdf (246.9 KB)

ICRA revised outlook from stable to negative…

Sanghi Industries -R-14022019.pdf (246.9 KB)

Any new updates in Sanghi?

Please share if anyone following it

I am looking forward to invest.

Remarkable Q3 results beating my EBITDA estimates handsomely - i have entered this stock taking a medium term view.

The management is confident of reducing earnings volatility and improving supply chain efficiencies.

This could be a 2021 doubler in my opinion.

Got interested with the company as they just completed an expansion project at Sanghipuram, Kutch. The expansion included 10000TPD clinker unit, 67 MW Thermal Power plant and a 2 MTPA cement grinding unit. The new unit commenced production in Febrary’21 behind schedule by a year due to covid related delay. With the new expansion project can the cement company post great results?The company has a price/book value of 0.78 and CWIP of 1262 cores as on Sept’21. Are we going to see the end of company’s production woes with the current expansion?

Poor past year performance

The company had a pretty poor FY’20, where sales went down significantly. The company faced severe production issues in the last FY. Company had to defer its annual maintenance to Q3 FY20 instead of seasonally weak Q2 due to heavy rainfall in its plant area. While the sale volume had improved in the initial part of Q4 FY2020, SIL undertook a second maintenance shutdown of its plant for 10-12 days in March 2020. Additionally, with the Covid-19 pandemic, the company’s plant was shut down since March 24, 2020, following the announcement of the Government’s national lockdown policy to control the virus spread Also Q4 ’20 was affected by lockdown. On the raw material cost front, The raw material cost per tonne of sale has increased by around 46% in FY-20 over FY-19. Due to production constraints, Company had to purchase clinker to maintain the sales in market. Hence, raw material cost increase includes around 1.16 lac tonne of external clinker purchased forming 31% of the cost. Company has captive power for its requirements. Power and fuel cost per tonne of sale marginally reduced by 1.6% in FY-20. The Company is importing coal at its own port with minimal inward freight. By blending higher quality coal with lignite, company is able to achieve improved consistency in production and better quality of clinker. The company can source lignite at competitive rates, given its proximity to GMDC Ltd.’s lignite mines.

Company’s locational as well as raw material advantages.

The company has its plant in Gujarat and 80- 85 % of the sales comes from Gujarat. The other two major states include Maharashtra and Kerala. SIL has an integrated cement production facility with easy access to high quality raw material, viz., limestone, at its captive mine about 3 km from its plant. Further, it has access to other raw materials like laterite, silica, clay and fly ash in the region with captive mines available for most of them. SIL has its own source of power with its 61.5-MW captive power plant (CPP) located about 10 km from the clinker plant and 2 km from the cement plant, adjacent to its captive jetty. The captive jetty allows SIL to directly import coal/pet coke for operating its CPP as well as for its cement operations. In terms of its fuel mix, it has the option to switch fuel source to lignite/imported coal/pet coke at both its CPP and clinker units, offering it the flexibility to control its energy costs depending on market conditions. The western India is traditionally a strong market for cement. Due to the captive jetty available the company is also exploring the possibility of export of clinker with the added capacity coming on stream. Company has also signed an agreement with Zuari for using its bulk terminal facility at Kochi port for packing its cement for usage in Kerala markets. Proximity to port can be considered an additional advantage for the company when it comes to export and reaching new market close to ports. SIL has also completed dredging activities at its jetty facility for enabling higher capacity ships/barges to voyage directly to the jetty.

Capacity Utilization

The company’s capacity utilization has been pretty poor (less than 50 %) in the past may quarters. Operational issues were one of the key factors, however, even during such dull quarters company was able to clock very good EBITDA/ ton close to 1000 due to good raw material management.

Debt

The company’s debt has moved from 771 crores in FY’19 to 1256 crores in FY’20 mainly due to the very large capex undertaken. Moreover the company has issues NCDs worth 305 crores for private placement on 23rd February for redemption of NCDs worth 256 crores issued in March’18. The NCDs carry a coupon interest of 14-16 %. In such a low interest scenario it’s not pleasant to see the company going for such high cost debt. The debt will be for a tenure of 6 years. The earlier debenture were at 10.5%.

To conclude it can be seen that the company has almost doubled its clinker capacity. The enhanced capacity has come on stream in Q421 when the country is seeing increased demand after covid unlocking, However the demand may have flattened with the 2nd wave. The company has advantages in the cost side due to its integrated nature of operations and proximity to raw material. The company has captive limestone mine, captive power plants etc. Also captive jetty will aid the company in imports of pet coke etc. and export of clinker as well. Digvijay cement has a similar market and had a revenue increase of 22 % in Q4’21 over Q3’21 with increased OPM margins. The capacity utilization along with debt reduction will be the key factors to watch out for.

Key risk:

The very high debt along with high cost of debt can be disastrous for the company if demand/ capacity utilization doesn’t pickup

Discl: Invested and biased, Not a recommendation

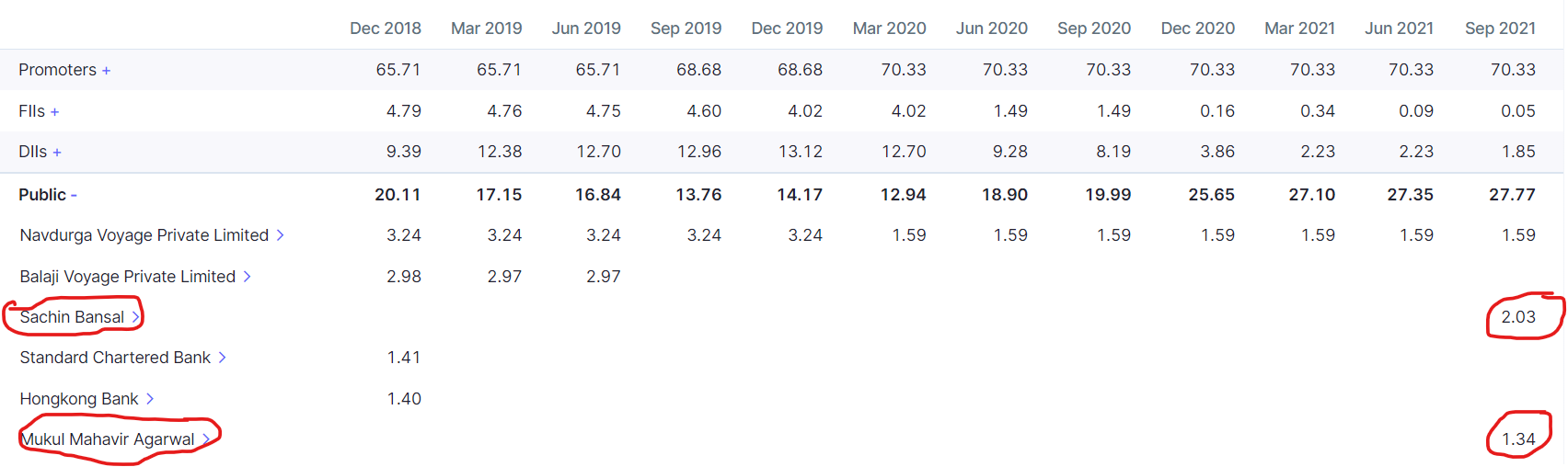

Couple of big investors have picked up stakes during last quarter

@hitesh2710 - Do you still hold Sanghi?

Q3 - Concall Summary

Full Conference call link - Sanghi Industries Ltd Q3 FY22 Earnings Call - YouTube

Disc - Invested, Biased

Why after huge capex, company is not able to generate revenue

Sub: Disclosure under Regulation 30 and other applicable provisions under

SEBI (Listing Obligations and Disclosure Requirements) Regulations,

2015, as amended (“SEBI (LODR) Regulations”).

This is to inform you that the board of directors of the Sanghi Industries Limited

(“Company”) met today (i.e., August 3, 2023) and inter alia approved the execution

of the share purchase agreement dated August 3, 2023 (“SPA”) amongst the (a)

Company, (b) certain members of the promoter/ promoter group of the Company

(whose names are set out in the Annexure, “Sellers”), and (c) Ambuja Cements

Limited (“Acquirer”). Pursuant to the SPA, the Acquirer proposes to acquire upto

14,65,78,491 equity shares of the Company (“Sale Shares”) representing 56.74 % of

the equity share capital of the Company, for a consideration of upto INR 114.22 per

Sale Shares (“Proposed Transaction”) subject to the terms and conditions mutually

agreed between the parties and recorded in the SPA. As a result of the Proposed

Transaction, the Acquirer will be required to make an open offer in accordance with

SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (“SEBI

(SAST) Regulations”). Subsequent to the board approval, the Company has

executed the SPA.”

Open offer triggered…

Can some one pls update if there is any other open offer after recent Abuja’s 50% acquisition?

Any view on the company as open offer was at 120 and stock is currently available at sub 90 levels

Background: Sanghi Industries Limited was the flagship company of The Ravi Sanghi Group dealing in the production and distribution of Cement under the Brand Name “Sanghi Cement”. Sanghi Cement was commissioned in 2002 with one of the world’s largest single stream Cement Plant located at Sanghipuram, in the Abdasa Taluka of Kutch District of Gujarat State. This plant is fully automatic with state-of-the-art technology from Fuller International, USA.

It is ranked as the second-largest cement plant in one location in India. It is one of the top three players in Gujarat and is also increasing its presence in Maharashtra, Rajasthan and Kerala. The co. has one manufacturing facility located in Sanghipuram, Gujarat. It also has a 130MW captive thermal power plant, captive mines, a water desalination facility, and a captive port in Kutch that can handle 1 mmtpa of cargo. Currently, SANGHI operates with a 6.1 million tonne grinding capacity and 6.6 million tonne clinker capacity, boasting a substantial limestone reserve of 1 billion tonnes and proximity to lignite resources.

The company grew its capacity aggressively and largely funded it through debt. The debt almost doubled from ₹ 770cr on 31 March 2021 to almost doubled to ₹1,550cr on 31 March 2023. Fuel cost was historically higher than peers for Sanghi and it used a mix of Coal and Lignite. Sanghi faced environmental clearance issues in the procurement of lignite which resulted in a change of power and fuel mix to be more dependent on Coal. With coal prices spiking up in 2021-2023, the margins to a further hit. COVID severely impacted the company’s operations, impacting dispatches due to a weak demand scenario, and the new 4mtpa clinker capacity was delayed and the 2mtpa grinding unit was deferred by almost two years.

The company was stuck in a deathly loop of poor cash flow generation, mounting debt, low dispatches, increasing costs, lowering margins and poor capacity utilization at almost 25%. The weakening debt metrics resulted in the company refinancing its existing NCDs from 10.5% to as high as 15-16%, with the overall finance cost ballooning to as high as almost 20% in FY23.

Strategic Acquisition by Ambuja Cements: In August 2023, Ambuja Cements Ltd. announced the acquisition of a majority stake in Sanghi Industries at an enterprise value of ₹5,185 crore to buy a 56.74% stake in Sanghi Industries from Ravi Sanghi & family and the transaction was completed in December 2023. The acquisition was done at ₹121.9 and Ambuja made the mandatory open offer at ₹114.22 and later increased to ₹121.9 an incremental 7.93% stake was added by Ambuja from the public through an open offer. Currently, Ambuja owns a 62.4% stake and Ravi Sanghi & family owns about 15%. Ambuja recently decided to sell almost 2% in the open market to comply with the minimum public shareholding norms, indicating that Ravi Sanghi & family’s stake is unchanged.

Steps taken by the Adani Group:

Supply Agreement- Sanghi has entered into a Master Service Agreement with ACC and Ambuja for the Sale of Cement, Clinker and allied products. ACC and Ambuja will bulk purchase Clinker and Cement produced by the company, which will then be sold under the AMBUJA/ACC brand. With this arrangement, the company is expected to improve its capacity utilization to around 80%. The company will receive advance payment along with the purchase order, the same will be used for the working capital and smooth operations and Sanghi will not have any financial constraints in the future. The pricing of the above arrangement will be "Manufacturing Plant’s Cost of Production (excluding Interest and depreciation) of previous Quarter, plus 10% markup. Adani Group believes this will improve the company’s EBITDA margins to 9%. While the duration of this agreement is not clear, shareholders’ approval has taken till FY25 for Rs. 2,000cr.

Financial Assistance- Sanghi’s debt as of 30 Sept 2024 stood at ₹ 1,828cr. Ambuja has already provided an unsecured loan by way of ICDs of ₹ 2,100 cr, at 8% interest rate, which has been utilized for repayment of high interest-bearing secured debts and to meet the other working capital and business needs. Additionally, it is proposed for Ambuja to extend another unsecured loan by way of ICDs of up to Rs. 500 Crore at an 8% interest rate, which will be utilized by Sanghi for working capital requirements, plant balancing and refurbishment, IT up-gradation, initiatives towards ESG, improve evacuation infrastructure and other general corporate purposes. Therefore, Sanghi will have no financial constraints in the future.

Expansion Plans and Vision: Under the Adani Group, the company has ambitious expansion plans. The promoters are set to debottleneck the grinding capacity, adding 3.9 million tonnes with a waste heat recovery system, projecting a minimal capex of ₹ 500 crores by March FY24. Post this enhancement, the total capacity will reach 10 million tonnes annually.

Additionally, the company plans to invest ₹ 3,000 cr to augment grinding and clinker capacity by 5 mt, scheduled to be operational by FY26. The promoters aim to deepen and expand the captive port capacity to accommodate larger vessel sizes, fostering synergies with another promoter-led company, Adani Ports, to implement an efficient coastal transport strategy.

Analysis: This is a special situation case, with a potential turnaround in operations being the trigger for the re-rating of the stock. With the financial support being offered by Ambuja, the liquidity challenges of Sanghi have been completely eradicated. The supply agreement with Ambuja will result in a swift improvement in capacity utilization to almost 80% from the current 25%. However, in the short term the operating margins will be capped as the projected EBITDA from the arrangement should be around 9%, which is low, given the average EBITDA margins for the company were historically in the range of 15-16%.

In the short term (6-12 months) assuming no improvement because of capex, the company should be able to reach around 80% capacity utilization, which will bring it back to profits and will start generating free cash flows. Over three years, once the production capacity is increased to 15mtpa and assuming 80pc capacity utilization, the company will be similar to the size of JK Lakshmi with an enterprise value of around Rs. 10,000cr. The company can clock revenues of ~Rs. 7,000cr and EBITDA of Rs. 1,000cr, estimated EV/EBITDA ratio of 10x, the EV should be ~ Rs.10,000cr.

Key risks to the investment:

Conclusion: This is a special situation case, with a potential turnaround in operations being the rationale for investing. The acquisition has fixed the liquidity issue for the company, smoothening the track for expansion and improving its profitability and capacity utilization.

Disclosure: Invested

The company has decided to issue preference shares of Rs. 2200cr with a dividend rate of 8%. Looks like this will be issued to Ambuja Cements to replace it with the debt it refinanced recently. While this is neutral from a net cash flow perspective, but with the interest cost falling by about Rs. 150-160cr, it should immediately put the company into profitability.

Disc: Invested

Best Regards

Shobhit

Looks like Sanghi wont get much out of this.

Correct, but how can we expect turn around keeping the same scenario in place. Growth is there but the cash flow is designed to go to Amubuja’s pocket. Isn’t it ?

With a plan to unify all cement operations under a single entity to streamline operations, how would this scenario play out for Sanghi?