SANDUR MANGANESE

BACKGROUND

Sandur was set up in the year 1954 in Karnataka by Mr. Y.R Ghorpade, the former ruler of the princely state of Sandur. It is the fifth-largest iron ore miner in Karnataka and the largest private miner of manganese ore in India (overall 2nd largest manganese ore miner in India, next to PSU - MOIL).

Sandur has lease deed over land of 3215ha with forest clearance for 2000ha. They have a mining limit of 1.6 Million MTPA of Iron Ore and 0.55 Million MTPA of Manganese (Mn) Ore (even though they have been mining 0.28 Million MTPA for the last several years). The estimated reserves of these mines according to the latest EC documents are ~102 Million MT of Iron Ore (which is 48x current annual permissible capacity) and 13.35 Million MT of Manganese Ore (69x of current annual production), valid till 2033.

Promoters hold 73% stake in the Company.

MAIN PRODUCTS/SEGMENTS

(a) Mining of Manganese and iron ore (running at 100% utilization)

- Manganese Ore 0.28 Million MTPA - partly used for captive purposes in ferro alloys and rest is sold in the open market.

- Iron Ore 1.60 Million MTPA - Completely sold out, no captive uses right now

- Sandur mainly has low to medium grade Iron Ore and Mn Ore fines and lumps.

(b) Ferro alloys and power

- Ferro alloys 48,000 MTPA of silico manganese (primary product)

- Thermal Based Captive Power generation of 32 MW (currently not operational).

(c) Coke and Waste Heat Recovery.

- Sandur did a capex between FY19-FY21 where it set up a 400,000 MTPA Coke Oven plant along with 30MW Waste Heat Recovery Boilers (WHRB).

- Coke Oven Batteries got commercialised in Jan’21 and has been operating at >100% utilisation.

- The steam generated from the Coke Oven Plant is recovered using WHRB to generate power for captive consumption in the Ferro Alloy Operations.

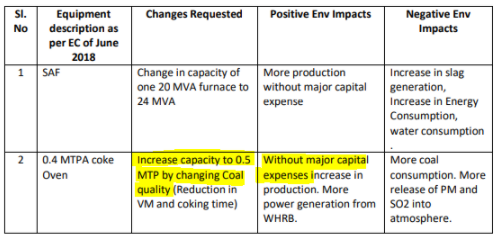

Large Expansion in recent years -

(a) Coke Oven & WHRB (Already commissioned)

-

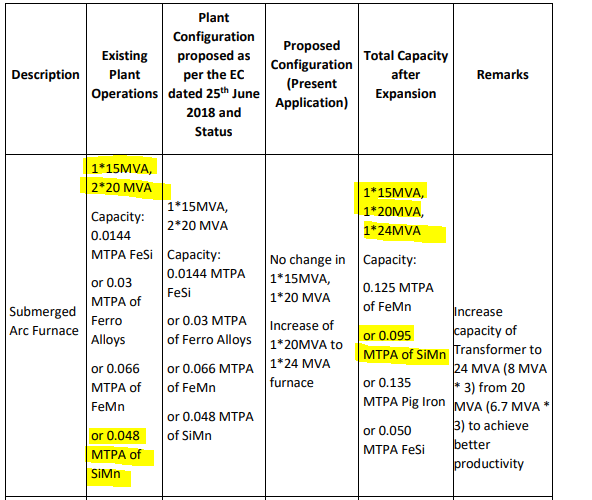

Coke Oven & WHRB with capacity of 30MW Power Generation- Sandur did a 600cr capex where it set up 400,000 MTPA Coke Oven Plant, 2 WHRB to generate 30MW power for the power intensive Ferro Alloy Operations, and increased its Ferro Alloy capacity from 36,000 MTPA to 48,000 MTPA by setting up a new 24MVA Furnace and refurbished the existing 20MVA Furnace. This entire capex commercialised in Jan’21.

-

Sandur currently has a 50% assured off-take with a Steel manufacturer in Karnataka for Coke on a fixed cost conversion basis - this will ensure fixed margins and reduce volatility to some extent. Rest is sold to other Steel players in the open market.

-

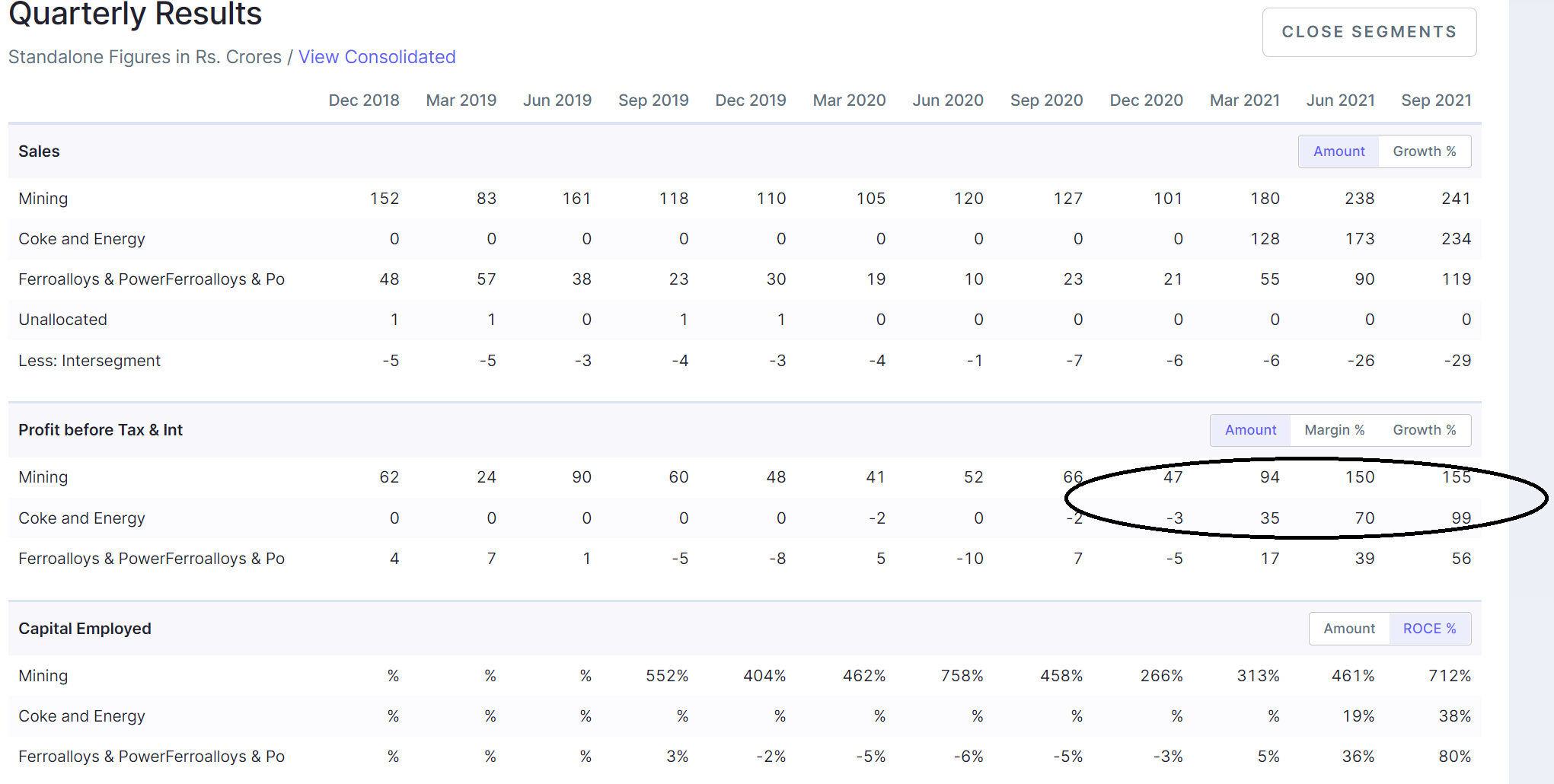

Overall, while mining was a high profitability and high ROCE business, the ferro alloy business was a drag on the performance due to high cost of power. Sandur has corrected this through capex on WHRB which has resulted in significant increase in profitability since Q4 FY 21. In H1 FY 22, as much as 50% of EBIT is from non-mining business.

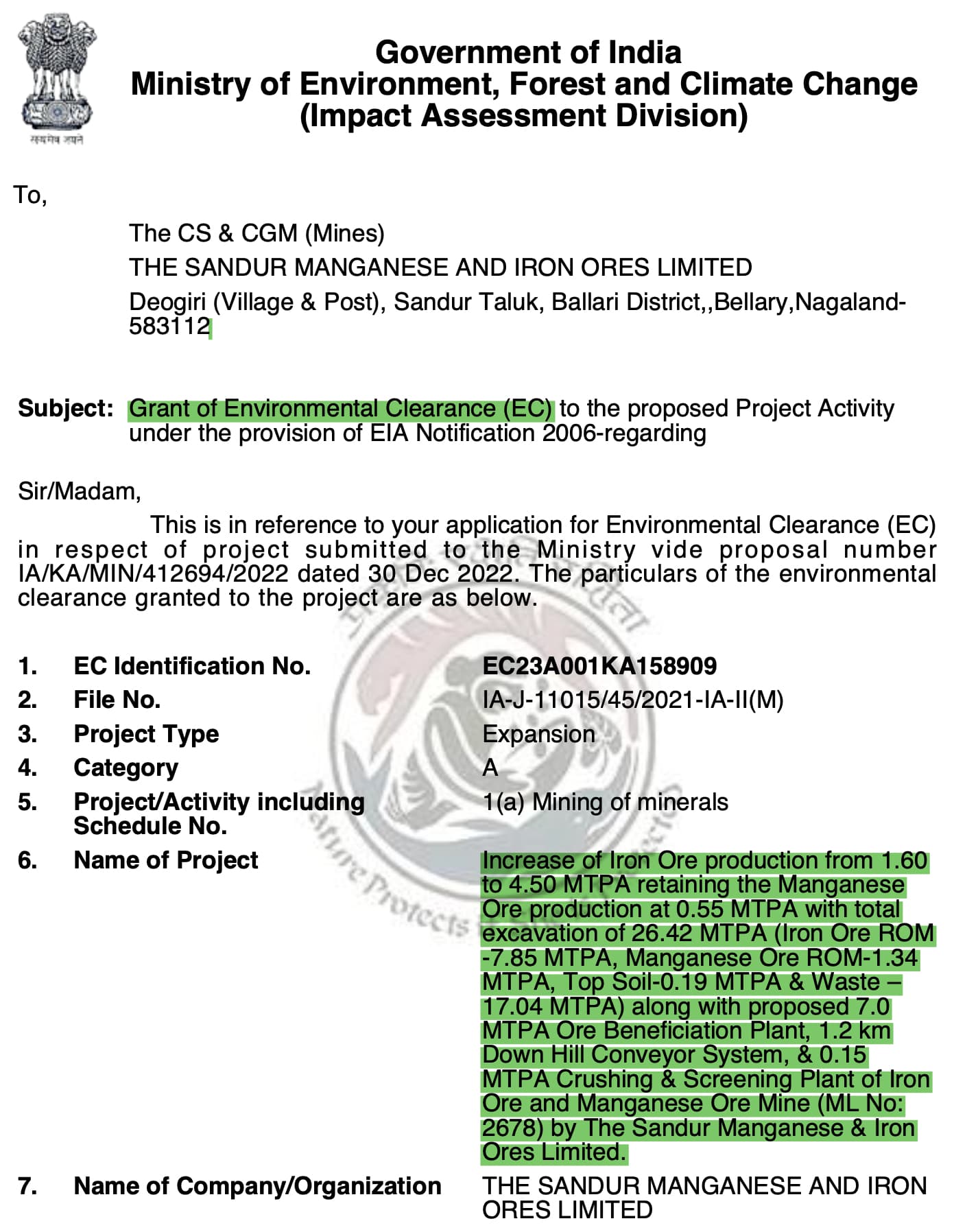

(b) Iron ore expansion (in final stages of EC)

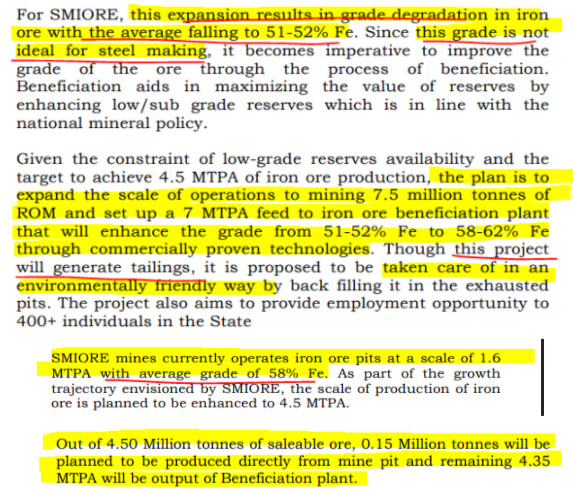

Sandur has been for long trying to increase its permissible Iron Ore mining limits from 1.6 Million MTPA to 3.85 Million MTPA. Due to past issues in the mining sector in Karnataka, they haven’t been able to increase their Iron Ore mining production. They were in the final stages of doing this but they were recommended Public Hearing by the EC committee. Following this, they amended their initial plans and have now applied an EC to increase the mining limits from the current 1.6 Million MTPA to 4.5 Million MTPA. Key point to note is that via amendment, they will now be increasing the extraction of iron ore by 5x to 7.5 Million MTPA and will beneficiate the output and sell 4.5 million tonne of better quality iron ore. This is better as the quality of ore would have depleted on further mining.

With this proposed expansion (pending EC), the company is expecting 2.8x volume expansion with growth in realisation as well as their current average grade is 58%. They will use the beneficiation plant to churn out higher grade Ore. Therefore, the value growth in Iron Ore can be 3 - 4x.

(c) Future Capex- (awaiting EC approval)

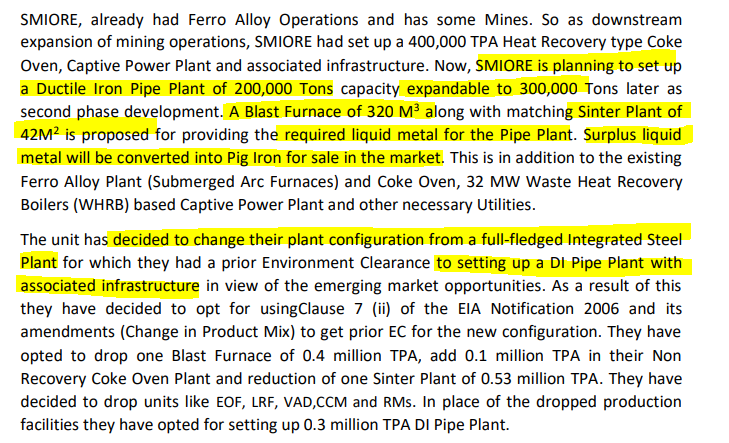

Sandur initially had a plan to set up a 1 Million MTPA steel plant but according to the recent EC filings, that has been revised and they plan to set up a Ductile Iron Pipe Plant of 200,000 MTPA capacity expandable to 300,000 MTPA later as second phase. This will be supported by Blast Furnace and Sinter Plant. Given that they have Captive Iron Ore and Coke, this project will be almost entirely backward integrated.

The idea behind forward integration is that when Sandur’s mines go up for auction in 2033, they will be in a position to secure the rights by showing the mine as a captive mine, though they will have to pay the premium as per the market scenario at that time. This also helps in mitigating concerns over sustainability as pure play merchant mining company.

-

In this capex, they will also increase their Coke production to 500,000 MTPA from 400,000 MTPA currently. This will be without any major expense and will also lead to More power generation from WHRB.

-

In this EC they have also applied to almost double their Ferro Alloy operations. The management mentioned in Q4FY21 concall that they have a 3rd furnace available which can take the capacity to 70,000 MTPA with a minimal capex of 15-16cr. The key bottleneck is power and having burnt their hands in the past, they want to expand further only if they can arrange cheap power.

-

The timeline and cost of this project hasn’t been announced by the management and this is a new development. The estimated cost as mentioned in the Form-1 of the EC filing is 900cr. We take this number with a pinch of salt unless confirmed by the management.

Source- EC Document

MAIN MARKETS/CUSTOMERS

The company sells its entire Iron Ore & Manganese Ore through e-auction. Therefore any registered customer on the MSTC portal can participate and buy their Ore. The Karnataka Govt. has imposed a ban of exports of Iron Ore and therefore, the company generates 100% of its Iron Ore revenues domestically. Since transporting Iron Ore & Mn Ore is expensive, most of their products are consumed in and around Karnataka.

For their coke operations, as mentioned earlier, they have an assured 50% off-take on fixed cost conversion basis while the rest is sold in the open market. Similarly, Ferro Alloy is also sold in the open market. The major customers for most of their production output are Steel players.

CURRENT MARKET/INDUSTRY TRENDS

-

Iron Ore Mines Auction- According to the MMRDA Act 2014, renewal of mine lease will be done through auctions. A total of 48 operating mines had expired as of Mar’20 and went up for auction. A lot of mines in Odhisa have been bought at a premium of 120-140% over the market price in some cases. The miner will have to pay the premium to the Govt. on the prevailing Iron Ore prices in that region. Due to this, there has been a structural shift in Iron Ore pricing in India since Steel players who acquired mines for captive use in the recent auctions will be paying high premium on their Ore extraction.

-

NMDC Royalty- In addition to the mining auctions, Govt has imposed very high royalty on NMDC’s Iron Ore who is the price setter in the industry and this has artificially pushed domestic Iron Ore prices higher. NMDC will have to pay a premium of 22.5% of average selling price (in addition to existing iron ore royalty payout of 15%. Therefore, even though prices are very high compared to past levels, they are not expected to revert to past lows.

-

The primary factor responsible for the global manganese market’s growth would be increasing use in lithium-ion batteries and the rising global shift towards electric vehicles running on them. Manganese also has applications in steel manufacturing. It is used as an oxidising agent that enhances steel’s hardenability and tensile strength.

BULLISH VIEWPOINTS

-

Sandur’s coke oven and WHRB capex of 600cr has been highly profitable. They got lucky due to the high pricing environment and they are on track to recover this 600cr within 2-2.5 years of commercialising. They took huge debt in FY20 (for their BS size and having remained debt free) and are already net debt free.

-

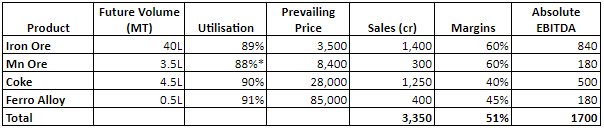

Iron Ore Expansion Cost, Timeline, & Rough estimates Mining is a high margins and high ROCE, cash generating business. Margins are a function of output and commodity pricing, even in a low price environment, Sandur manages to clock 25-30%+ EBITDA. (also evident in high EBITDA margins in Q1 FY 21 margins at time of peak Covid wave 1)

They are doing a large expansion in iron ore mining. Further details on their mining cost and how profitable this expansion will be-

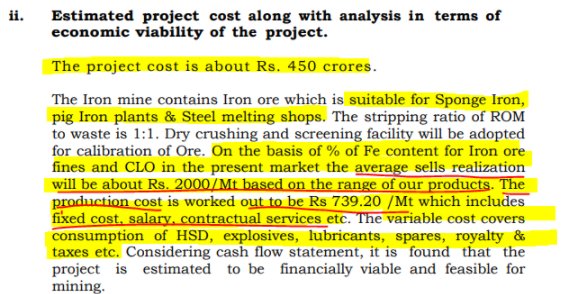

Source for all these images- EC Document

-

It has been mentioned in the Concalls and AGM that Iron Ore production can be expanded very quickly with only minimal capex. The major capex will be towards the beneficiation plant now. The cost of this project as mentioned in the EC document is 450cr. Management’s estimates are awaited.

- Back of the envelope calculations illustrate the attractiveness of this expansion:

Assuming, iron ore price @ Rs 2,500 per tonne (compared to average Rs 4500/tonne in Q2 FY 22)

Increase in iron ore conservatively, say 3MT @ Rs 2,500 / tonne = Rs 750 crs additional topline.

Incremental PBIT (existing margins Q2 FY 22 was 64%) - Assume 45% = Rs 340 crs per year with capex of c. Rs 450 crs - Very High RoCE.

- Back of the envelope calculations illustrate the attractiveness of this expansion:

- Manganese Ore expansion- Sandur has a Manganese Ore mining permit of 0.55 Million MTPA but has been mining only 0.28 Million MTPA over the last few years. Management has indicated that they plan to increase production for Manganese Ore as well, once they start their Iron Ore expansion.

BEARISH VIEWPOINTS

-

Delay in EC approval for iron ore expansion due to public hearing etc. - This is the biggest risk in the thesis. There have been long delays till now.

-

Sandur’s products are commodities and prices are cyclical in nature. There is a risk that prices of commodities revert and fall dramatically while Sandur comes up with its expansion.

-

De-link of Karnataka iron ore prices from international prices (as exports not permitted).

-

Sandur produces lower grade ore reflective in lower realizations vs NMDC (and hence benefication plant)

-

50% of coke is sold on cost plus basis to a South based player (which we suspect is setting up its own coke oven capacity in 1-2 years) - Offtake of coke is important for viability of ferro operations since if Coke is not produced, steam will not be generated for Power. Management does not see this as a risk since there are many Steel players in the South and coke is imported in India.

-

Large phase 2 Capex of DI Pipe - execution risk and a lower RoCE business compared to mining.

-

Large contingent liabilities - Ongoing disputes of income tax (Rs 69 crs) and forest development tax (Rs 68 crs)

-

Young MD- The current MD is around 30-years of age. He has been associated with the operations since 2015 in multiple roles. He became the MD in June’20.

-

Government Regulations and Intervention- Sandur operates in an industry which is highly regulated and there is a lot of Govt. intervention. Their operations were disrupted in 2011 and 2012 when the Supreme Court had ordered suspension of all mining activities in Karnataka.

INTERESTING VIEWPOINTS

- Iron ore business is a cash cow for them with very high RoCE and a large expansion is coming here. So, even though current numbers look unsustainable on the face of it, beginning FY24, Sandur can generate much higher EBITDA than what it has ever generated..

- Ferro alloy operations have turned around and along with Coke contributed 50% of profits in H1 FY22. Even though margins may normalise here, they are expected to remain above 20% in normal scenario.

- Promoter pledge on shares to banks c. 51% shareholding (on debt raised for Phase - 1) was released in Dec’21.

- It was a sleepy company till 2019 with not much of growth. It was being professionally managed. Afrer 2 decades the next generation of the promoter family has got involved in the business and are doing expansions to grow the business and unlock the huge asset base they have had being a 100 year old company.

BARRIERS TO ENTRY

The non-mining business is capital intensive. The mining operations require a mining lease that is granted by the government which creates a huge barrier for new entrants. Other than this, it is a commodity business.

BUSINESS MODEL

-

The model is fairly simple. The govt. assigns the mining limit. The company has a mining cost, beyond which, everything flows to the bottom line. Mining is a very high margin business if done well, although it is directly linked to the volatility in Iron Ore, Mn Ore, and Silico Manganese prices which in turn is linked to the performance of the steel industry and level of economic activity in the country and globally.

-

For the non-mining business of Coke and Ferro Alloy, the key input is Coking Coal which is a volatile commodity. 50% of the current Coke production is sold on a cost plus basis to one customer and the rest is sold in the open market. The pricing and volumes here are also decided by the performance of the steel industry and level of economic activity in the country and globally.

VALUATION MODEL

- Market Cap- 2200cr

- Cash & Current Investments- ~820cr with Debt of 340cr.

- EV- 1700cr

- Taking conservative estimates (with prices lower by c. 35%-40% compared to prevailing prices), Numbers post completion of Iron Ore expansion could look like this-

*Manganese Ore capacity has been assumed to increase from current 2.85L to 4L (mining limit is of 5.5L).

However, if we estimate the numbers based on current prices, this is what they look like-

The above numbers do not include DI plant projections.

On the lower end of assumptions (660cr EBITDA), Sandur is available at 2.6 times FY24E EBITDA at today’s EV.

CORPORATE GOVERNANCE SCAN

-

The company is one of the few 5 star rated private mines in India with an exemplary track record. In an industry which attracts a lot of negative attention, SMIORE has always been in the good light.

-

In 1994, during the 2nd renewal of mining lease, Sandur had surrendered 1500 HA of forest area for forest conservation. This was well appreciated during the Supreme Court judgement related to the Karnataka Mining Scam in 2011.

-

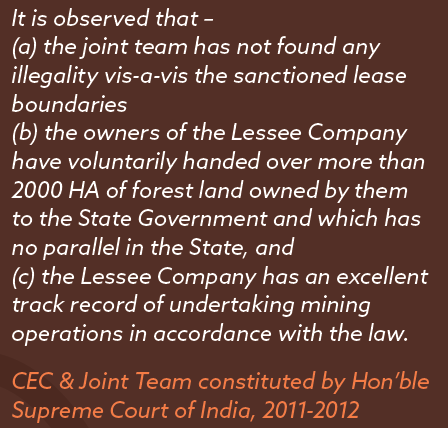

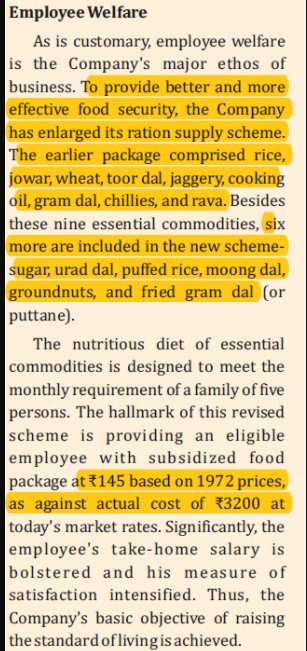

Excellent work environment- The management takes care of its employees. They provide subsidised food to employees and never faced problems since inception as per Annual Reports.

-

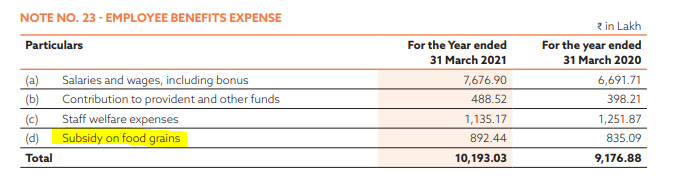

Mine closure provision- The company has provided for mine closure. Even very large miners like Hindustan Zinc does not provide for the same. Once mine operations are over, there is a huge cost involved to surrender the mine back to the Government.

RED FLAGS/FORENSIC SCAN

- No major related party transaction

- KMP remuneration, although a little high, is stable

- No negative surprises in Ind-As transition

- Strong cash flow conversion

DISCLOSURE(s)

Ayush Agarwal: Invested

Yachna Bhatia: Invested

Reference docs:

Investor ppt Q2 FY 22.pdf (3.8 MB)