Sandhar Technologies Limited

BSE: 541163 | NSE : SANDHAR | SANDHAR: IN

Sector - Auto Ancillaries | Industry - Auto Ancillaries

Cyclical, Growth, ROCE expansion.

Elevator Pitch: Depressed ROCE, OPM caused due to short term RM costs elevation(passed with 1 quarter lag) likely to turn up disproportionately on the back of higher OPM and sales growing quicker than capital employed.

Business Overview

Sandhar Tech is a diversified OEM supplier to mostly Indian Auto companies. Sandhar is the sole supplier/single-source supplier of lock sets and mirror assemblies to Hero MotoCorp Limited, TVS Motors Limited for motorcycles and Honda Cars India Limited. Moreover, it is a single-source supplier of wheel assemblies to TVS Motors Limited and Eicher Motors Limited (Royal Enfield), and operator cabins for excavators to JCB India Limited. Management has over 3 decades of experience in OEMs.

Highly diversified in product offerings, with locking systems and aluminum die casting (ADC) each contributed to ~21% of FY21 sales, with cabins (16%), sheet metal components (19%), vision systems i.e. mirrors (8%) and others (13%) following suit.

Concentrated client base especially in the 2 wheeler segment, with 50% of revenues coming from TVS motors and Hero Moto Corp. They do, however, have decadal relationship with many of their clients.

Segment-Wise revenue - 1. 2 wheeler - 54%, 2. 4 wheelers - 24%, 3. OHV & Tractors - 16%.

Geography Split - 86% from India, 14% from Spain(by subsidiary).

As the company services the Auto industry(particularly 2 wheeler and 4 wheelers) it is dependent on the cyclicality of the auto industry. I would classify it a shallow cyclical(although it does usually outperform the industry and its client’s performance). As far as the thesis goes, increasing wallet share and product launches will be considered the main growth levers rather than the auto cycle uptick.

Variant perception

-

Company had guided for 30% growth in topline this year, which has not been achieved on account of general de-growth throughout the auto industry. They grew about 24% as against 25% for the industry. Such growth can now be expected for FY23 and FY24.

-

Company also faced major RM cost headwinds with OPM dropping to an average of ~8% for FY22. Once RM prices(Zinc, copper, nickel) cool off margins are likely to flow into low double digits.

-

ROCE also remains highly depressed. Stretched WC with NWC in FY21 being 212 crores which has now grown to 300 crores(note NWC = Trade receivable + Inventory - Payables). ROCE has also fallen from 9-10% to 8%.

-

High leverage for the short term(D/E has doubled to now) so capital employed is stressed for the short term.

-

Low float available in the markets. 70% with promoters, 16.5% in Institutional hands, only 14% in public. Also promoter, Jayant Dawar has constantly bought shares from open market, buying at average prices of 250 in the last year(1 crore in 2021, even more in previous years)

Strategy

- Company is aiming to increase wallet share from existing customers.

- Increase market share

- New product launches

- Increasing premiumization

- Commissioning new plants(capex of 350 crores), 43 plants in 2021 and to commission 7 new plants in 2022 to bring it up to 50. Current utilization is only 60%. Many of the new plants are booked 100%. Can bring in 800 crores.

- Company has a tie-up with more than 50% of new EV entrants. EV is insignificant to the company currently, but the growth of EV, company can hold itself.(<5%)

- International Markets now have higher margins than domestic. New plant in Romania to help with a betterment in margin profile for the business.

- Have taken debt inorder to capitalize inorganic growth opportunities. Stretched WC should get better and short term debt of 250 crores will be reduced.

Valuation

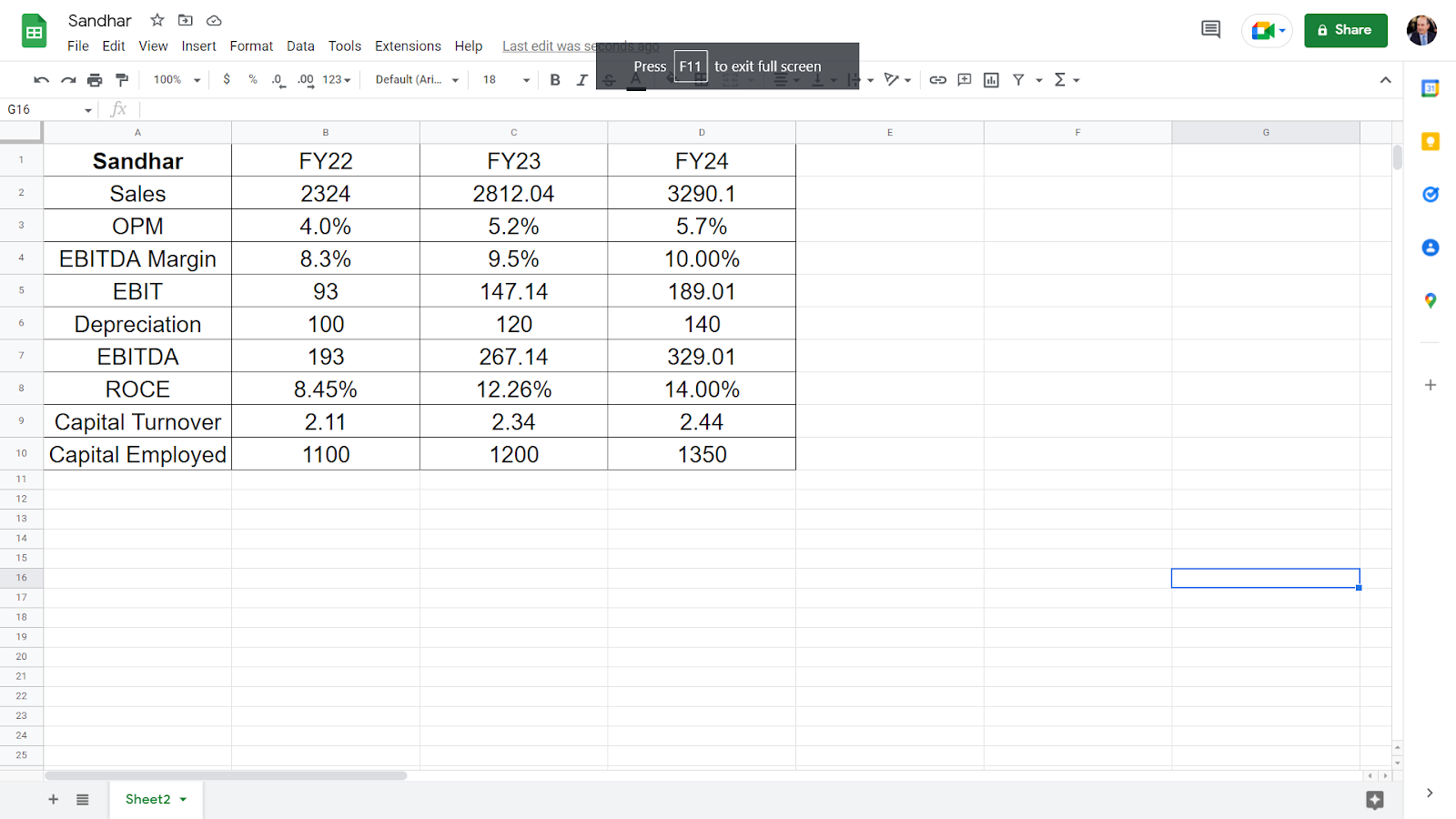

Currently the company trades at a market cap of 1500 crores. TTM EBITDA of 193 crores, EBIT of 93 crores. Trades roughly 15x EBIT.

Inputs - 21% growth in revenue for FY 23, 17% for FY24. Assuming EBITDA margin to rise to 10% by FY24 on the eventual cool off in RM prices, and prudent capital allocation by management to only produce high margin products. Capital Employed(NWC+NFA) is dependent on the CWIP which might go higher than I estimate and reduce ROCE.

ROCE(calculated as its dupont form - OPM*Capital Turnover ratio) calculated are very rough estimates to understand the trend, which should be taken with diabetes-inducing grains of salt. Capital turnover ratio(Sales/Capital Turnover) are shown to be trending upwards as I do believe that utilization rates will turn up and sales will grow quicker than the capital employed, i.e ROIIC will be high.

Both sides of ROCE(OPM & Capital Turnover) will work together, and cause a disproportionate increase in ROCE, and lead to a rich CFO generation.

Assuming the company is valued at 15x FY24 EBIT(Margin of safety baked in price as ROCE’s are likely to turn up so I’d say conservative enough), 2835 crores could be a fair value for the business. This again is built on a conservative take on management’s guidance, but still this is an imprecise art and therefore please do your own DD to evaluate whether or not the business can achieve it.

Catalyst

This begs the question why the company is away from fair value.

- I think the major catalyst for Sandhar is RM prices cooling off, as I believe the company has already delivered on top line growth as per the management guidance and will continue to do so. This should lead to a disproportionate rise in margins(higher than my numbers).

- Once the company delivers a little less than half of their 615 crores of debt. 250 crores is short term with an interest rate of 4.5%. Upon paying it off the company should see a rise in ROCE’s even more disproportionately as capital turnover goes up.

Exit/Risks

- RM costs will be a major risk for Sandhar.

- If the company levers itself even more, it would be a huge red flag.

- Look out for capital allocation and where they choose to use their money for inorganic growth opportunities. Also read new credit rating reports when they come out.