Samrat Pharmachem Ltd is a producer of pharmaceutical chemicals, primarily engaged in manufacturing of various types of Iodine compounds. The intermediates produced are used in pharmaceutical and chemical industries.

Samrat Pharmachem Ltd was incorporated on 16th June, 1992 at Ankleshwar in Gujarat State of India by Mr. Lalit Mehta and Mr. Rajesh Mehta. The founders of the company Mr. Lalit Mehta and Mr. Rajesh Mehta decided to focus on Iodine as the key ingredient for all their products with a vision to become the King in Iodine Chemistry. The Company has become a major supplier of Iodine Derivatives to the Indian and Foreign Market.

They are manufacturing Iodine compounds that finds its application in pharmaceutical, FMCG, Chemicals, Agrochemicals. Now the company has also entered new industries like Salt, Animal Feed, Textile & Tyre Cord Manufacturing segment.

Samrat Pharmachem is leading manufacturer of Iodine Salts. The company’s customers include several multi-national companies in India and abroad. (I could not find the list of customers)

The company exports its products to geographics like US, Europe, Africa, Asia, Middle East etc.

They claim that since inception, they have retained and added to its list of customers due its fair and human policies which ensure zero attrition rates of customers.

Products:

Di Iodosalicylic Acid - [Used in Animal Feed / Chemical / Pharmaceutical]

Ammonium Iodide - [Chemical / Pharmaceutical]

Cadmium Iodide - [Chemical / Pharmaceutical]

Calcium Iodate - [Animal Feed / Chemical / Food / Pharmaceutical]

Clioquinol - [Chemical / Cosmetics / Pharmaceutical]

Copper Iodide - [Chemical / Pharmaceutical / Textile]

Ethyl Iodide - [Chemical / Pharmaceutical]

Ethylenediamine Dihydroiodide - [Animal Feed / Chemical / Food / Pharmaceutical]

Hydroiodic Acid 57% - [Chemical / Pharmaceutical]

Iodic Acid - [Chemical / Pharmaceutical]

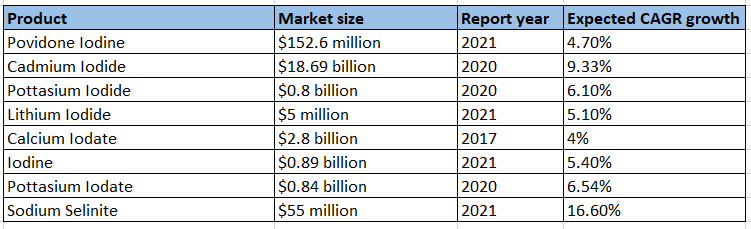

Iodine - [Agrochemical / Animal Feed / Chemical / Food / Pharmaceutical / Printing]

Iodine Monochloride - [Chemical / Pharmaceutical]

Iodoquinol - [Pharmaceutical]

Lithium Iodide - [Chemical]

Methyl Iodide - [Agrochemical / Chemical / Pharmaceutical]

N-Iodo Succinimide - [Chemical / Pharmaceutical]

Periodic Acid - [Chemical / Pharmaceutical / Printing]

Potassium Iodate - [Animal Feed / Chemical / Food / Pharmaceutical]

Potassium Iodide - [Agrochemical / Animal Feed / Chemical / Pharmaceutical / Textile]

Potassium Metaper Iodate - [Chemical / Pharmaceutical / Printing]

Povidone Iodine - [Pharmaceutical]

Selenium Dioxide - [Chemical / Cosmetics]

Sodium Iodate - [Chemical / Pharmaceutical]

Sodium Iodide - [Agrochemical / Chemical / Pharmaceutical]

Sodium Metaper Iodate - [Chemical / Pharmaceutical / Printing]

Sodium Selenite - [Animal Feed / Chemical / Pharmaceutical]

Tri Methyl Sulphoxonium Iodide - [Pharmaceutical]

Strengths of the company:

- The company has long presence of 3 decades in manufacturing of iodine derivatives and has developed keen understanding of market dynamics and healthy relationships with suppliers and customers. Over the years company has increased its product range catering to various industrial segments like pharmaceutical, fast moving consumer goods, Animal Feed, and Agrochemicals among other. Samrat Pharmachem is a leading domestic player its area of operations and generating healthy return on capital employed (RoCE).

- Samrat Pharmachem has moderate working capital cycle with gross current assets (GCA) around 3 months driven by receivables of around 2 months and inventory of around a month.

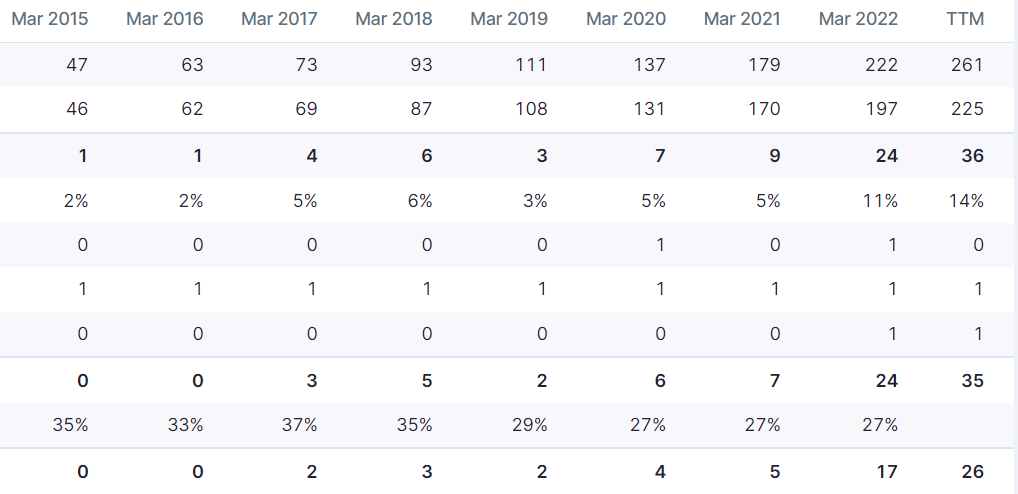

- Sales are growing consistently from 2015 onwards with OPM also improving.

Investment thesis:

- Company is consistently growing its revenue and its profits with OPM also improving.

- Company intends to double its turnover in a short period of time.

- Company is trading at reasonable valuation. With TTM P/E ratio of 8 and Mcap/S ratio of 0.78, company looks cheap. If they can maintain the same growth as Q12023, company is available at FWD PE ratio of 5.5.

- Company has ROCE of 52% for 2022.

- Very low debt to equity ratio of 0.16

- Promoter holding is reasonable - 49.65%

Risks:

- This is a microcap company with only 204cr Mcap as of today and could be very risky.

- As very less information is present about the company, not sure of the reason for increasing OPM in last 2 years.

- If this is complete commodity company, then if we invest now, we could be investing at the peak margin cycle and margins could come down in next few years.

- As per CRISIL credit report, there seems to be no entry barrier for the business. “The processing done by SPL is not much complex and can be replicated by others, restraining the profitability.”

- Since majority of procurement comes from the international market, any sharp fluctuation in forex rates affects procurement cost and accrual. This exposes the operating margin to fluctuations in forex rates. (From CRISIL report)

Disclosure: Tracking position (This is not a investment advice. Please do your own diligence.)

P.S: If anyone is tracking the company or have any information, please provide your inputs.