Growth AUM has to grow 3x+ to meet 1 lk cr target in 2 years. It seems super ambitious. What do you all think? I know they want to ramp up colending and all but is this achievable without deteriorating quality?

5 Likes

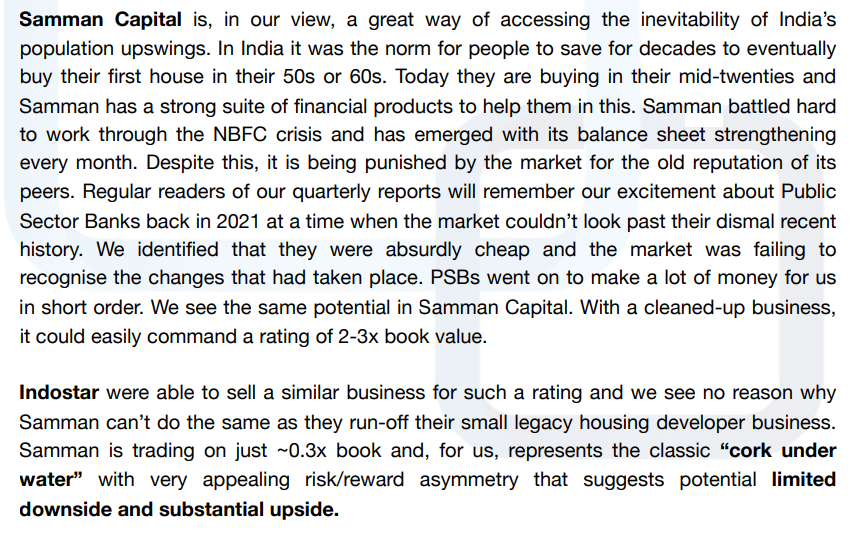

Very insightful info from Cohesion MK(fund managed by madhu kela sir) quarterly investment report

Disc - Invested

14 Likes

This is really very ambitious. I’m also skeptical. Management said this(Q4FY25 Concall) in this context -" on a goal of reaching a

Fiscal ‘27 growth AUM of Rs. 1 lakh crore, we are at Rs. 37,452 crores, still a long way to go.

But quite hopeful that as we scale up disbursals at both Sammaan Capital and Sammaan Finserve

and the AIF platform starts firing, we should be in a position to hit this number"

“The annual disbursals are trending along well. With nominal growth 20%-30% every year, we

should be able to achieve our target out there.”

I run this simple calculation

- Final Value = ₹100,000

- Initial Value = ₹37,000

- n = 2 years

CAGR=≈0.6434=64.34%

Need a CAGR of approximately 64.34% per year to grow ₹37,000 to ₹1,00,000 in 2 years.

What am I missing here?

Disc. Invested & planning to increase allocation.

3 Likes

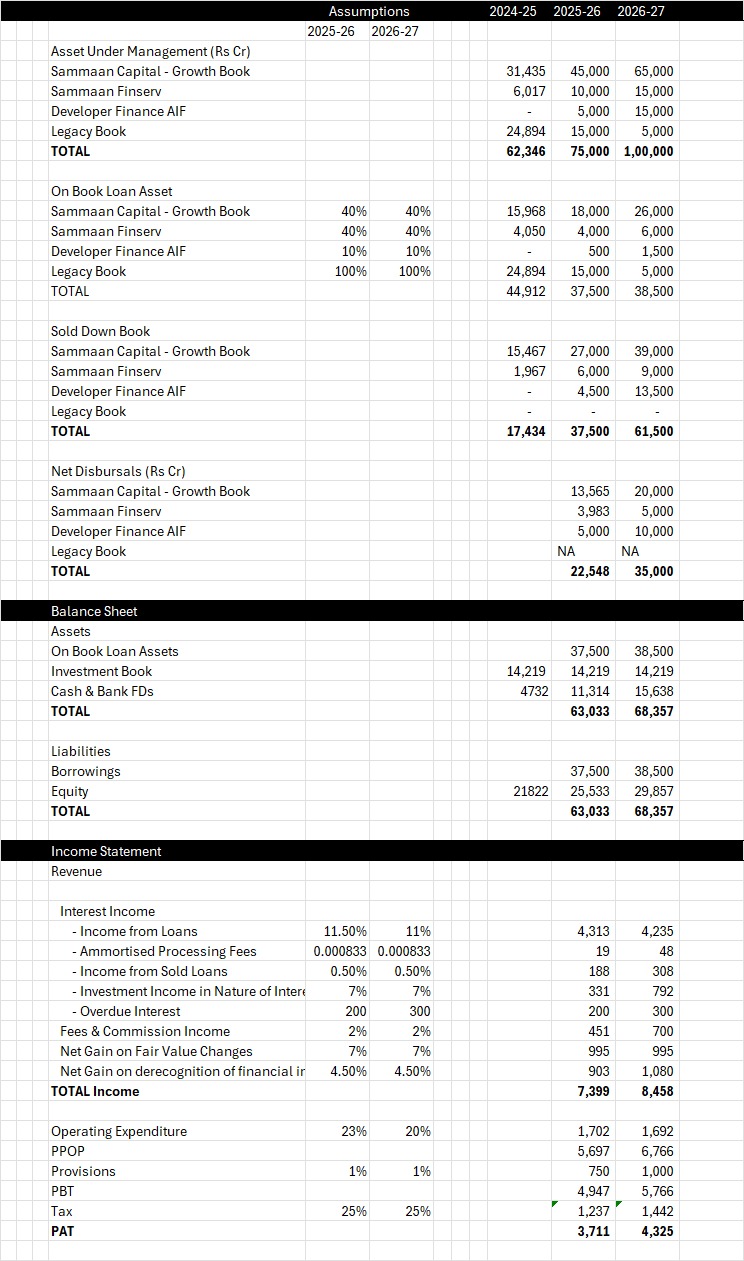

With the management detailing out the various income streams in the latest quarterly earnings update, here is a more detailed modelling exercise (than the one I shared many months ago) on the financial projections for FY2026 and FY2027. Wherever management has given a range for income streams, I have tried to take the lower end of the same. Similarly, fee income pertaining to new disbursals have been applied to net disbursals instead of gross disbursals to remain conservative.

No impact of write-backs from written off pool of loans has been considered.

Here is the outcome: -

The net profits for FY2026 and FY2027 are projected to be Rs 3700 Cr and Rs 4300 Cr respectively. Net Worth by FY2027 is projected to touch Rs 30,000 Cr. The excel file is attached herewith.

Sammaan Capital Projections.xlsx (12.6 KB)

Counter arguments and critique invited.

Disclosure: Invested with a substantial allocation. Views are likely to be biased

4 Likes

No finance cost on ~38k cr borrowings?

2 Likes

My bad! I had realized it just as you mentioned it. Have incorporated cost of funds @ 8.5% for FY2026 and 8.0% for FY2027. The operating cost will also reduce since it is a % of Net Interest Income. Here is the revised working.

Now the numbers are much more believable. Net profit touching Rs 2400 Cr and Net Worth touching Rs 26,000 Cr by end of FY2027. Excel is attached herewith

Sammaan Capital Projections.xlsx (12.7 KB)

7 Likes

Repo & CRR Cut – lumpsum Impact on Sammaan Capital

- Borrowing base: ₹52,297 Cr

- Current cost of funds: ~7.5% (typical NBFC spread over MCLR)

➤ Repo Rate Cut:

- 50 bps cut → assuming 60% transmission = 30 bps benefit

- Effective rate drops to ~7.2%

- Savings: ₹156.9 Cr annually (0.3% × ₹52,297 Cr)

➤ CRR Easing:

- Banks’ cost drops 10–20 bps → NBFC benefit ~10 bps

- Combined drop = 40 bps → borrowing rate ~7.1%

- Total savings: ₹209.2 Cr annually

➤ Pass-through to borrowers (20 bps):

- ₹104.6 Cr passed on (0.2% × ₹52,297 Cr)

- Net benefit retained: ~₹130 Cr

3 Likes

They will do a 25-30% CAGR and get growth AUM around 55-60k mark by 2027

100000cr is an exaggerated target, but even at ~60k cr and re-rating from current 0.5x PBV, cleaned up books, the stock will see a big jump!

7 Likes

Forgive my naivete but if it was this straightforward why wasn’t it done for all these years ? This Co has existed in a previous avatar for almost 2 decades. Granted that this is a change of strategy & direction post the rebranding (of sorts), but I see that the senior mgmt. team is largely unchanged. Growth targets with large AUMs and cleaned up books on a long term, sustained basis are easier on slide decks than reality.

11 Likes

June 10, 2025 Update

Unsecured creditors have officially approved the Scheme of Arrangement as directed by the NCLT. This is a key structural step for Sammaan as it moves forward with the consolidation of six legacy group entities into the main company.

This merger simplifies the group structure, cuts administrative overhead, and fully distances the brand from the Indiabulls legacy. It also improves transparency, governance, and operating efficiency. Over time, this should reflect positively in cost ratios and ROE.

No dilution, no restructuring — just cleanup. Now awaiting final NCLT clearance. Good step forward.

8 Likes

My channel checks point out to very easy approval process even to not so good customers. They do loans more than actual valuation by charging a premium in interest rates. The borrower is ok as he will stop paying after some time and get higher money than value of property, samman gives out loans as they hare happy collecting processing fees in tune of 2% and insurance in tune of 5-6%. Good borrowers move to banks or NBFCs giving better rates and bad borrowers keep crowding in. I wonder what percentage of such loans they give overvaluing properties. I have question marks as to their Underwriting quality.

7 Likes

Hey,

Disclaimer : more than half of my non cash position is in SCL, just trying to be devil’s advocate.

Great work on the projections, I disagree with them largely because if you read 2022 and 2021 transcripts you’ll realise that a “1 lakh crore AUM in the next 2-3 years” pipe dream has been sold to investors for a really long time now with Banga claiming to reach there by as early as 2025 (Per 2021 transcripts).

Since then, obviously there have been VISIBLE business changes and the growth AUM has increased by ~50% just this year which is an incredible feat I think. However, we don’t know the drivers yet and realistically from ~37,000 crores FY 25 growth AUM we can see a ~70,000 crore “real” book by 2028 and with SCL’s underwriting being untested in retail (Remember Indiabulls grew it’s AUM largely by scaling in bulkier builder loans and we know how that turned out) we don’t know the NPA’s we’ll see. Assuming a 2.5% ROA ( I understand while Banga claims 3% ROA there have been such claims in the past and it’s his job to paint a rosy picture so no blame there ) Reaching even a 2.5k crore PAT seems difficult, obviously these are conservative numbers but at this point I think a P/B of 2 won’t be too shabby for this sort of business getting a sort of 45% IRR if we get a P/B of 2, at a P/B of 1, an IRR of 26% won’t be too bad either but let’s hope for the best.

FYI : Take a look at the dilution and the ESOPs, SCL with a 8-10k crore market cap has raised more than 5,000 crores of equity within a year, with shares outstanding going from ~44 crores in 2021 to now ~68 crores, a 50% dilution. While currently on a per share basis the company at P/B of 1 might see a ~270 price per share any further dilution might screw investor returns drastically.

8 Likes

SCL has become my largest holding considering recent additions post its fall from Rights Issue level of 150.

Many negatives are there and only time can prove how stock behaves. Banga pictures a rosy outlook, outlook is bought by many institutions and many sitting on sidelines.

Growth in Growth AUM and degrowth of legacy portfolio is a matter of time as per my view and I am ready to wait considering current valuations. Uptrend in real estate cycle have greatly helped housing finance companies and even defunct property parcels have become attractive now and that is helping in decent recoveries, start of stalled projects and new affordable sector demand.

As its very hard to find any other decent value proposal with decent independent management, my bias in increasing stake on every fall.

Although its difficult to analyze any company as a retail investor but presence of FII/DII in this stock at least assures due diligence as would have been done by them.

My views are personal and should not be construed as any investment advise as my risk taking capability and waiting period may be far different than others.

5 Likes

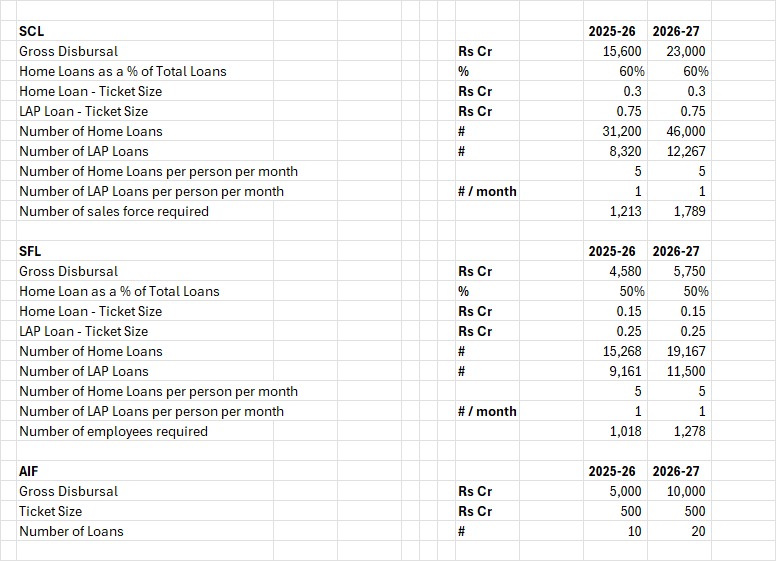

This is how I am thinking about disbursals. Once the systems and processes are in place to do co-lending at scale, the disbursals are a function of brute capacity. As has been mentioned in the projection sheet, to meet the FY2027 target of Rs 1.0 lakh Cr AUM, they need to have the following net disbursals: -

SCL - Rs 13,500 Cr (2026) and Rs 20,000 Cr (2027)

SFL - Rs 4,000 Cr (2026) and Rs 5,000 Cr (2027)

AIF - Rs 5000 Cr (2026) and Rs 10,000 Cr (2027)

Now, they already achieved the following net disbursals in 2025: -

SCL - Rs 8,200 Cr; SFL - Rs 2,600 Cr

(all figures are rounded off to Rs 00 Cr)

The gross disbursals required will probably be 15% higher than the net figures. Taking the average ticket size for SCL and SFL from their earnings update, number of loan sanctions and workforce required is worked out as follows: -

I have assumed 5 home loans per person per month and 1 LAP loan per person per month as per ChatGPT (entry level sales officer).

From the above, they need approximately 2200 sales staff for 2025-26 and 3000 sales staff for 2026-27. The FY2024 Annual report mentions 4358 employees although it does not specify how many are in sales function. My guess is majority will be in sales given this is a loan origination company. Gagan also keeps mentioning the company is currently capacitized to do Rs 2000 Cr of disbursals per month which will increase to Rs 2500 Cr per month for FY2027 which is broadly in line with targets.

However, I am not hung up on Rs 1 Lakh Cr AUM by 2027. Whether the company achieves 90,000 Cr or 1.1 lakh Cr by FY2027, it won’t change anything directionally so long as they clean up the legacy book without further hit on earnings or capital. I am not worried much about retail NPAs (at least not yet) given that 60-80% of the retail loan is going to sit on the Bank’s balance sheet and (hopefully) they will keep a check on underwriting standards.

As regards equity dilution, I take 100 Cr as a good round number for shares outstanding in FY 2027 (no basis) just because I don’t trust the management on this front. They have been poor capital allocators - issuing tons of equity at low prices.

2 Likes

I’m just concerned about the new co-lending regulations that RBI might push wherein both banks and NBFC’s will have to originate loans not just NBFC’s. Plus I don’t think it’d be as easy for SCL to avoid NPA’s considering a weaker underwriting and untested retail, a good thing is that we carry very very low risk on our books but still it might impact profitability going ahead.

Plus another factor of concern is that RBI has reduced focused sector banking from 75% to 60% this quarter, so larger banks don’t have as much “need” to push affordable financing via co-lending, let’s see how this plays out.

1 Like

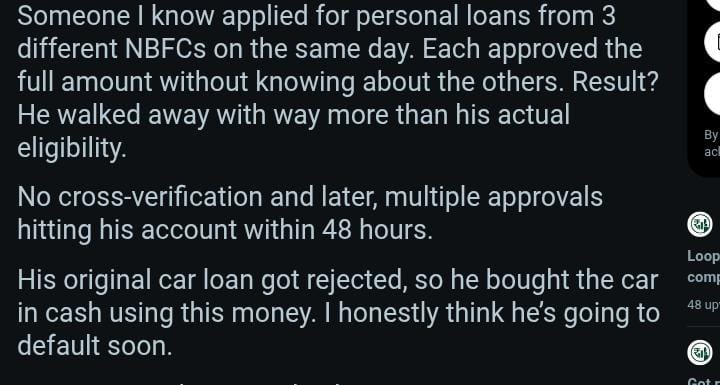

After MFIs, the next crisis could come from NBFC Retail Books. They need to steer clear of Overleveraged borrowers

Hopefully ideas like ULI make things more transparent for businesses.

https://yourstory.com/2025/04/unified-lending-identity-the-next-upi-moment-for-india

2 Likes

This fascinating line caught my attention. Personally for me and perhaps many of us if " I don’t trust" the management I will just walk away. If you don’t mind I would like to know more about your position sizing framework. Like how much will you allocate to this position.

1 Like

Haha…poor choice of words from my end probably. I just wanted to harp on the management’s inclination to issue equity irrespective of the stock price. It is the sign of a mediocre management to issue shares at low prices and then buy them back at elevated prices (or return money through high dividends which are tax inefficient). So, my comment about lack of trust need not be construed from a fraud / misrepresentation angle. I just don’t trust the management to become good capital allocators. I trust they will stay mediocre (and self-interested) as far as equity financing decisions are concerned and hence assumed 100 Cr shares outstanding by 2027.

Coming to position sizing, this position currently accounts as my largest stock position and a substantial part of my net worth. It was accumulated gradually over the past 3 years simply on account of the discount to net worth and increasing conviction as the negatives came out in the open, were provided for and more than priced in the share price.

In lending businesses, value is not destroyed when equity is raised at low prices. Rather the destroyed value during poor / risky underwriting in prior years is made manifest at the time of such an equity raise. Since the bulk of my investment was made after most of the bloodbath had already occurred, I am comfortable owning this business.

My current asset allocation is - 10% cash, 40% MF and 50% individual stocks plus some home equity in a residential real estate for investment purpose.

I don’t have much of a position sizing framework. My buying period (subject to valuation and improving business fundamentals) is 3 years and holding period is 4-5 years thereafter totaling to a 7–8 year investment horizon which is pretty much the length of a business cycle and allows time for mean reversion of industry as well as company specific fundamentals. I am happy holding 2-3 stocks if that is what I like. I have found it difficult to allocate money to something else which is near fully priced (just for the sake of diversification) when my own holding is still available at a discount.

8 Likes

Can you provide the link for the above image?

1 Like

For anyone remotely interested in Indiabulls Housing, i would strongly recommend reading this book "Fooling some of the people all of the time"by David Einhorn. The book is on this company named “Allied Capital” . I realized someone in the management of Indiabulls housing has taken out time to carefully read each and every word of this book.

7 Likes