Is Samhi hotels paying too much given the turnover is only 24cr but they are paying 205 Cr?

1 Like

The property could be poorly managed and Samhi could bring efficiency and utilise the property efficiently to maximise the revenue.

4 Likes

They have surplus land along with permission to extend the room count which is very good sign. Also Whitefield is prominent location for IT in Bengaluru.

2 Likes

It’s nearly ~2x valuation (if compared to current market cap).

But considering they plan to double the room count(of acquired entity) and Bangalore land prices increased significantly in past couple years. Seems fair valuation.

1 Like

Hi Ayush

Would like to understand how do you mean ~2x valuation. Looking at screener PE or PEG is not available. Could you please explain that a bit?

1 Like

MERGER & ACQUISITION

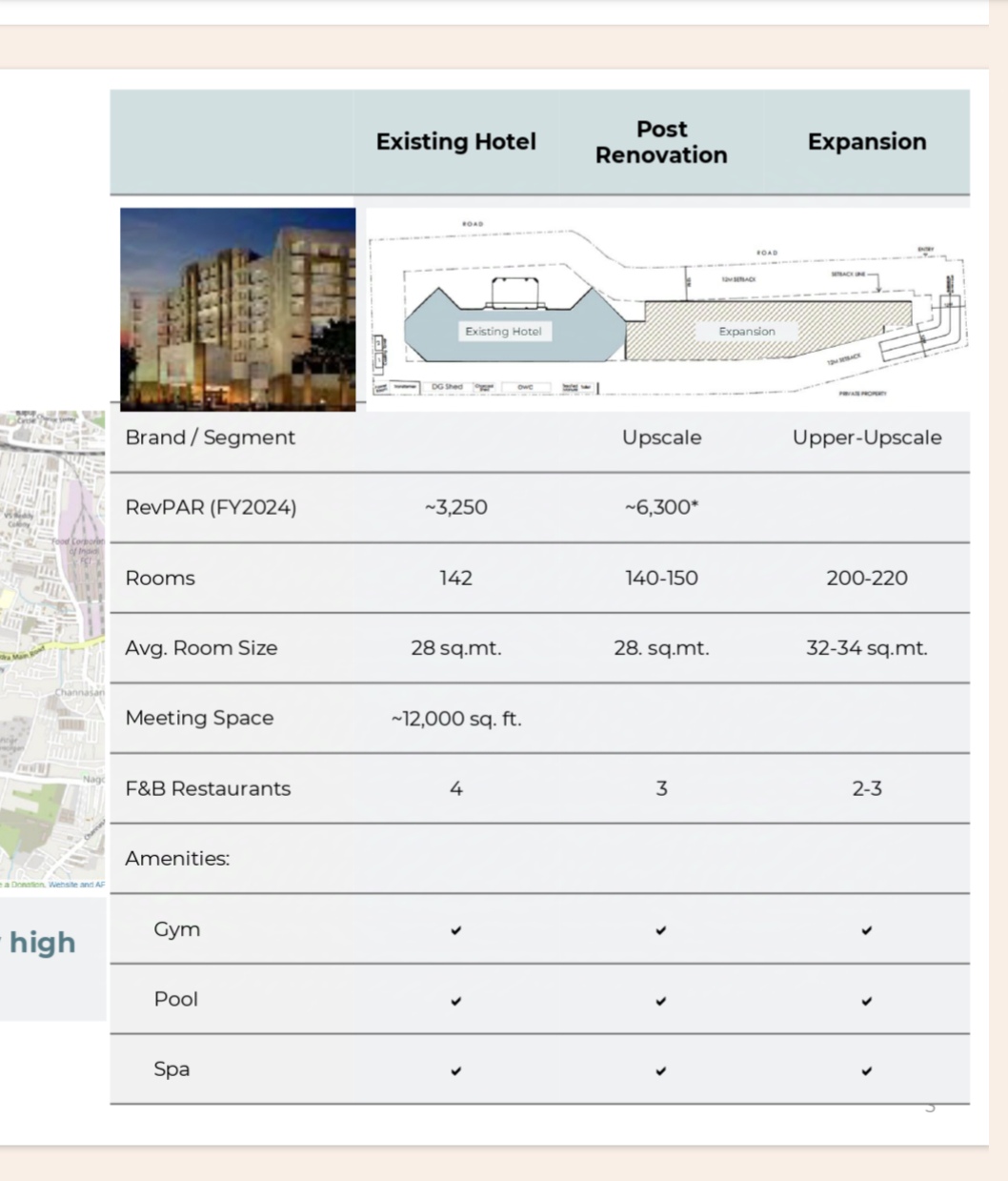

Acquiring 100% of Innmar-Tourism and Hotels Pvt Ltd for an EV of INR 205 Cr. Company owns an operating hotel with 142 rooms in Whitefield, Bangalore along with surplus land for development of an additional 200-220 rooms in the Upper Upscale segment. The company did a turnover of 24 Cr in Fy24 & Fy23.

Valuation: The acquisition has taken place at a EV/S of 8.5x. Currently SAMHI is trading at EV of 6300 with 957Cr sales in Fy24, hence implied EV/Sales is 6.6x.

The revenue per key for the Innmar in Fy24 is 17.5 lakhs. For an upper upscale segment it seems to be quite low for a hotel located at one of the major city. In contrast the upper upscale revenue per keys for SAMHI portfolio of same category is ~39 lakhs. One probability for low rev is maybe the hotel is upper mid scale category, in a similar case Samhi has ~20lakh rev per keys.

6 Likes

I Compared current Samhi valuation w.r.t. its turnover of the acquired entity.

Samhi: FY24/Market Cap= ~22%

FY24- 957

Market Cap: 4,308

New acquired Entity: FY24/Market Cap= ~12%

FY24- 24.7

Market Cap: 205

Rooms: 142

Assuming, they can double the rooms the revenue/market cap will be in line with Samhi.

(I know it will involve further cost addition to construct rooms but significant cost is land , as Bangalore real estate prices skyrocketed in last 3 years, especially in Whitefield)

It’s fair valuation.

Hope it helps

9 Likes

Yes it did.

Didn’t know this way of valuing and comparing a hotel business before. Thank you!

Assuming they debt fund this, 205Cr @ 10% , they will need to shell out 20Cr in interest costs. Co did a turnover of 24Cr in both FY24 and F23. Assuming at best it gives 20% net profit margin of ~5Cr. So it’s a negative ROI to begin with. In an year or so they spend another 50 odd crores and double the turnover to 50Cr, they might only get to 10 -15 Cr net profit, still doesn’t seem like they will make enough to even pay the interest on the loan.

Disclaimer: Not invested, researching.

1 Like

They have/will fund it with internal accruals. In this fiscal itself Samhi will generate 225-250cr or FCF.

24cr of revenue in fy23 and fy24 was when the property wasn’t managed and operated by Marriot. RevPar will be very high post renovation to upper scale/upper upscale.

3 Likes

If you were to see the slides shared by the management, few things that come out:

- this particular investment is cash accrual funded, so good news

- Basis the revpar (about 6k) of the nearby upscale properties as shared by management, current 142 rooms once upgraded have potential to make 32 cr annually and with additional 200 room once built, the total revenue easily exceeds 75 cr plus. Ofcourse there is going to be additional capex in upgradation and building new rooms but once completed the hotel with revenue potential of 75 cr is not a bad acquisition in 203 cr.

Basis my understanding this is how I read the acquisition and numbers are based on guestimates with the given data. Ofcourse management will clarify details on Monday conference call.

11 Likes

SAMHI Hotels -

Q1 FY 25 results and concall highlights -

Company profile - Operate a total of 31 Hotels, 4800 rooms in 13 cities under 8 brand names

Upscale Hotel rooms - 1074. These include properties like -

Hyatt @ Gurugram and Pune

Sheraton @ Hyderabad

Renaissance @ Ahemdabad

Courtyard @ Bengaluru

Total - 5 hotels

Upper Midscale Hotel rooms - 2163. These include properties like -

Four Points @ Pune, Vizag, Jaipur, Chennai

Fairfield by Marriot @ Bengaluru (03 hotels), Coimbatore, Chennai (02 hotels), Hyderabad, Goa, Ahmedabad

Caspia @ Delhi

Total - 14 hotels

Midscale hotel rooms - 1564. These include properties like -

Holiday Inn Express @ Pune (02 hotels), Ahmedabad, Bengaluru, Nasik, Hyderabad ( 02 Hotels ), Gurugram, Chennai, Nahsik

Caspia Pro @ Noida

Total - 12 hotels

Q1 FY 25 outcomes -

Revenues - 256 vs 191 cr, up 33 pc YoY

EBITDA - 89 vs 47 cr ( margins @ 35 vs 25 pc - huge margin expansion, ESOP costs fell from 11 cr to 4.5 cr YoY )

PAT - 4 vs (-) 83 cr ( finance costs fell from 107 cr to 55 cr YoY )

Net Debt stands @ 1862 as on 30 Jun 24 vs 2938 cr as on 30 Jun 24. Cost of debt @ 9.7 pc vs 13 pc YoY - basically a massive improvement on this particular aspect

Q1 RevPar @ Rs 4276 vs Rs 3662, up 13 pc YoY

Breakdown of revenues ( segment wise ) -

Upscale - 43 pc ( RevPar growth @ 21 pc, Occupancy @ 79 vs 74 pc, 32 pc of revenues from F&B )

Upper Midscale - 43 pc ( Rev Par growth @ 9 pc, Occupancy @ 72 vs 72 pc, 23 pc of revenues from F&B )

Midscale - 14 pc ( Rev Par growth @ 4 pc, occupancy @ 74 vs 72 pc, 9 pc of revenues from F&B )

Schedule to be operationalised by Q3 FY 25 ( a total of 302 additional rooms with an annual revenue potential of 25-30 cr ) -

Opening of Holiday Inn express - Kolkata ( will add 110 rooms )

Addition of rooms in Holiday Inn express - Bengaluru ( will add 54 rooms )

Renovation and rebranding of Caspia Pro greater Noida to Holiday Inn Express ( will add 137 rooms )

Addition of 22 rooms @ Hayatt regency Pune

Addition of 12 rooms @ Sheraton Hyderabad

Company believes their EBITDA margins have a material scope for improvement as Q1 is generally the weakest Qtr ( seasonally )

Rapid expansion of Office spaces and Aviation Industry augurs well for the company ( as they primarily run Business hotels in Tier-1,2 cities )

India added 9 million Sq Ft of office space in Q1 out of which, 67 pc came up in Hyderabad, Pune, Bengaluru and Delhi NCR - which are all company’s core markets

Expect EBITDA margins to go to 40 pc levels in Q3, Q4

Expect the cost of debt to fall further to 9.5 pc in next 6-9 months

Not seeing speedy supply build up in the markets like - Hyderabad, Pune, Delhi NCR - should augur well for company’s ARRs and occupancies. Only significant supply addition ( ie new hotels ) that’s happening right now is at Gurugram - Aerocity area

In any case, supply addition in the Industry is unlikely to be > 4-5 pc ( avg across all major markets ) where as the demand growth is much higher than this

Over and above the 302 new rooms that the company intends to operationalise by Q3, they also intend to add another 200-300 rooms via inorganic route. They ll announce the same when they strike a deal. They aim to keep adding inventory @ 10-15 CAGR for foreseeable future

Confident of generating 225 - 250 cr of free cash in current FY. Plus they are holding a cash surplus of Rs 300 cr. So - the liquidity position going forward should be comfortable to fund inorganic growth and deleveraging the balance sheet at the same time

Total capex expected for FY 24 @ 140 cr

Seeing improved occupancies in July, Aug vs Q1. Also expecting a further ramp up in F&B sales wef Q2 as Q1 was muted wrt Conferences, Meetings, Seminars etc because of general elections

Disc: holding, biased, added recently, not SEBI registered, not a buy/sell recommendation

12 Likes

Hotel industry is always capital intensive.

I will probably add 2 points in your assumptions :-

-

The appreciation of real estate/rooms , which is usually ~7%(could be more being in Bangalore)

So, net interest would be 3% which would come around 6 Cr. -

From last 2 year OPM% of Samhi is ~30% and will probably remain at around 25%

So considering 2 points above the deal seems fair.

3 Likes

I diagree with the 2nd point opm for samhi would be align with 30 or more in this fiscal year

Hi

Anyone attended today’s call, Need to know how this deal is financed, all cash, part cash part loan and net cash levels post aquisition.

1 Like

Business Update Call to discuss the Acquisition of Innmar Tourism and Hotels Private Limited (“ITHPL”).

2 Likes

Thanks a lot Girish, for sharing the recording.

My understanding of the concall is as below, others can also add, if I miss any point.

- No additional debt would be taken by the company for this acquisition.

- Renovation will start from Q1’FY2026

- Current acquisition will start contributing to top and bottom line from current quarter onwards (may be around 10 cr in the top line, calculated from Revpar and rooms )

- Company has also refinanced around ~350 crores of NCDs from 13.5% annual to 9.2% annual which can help saving around 13 cr to 14 cr in interest expenses annually.

- Net Debt/EBITDA will stand ~4.4x at the end of FY’2025 , Net debt would be around 2060 crores, which means EBITDA would be 460 crores to 470 crores

- If I assume depreciation in line with last year ~120 cr and annualize the interest payment of 55.57 cr which would be ~220 crores (one can adjust the benefit of ~6.5 crores of half yearly benefit from refinancing of NCDs) PBT for the company can around ~120 crores to ~125 crores.

- Company was in losses in previous years , so I believe it may not have to pay taxes in the FY’2025

Company is available at ~32x of FY2025 earnings. Not sure about the upside but downside seems to be limited.

19 Likes

is that 4.4X Net Debt/EBITDA correct ??

Haven’t they guided for 3.5x , if this acquisition isn’t serviced by debt and they told that the new asset will be contributing from this quarter itself means,

how and why it has increased from 3.5 to 4.4 ?? did they change the guidance or it has changed coz they used up the cash for capex?? Thought they guided to 3.5x including the capex from internal accruals, can anybody shed light on this?? @amit151190

2 Likes

Yes, because some of the case is used in acquisition.

Hello, i appreciate your concern of the debt levels but if you look at the FCF yield for this business it is very compelling. So debt servicing especially at lower interest rate should not be an issue for the company. With samhi, one of the key things to look at is that they can add inventory (room keys) other hotel players can simply go build hotels whereas samhi needs to buy the right existing asset. The fact that you have revenue visibility is more important in my opinion

1 Like