^ IHCL Commentary Q3Fy24 - Hotel room demand growing at 8-10% far exceeds supply at 5-6% CAGR.

^ As per ICRA Mar 2024 - In FY2024, the RevPAR is expected to be at an 8-12% discount to the FY2008 peak. ICRA expects hotel industry to report a 7-9% revenue growth. And as per various research report SAMHI rev growth will be close to 20%.

^ As per Jeffries report Mar 2024- “Foreign tourist arrivals have yet to catch up, while Indian Nationals’ Departures are back to pre-COVID levels.” which is a tailwind for SAMHI hotel being internationally recognized brands. With Occupancy CY23 broadly matches CY19 levels.

Occupancy at close to 70% in Fy2024 which can further go to 80-85%.

In my opinion demand will improve post elections as the new govt may introduce some policies to bring up the travel industry. (?). even aviation sector is facing some challenges. Domestic travel has to go up so that these hotels will see better results.

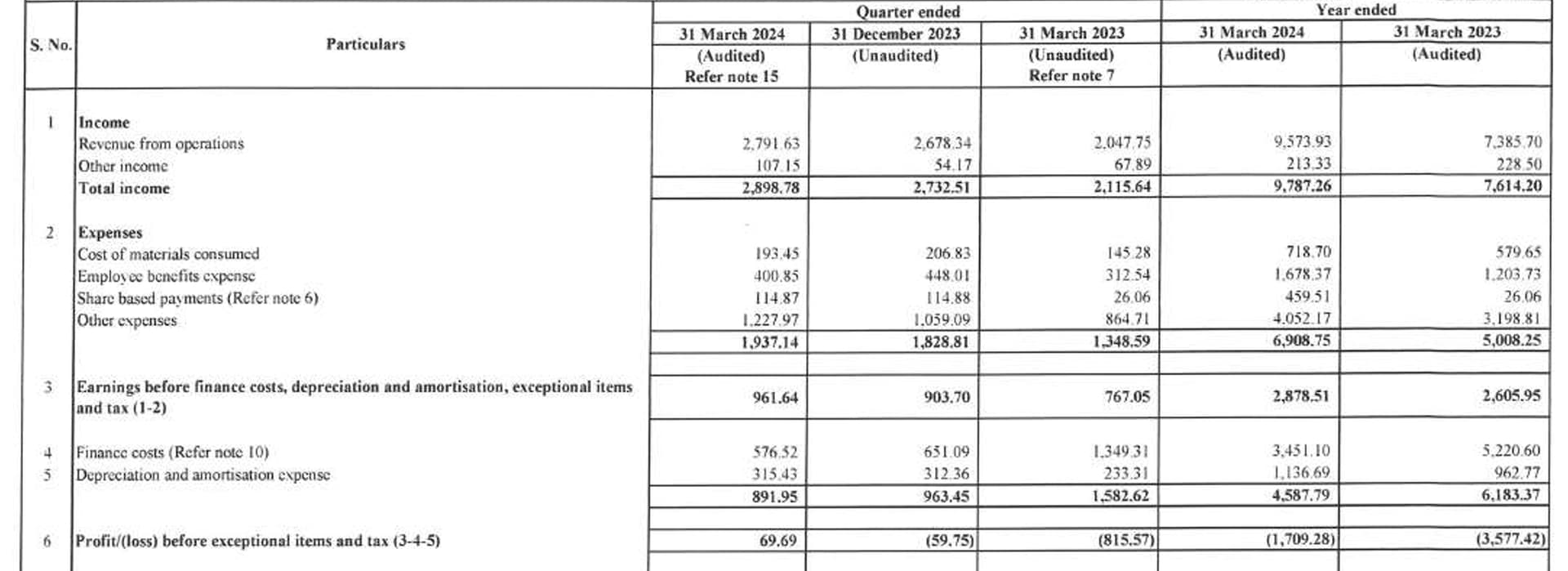

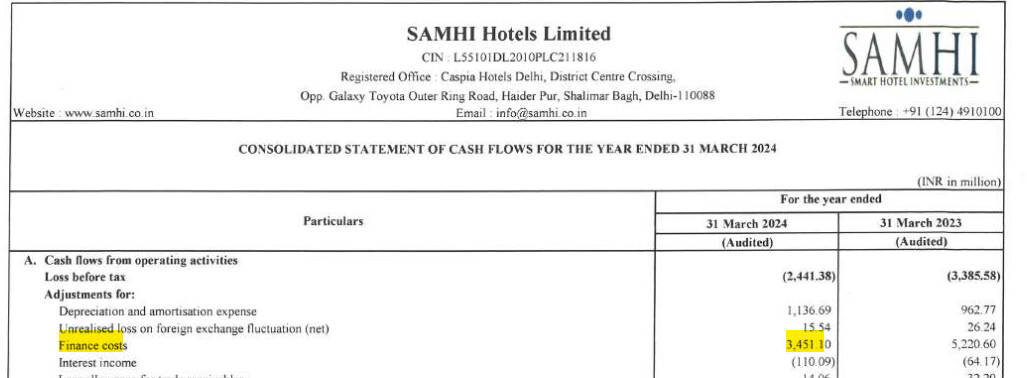

Can someone explain to me why is finance cost paid in cashflow statement significantly different than finance cost in P&L even after adjusting for interest on lease liabilities

The finance cost of Rs. 3451.10 million is related to NCDs. This amount is mentioned in the “cash flow from operating activities” section of the cash flow statement.

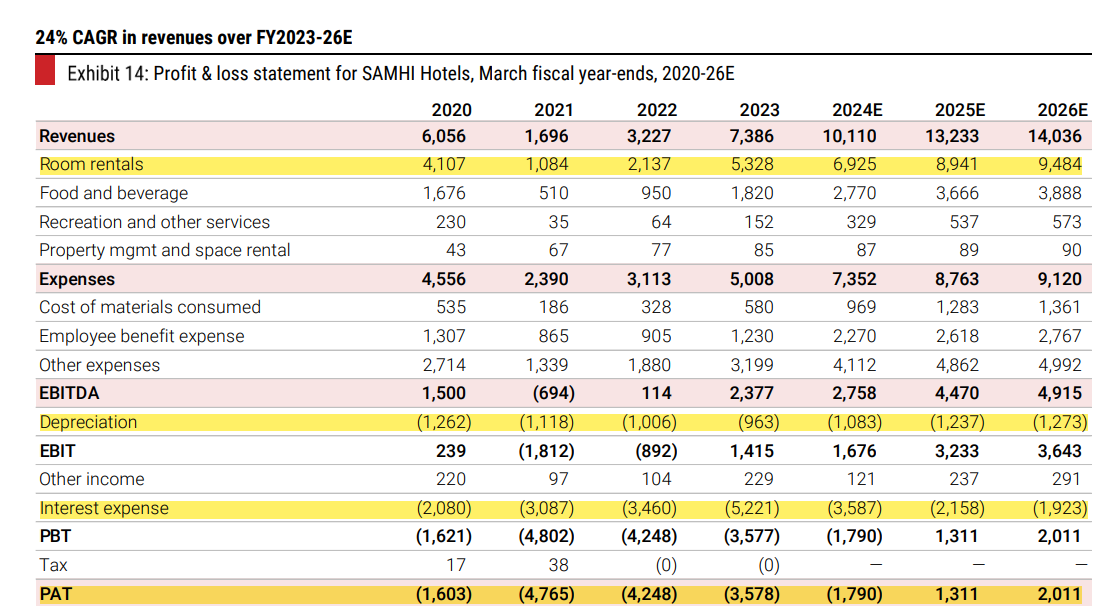

Thanks RJ! It is at a significant discount to peers and if you consider the Ex-ESOP EBITDAM which obv ESOP will finish in 2 years or so they are already doing close 38%+ EBITDAM which at a larger scale + debt repaid should result in significant EPS growth

@Investment_Learner but my question is regarding “finance cost paid” mentioned in cash flow from financing activities.

In p&l its 345 cr ( the same number is added back in cash flow from operating activities) but in financing cash flows its 672 cr

Typically, finance cost across P&L and CFS is not the same. One is finance cost and the other one is how much cash was actually paid as interest in the year. This is usually different for most companies. In this case I’m making a guess but they may have paid upfront to reduce their debt liability as they had raised IPO money to reduce the debt. So some of the additional debt they may have paid would have also got some interest cost.

What I am able to understand is that the “finance cost” of Rs. 345 cr. is the amount paid on the maturity of NCDs [refer note 10 of consolidated statement] as it is of non-core nature, therefore reflected as inflow to cash flow from operating activities.

The outflow of Rs. 672 cr. as “finance cost paid” in the cash flow from financing activities, which included the above finance cost and interest paid on borrowings.

It is speculative as not much details are available.

Hi, Neeraj… Thanx for pointing out… I totally missed it. Also, I would add that, I am bit skeptical about 200Cr interest payment in Fy25. I think it will be close to 150Cr, my thinking is that, Mgmt has already guided that, they could generate 225-250Cr FCF in Fy25 which I also agree looking at this year Cash flow. Plus they are guiding to reduce their net debt to EBITDA to 3.5x, (i assume they reduce it to 4x, so net debt will be 380*4=1520) Now, currently their interest rate is 9.8% which gives me an interest payment of ~150Cr. However, I have not considered any inorganic expansion. So things may change.

Thanx…

Got my hands on a report from Kotak, the revenue growth in FY2025 can be higher, as they have acquired additional ~950 keys and adjusted revenue for FY2024 was ~1050 crores. So my assumption is in FY2024 they may touch 125 crore to 150 crore in PAT, considering they will be saving 30 crores in ESOP expenses and the money they spent last year on integration of the additional ~950 rooms.

they won’t have to pay taxes for a long time as they had losses for the last few years.

and here is how I calculated ebitda

Expecting 200 crores to be their interest cost. So 2000 crores is debt because cost of debt is 10%. Assuming 145 crores+200 crore free cash flow, ebitda coms to 470 crores(3.5 times net debt/ebitda is expected)

Out of this, 200 is interest costs, followed by almost the same or a little higher depreciation at 125 crores.

so we get, 135 crores. remove 30 crores because of G&A and ESOP costs, we get a pat 100-110 crores.