I sensed that PE investors will lose their patience, given all other variables that go around, esp with bond yields, currency and more…I exited around 210 and will reconsider this, when this dips to a level, where it will discount, every negative possible. I might be wrong in this (as it has happened often in the past ![]() ) and for all you know, the price might put egg on my face but I have to accept that and move on. Often in the past, my exit decisions made me look very savvy for a few days, before mocking back at me !!

) and for all you know, the price might put egg on my face but I have to accept that and move on. Often in the past, my exit decisions made me look very savvy for a few days, before mocking back at me !!

PS - not sebi registered and this is not a buy/sell reco

8 Likes

Samhi Hotels will be valued between 8000-10000 cr market cap in future based on valuations. Positive triggers, QIP to reduce debt, some major corporate house buys PE stake, this will prompt to a large rerating, Ashish might stay as MD. I will stick to it as i am unable to find much in markets as of now. Though portfolio is down by 10%, Samhi has performed well in recent correction. Kalyan Jeweller was my top holding with 25% allocation, sold off all holdings between 690-750 range and increased Samhi holdings around 180 levels. Avoiding loss is a major achievement in todays market, you never know which stock will be sold for no reason:joy:![]()

![]()

22 Likes

I Like park over Samhi , it’s not clear what Samhi’s “asset lite “ business model is

1 Like

asst lite means they don’t own the property they just get them on long leases which makes it easier for rapid expansion and does not lead to delays which are there in get the properties in their own name and other problems that comes with owning the asset.

5 Likes

The bellweather of the hospitality sector, IHCL has given strong Q3 results

Topline has increased by over 35% QoQ, last quarter it had an accounting adjustment exceptional item influencing the bottom line, keeping that aside the PBT has increased over 2x QoQ

I would say it augurs well for our minnow SAMHI and an EBITDA of 450 crores for the full year seems a distinct possibilty … ![]()

13 Likes

Another hotel co. Gujarat hotel gave good result. Itc hotel has 45% stake in it.

3 Likes

We are in bear markets now, only difference in bull and bear market is that growth and growth valuations are punished and every switch to other stock will take you further down despite looking cheap:joy:![]() , experienced the same during 2018-19 period.

, experienced the same during 2018-19 period.

Markets will turn to value from growth now. Stocks which have run up hard will keep correcting, not because of any fundamental issue but because of high ownership. People will book profits from anywhere. Soon you will get horses at donkeys rates and donkeys will be slaughtered. I have shrunk my number of stocks, booked Genesys and Ceinsystech, Kalyan already booked at 700 and avoided a major dent on PF.

All high PE stocks should be avoided now, sellers will be there at every level. PE is just a perception, Bull market PE of 50 and bear market PE of 15 for same stock can be justified by same analyst. ![]()

![]()

44 Likes

All the best for your portfolio

1 Like

Revising my thesis in SAMHI with the price action making me edgy… however, I realize that I need to give it the next 2 quarters to understand whether operational leverage will play out as I am anticipating.

On hindsight SAMHI seemed to have entered the party a little late with the big boys already enjoying rich valuations…much of what it got in the IPO went for debt cleanup and it still has a good pile of debt left relative to its maketcap.

A big drawback of this company in the current scenario is that it does not have a promoter with skin in the game. Who but the MD calls the shots here? Ashish Jakhanwala poses a keyman risk that I previously didnt think of. goldman sach left in a tearing hurry and now with the dollar and yen doing what they are, quite a big chunk of FII have and are exiting. Its free float post march 2025 will be 100% and it doesnt enjoy premium valuations relative to its peers.

Amongst the Institutional Investors, Govt of Singapore with 8% equity and ACIC, Blue Chandra & GTI with 22.47% equity seem to be the steady ones but the latter 22.47% only because the lock in period of their shareholding till March 2025. Then there are investors like SBI MF, Aditya Birla MF, Lion, TT that have a 10.6% stake which are reducing their holding every quarter. ACIC is the only equity holder that has a nominee director on board.

I do worry that no meaningful appreciation will happen until this 10.6% equity changes hands and Blue, GTI an ACIC decide on waiting it out for some appreciation.

Another drawback is that it is present primarily in 6 cities. bengaluru, hyderabad, pune, ahmedabad, chennai & gurgaon will account for 87% of its portfolio. It doesnt have any presence in mumbai and only one midscale hotel in delhi. It doesnt have leisure or theme travel as its core strategies.

Fundamentally, the company is set to make the most of operating leverage in the quarters to come. It is continuously upgrading its portfolio of rooms and I anticipate that in 3 years time it is set to nearly double the rooms in the premium upscale and upper upscale category with that segment becoming 33% of its portfolio…

I expect it to churn out nearly 100 crores of net profit in this FY. And with that get the ball rolling for some more quarters of growth and entering new markets and territories. This concall I would like the management to answer how they would tackle keyman risk and whether they do entertain the possibility of roping in promoters (getting acquired) as it has a danger of de-estabilizing if there does not remain sticky institutional investors and the experienced MD no longer in the role.

21 Likes

Very valuable insight but I would argue that not being in leisure is actually not a bad thing as this protects them from cyclicality of leisure tourism. Being in metros they have business demand which is also more ADR agnostic. Also supply of new hotels in these regions could be limited because new investments wont be RoCE attractive so only players like Samhi who has good brand relationships can convert existing unorganized share to branded hotels and benefit from that. Given the valuations and FCF yield in excess of 10% makes samhi attractive. Samhi is trading in line with the global peer group of hotels, which do not benefit from the level of growth samhi is potentially capable of in terms of volume growth as well ADR growth given hotels in India are materially cheaper

13 Likes

much of it echoes with what has already been written earlier… but external validation is welcome in times like these ![]()

14 Likes

10 Likes

Samhi results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1af2edea-c339-4e09-8e6a-bfb6f7de55dc.pdf

4 Likes

OPM is improving but I was expecting better topline than this.

2 Likes

Everything seems good but top line growth 10% yoy not so impressive given the industry scenario.

Considering indian hotels revenue (sales) growth approx 29%yoy chalet 22.51%yoy.

Otherwise, highest ever Revenue, EBITDA, PBT & PAT

2 Likes

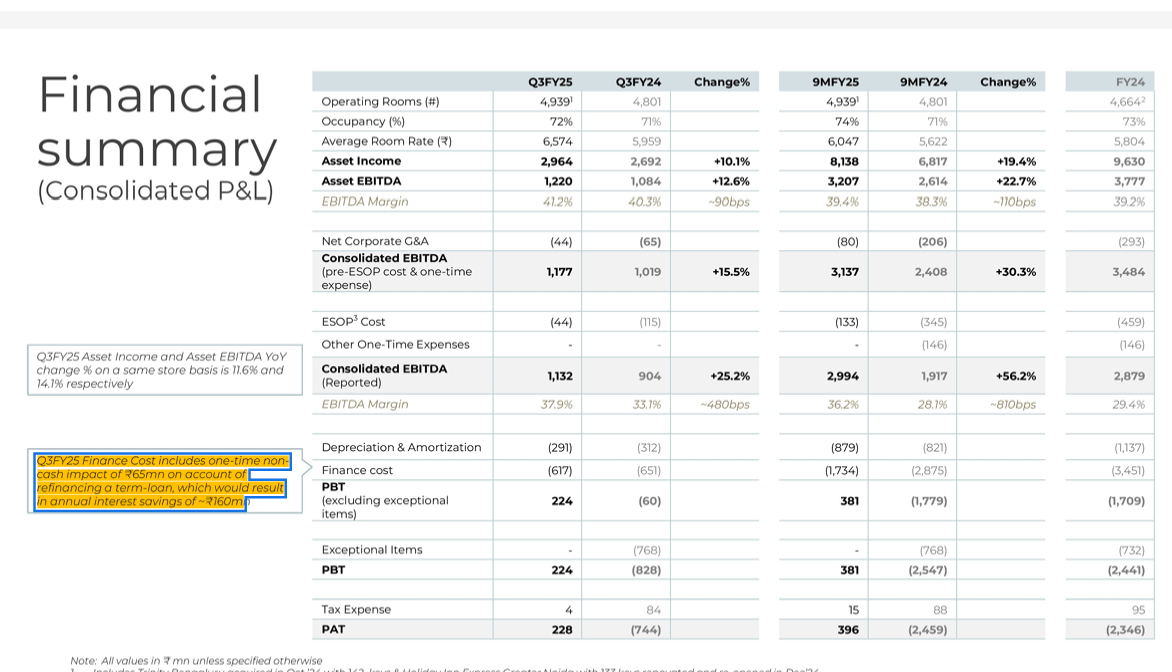

one hidden financial point to notice

Q3 has one time impact cost of 65 mn (6.5cr)

as well as annual interest savings of 160 mn ( 16 cr pa = 4cr per quater )

so this quater’s q3 profit of 22.8 cr (228 mn) should be viewed as 22.8 cr + 6.5 cr + 4 cr = 33.3 cr of profit… (333 mn)

15 Likes

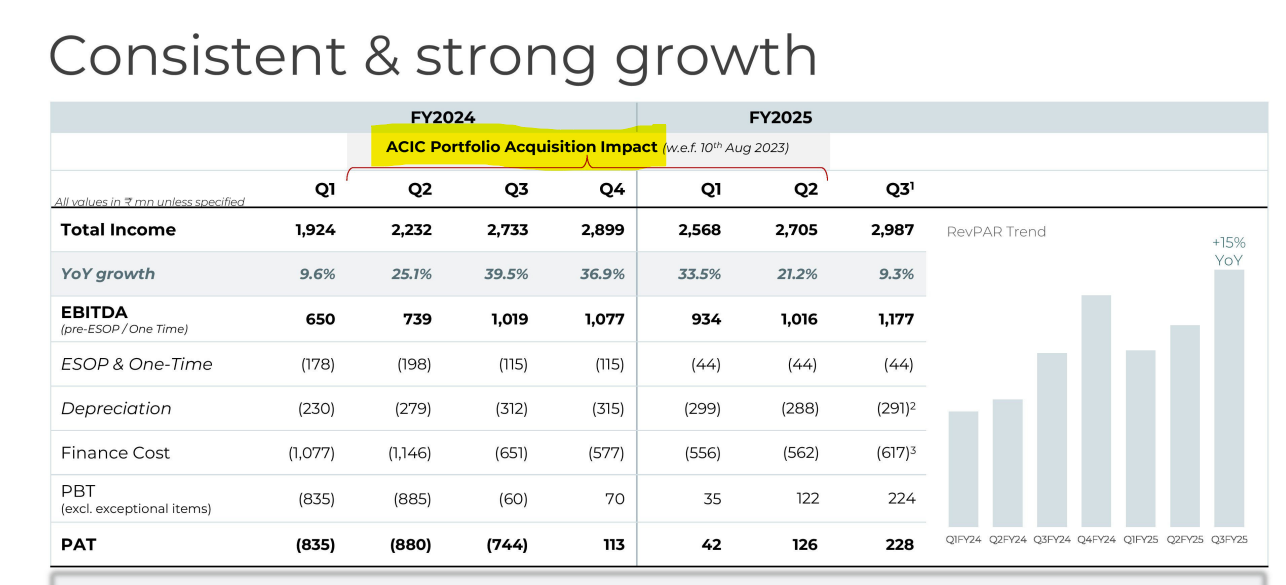

The outstanding topline growth over the last 5 quarters was due to the ACIC portfolio acquisition. The company highlighting it in the inv ppt is maybe a hint towards slower topline YOY growth in the coming quarters.

3 Likes

Q3 is strongest Quarter for travel related to leasure holidays (which Indian hotel & chalets cater ) whereas weakest for business travel (which samhi cater)

12 Likes

Its a long term hold, 422 cr TTM EBIDTA preESOP, currently trading at EV/EBIDTA of 10, 50% upside in short term should be logical, only caveat is PE locking ending in March 25 which might become a block deal now as asset is cheap and screaming buy at mouth watering valuations. Long hold for a target market cap of 10000-12000 cr.

9 Likes