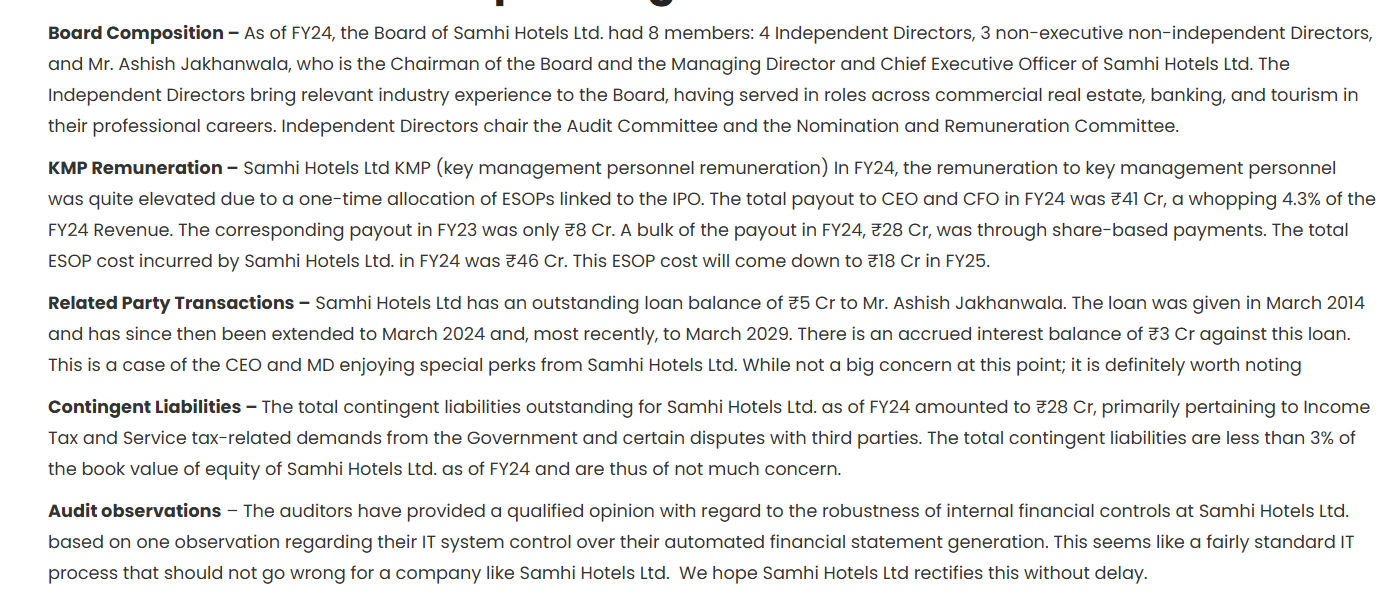

If you read the entire paragraph earlier, it is not as bad as it seems. It’s good that the auditor pointed it out which shows that they mean business. Hope the company either fixes it or gets a new accounting software

9 Likes

Thanks @CA_Sonali for mentioning my video… @dark_hunter for summarizing it.

On the qualified opinion from Auditor. Thought of sharing this note from ICRA, I read sometime back.

3 Likes

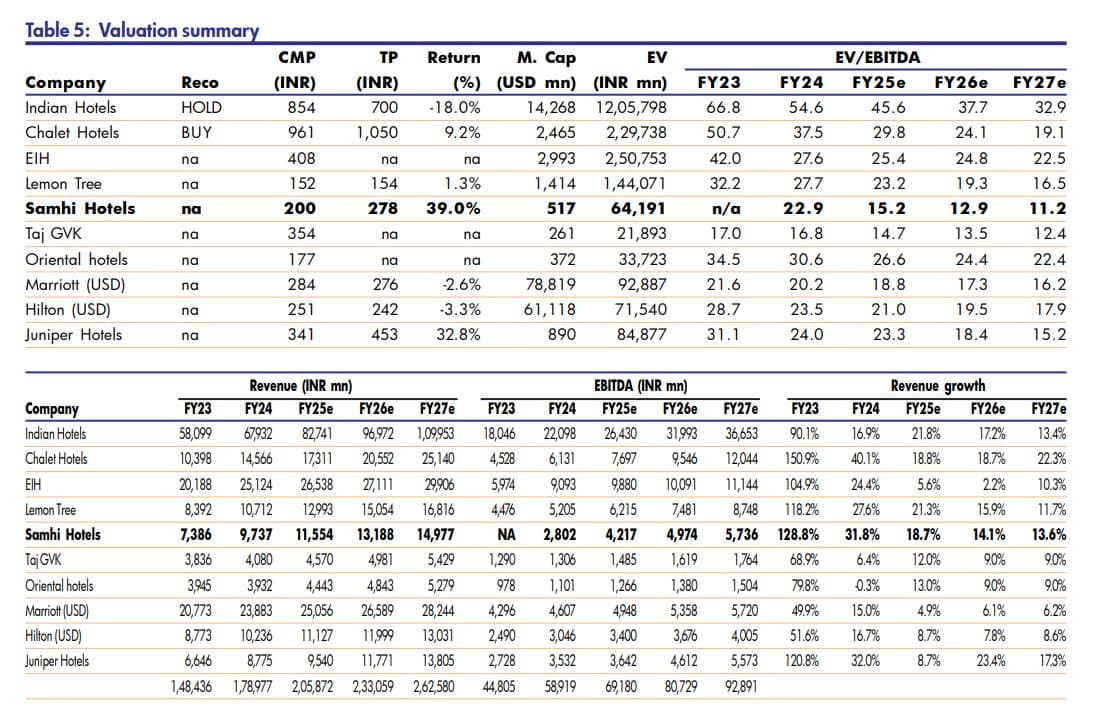

Sorry for being blunt and noobish - I fail to see the Samhi thesis here. An argument is that Chalet and Juniper trade at richer valuations but even if you calculate Samhi’s ROCE in a 450 Cr annual EBITDA scenario, the ROCE barely touches the 15% mark. Why don’t we consider the logic that Chalet / Juniper are overvalued instead? None of Chalet / Juniper have shown 15% ROCE so far because the inherent nature of this business is capex guzzling. Why should one pay 20-30x EBITDA for this?

14 Likes

May be I am over prudent about this company. But at the same time I feel that it would give me a better risk reward ratio.

6 Likes

Gain happens in 2 ways. First is obviously rental income. And second is fair value gain. India has the largest population and as cities become more larger and metropolitan, their fair value will keep growing driving their rental incomes.

Such companies cannot be looked from just todays portfolio but also their future to acquire more money making hotels and thus needs to be given a premium valuation. Just like how microstrategy is given a premoim valuation for their bitcoin holding. And remember, Samhi Hotels is way undervalued compared to Chalet and others if you go by P/S as well as comparable EBITDA. As Samhi increases revenues and EBITDA, most will flow directly to the bottom line and this can be a huge value driver.

11 Likes

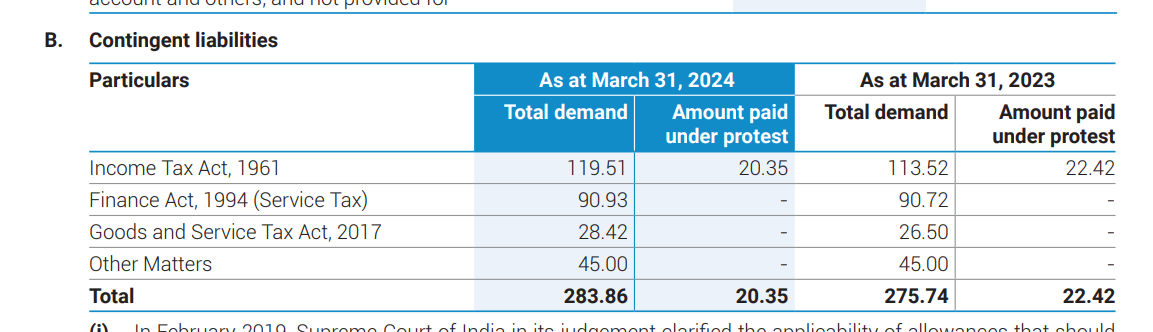

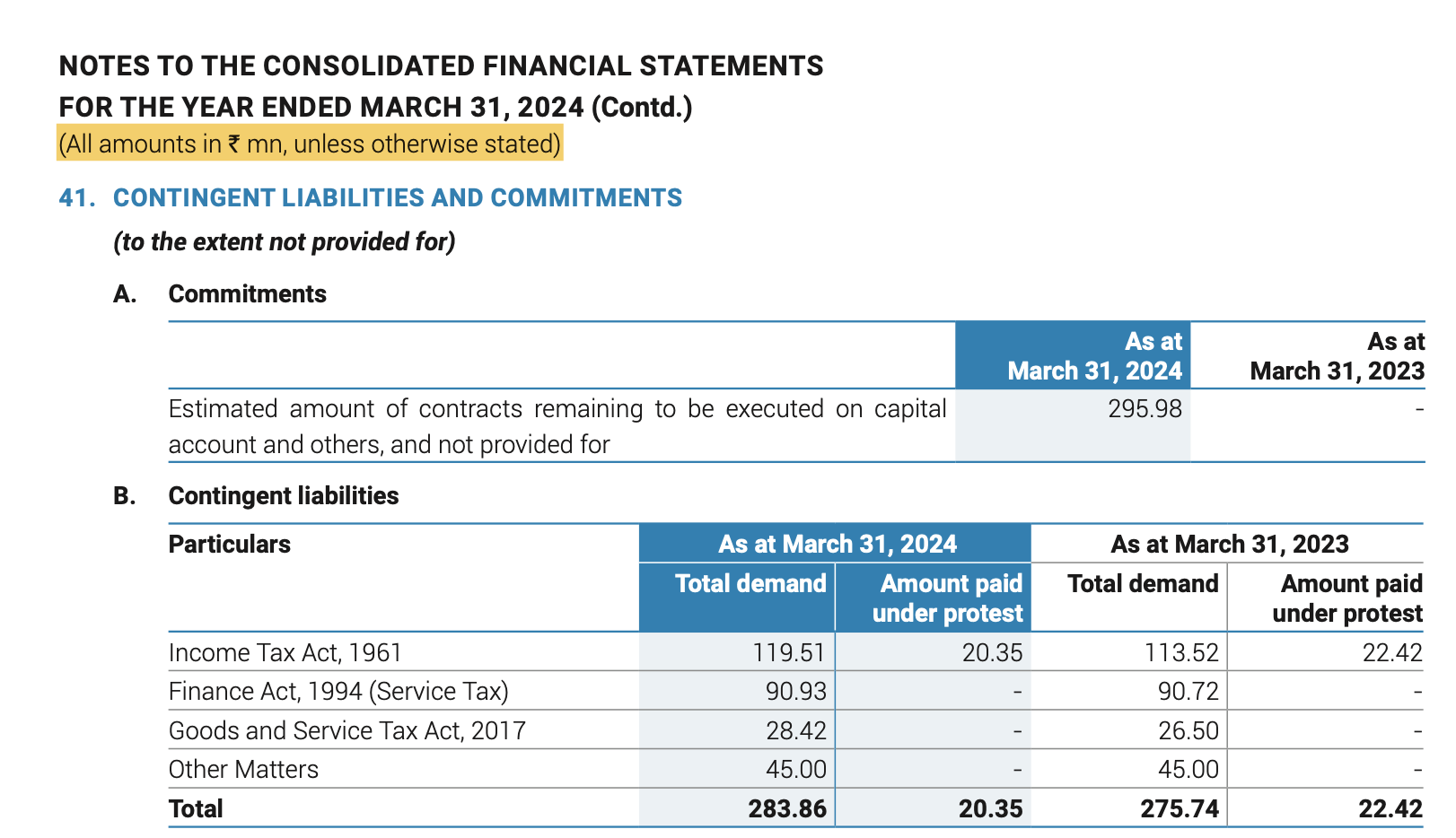

This is 28.3 crores as numbers are mentioned in INR million. 28.3 crores as a % of Networth which is 1000+ crores seems non material…

26 Likes

Don’t agree completely but would like to know forums view as well. Especially @Worldlywiseinvestors if this POV has been considered previously

I think Ishmohit has already replied to that view.

“Innovative reasoning comes up when a stock doesn’t work” hits home!

When things get too complicated, I look for simpler explanation. You are getting ~5700 rooms with an even split between midscale, upscale and upper upscale at a price of ₹ 4400 Cr. (although should add debt to it to value it properly but you get the point) - with operators like Marriott, Hyatt, holiday inn frontending it with their network, loyalty programs and a decent (and growing) OPM for Samhi to pocket.

16 Likes

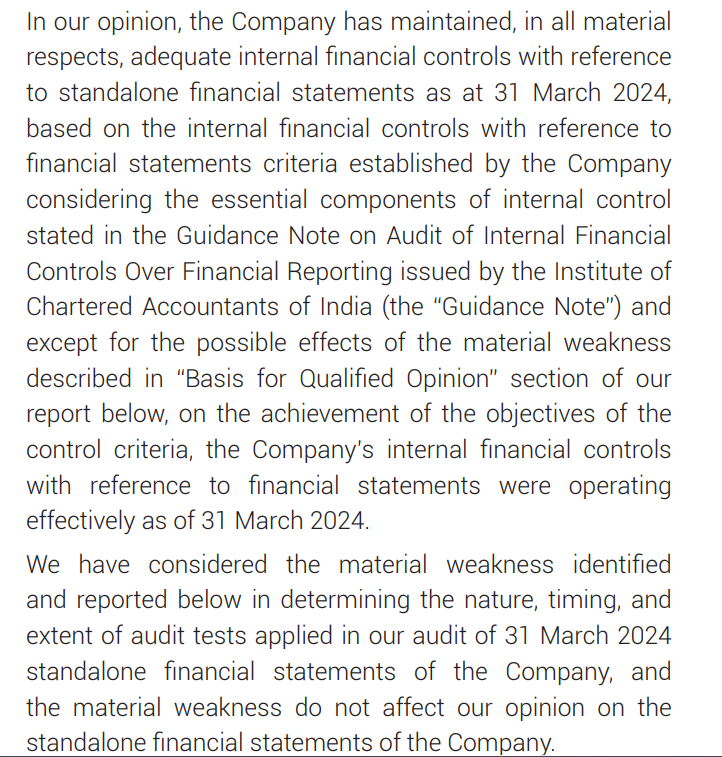

Auditor comments on the IFC is a part of a supplementary reporting along with the main Audit report which remains unqualified.

A qualified IFC means an auditor has not gained comfort through internal controls but did substantive audit procedures (such as vouching, external confirmations, etc.) to gain comfort.

Its not a big deal, honestly. Generally, its a sign that company is transitioning from a small auditor to a bigger/medium auditor. It will go away in coming time. Don’t sweat on it ![]()

5 Likes

Seems to be equally split between the sellers and the buyers, this one…

Certain FIIs roughly holding 8 percent of the companys equity as per sep qtr shareholding are selling constantly…

Closer to the Q3 results announcement date I would imagine that the triangle in formation that the stock price is travelling within, should give us a breakout and the results would confirm the long awaiting bullish thesis that people seem to have

13 Likes

Given that nearly 60% of SAMHI’s inventory consists of Marriott-branded properties, Marriott Bonvoy appears to have a more loyal member base compared to other programs, which could work in SAMHI’s favor, especially as international tourist arrivals are yet to pick up.

Source: Ventive RHP, SAMHI RHP

10 Likes

I’ve also been baffled by this valuation gap between Samhi and others. One plausible factor is the relatively high debt and interest cost for Samhi compared to peers. And the fact that management is not in a hurry to bring down the debt while continuing to invest in growth.

Another factor I have observed is that Samhi has historically focused on the mid-segment hotels and is only now investing more in the upper upscale segment (Yet to set foot in the luxury segment, although I guess they will, soon). On the contrary, most peers already have had significant upper upscale projects in their portfolio. In fact, Juniper’s majority assets are in the luxury space. Ventive which IPOed at > 50x Ebitda too is mostly into the luxury segment. Premiumization has been the theme lately and it is no surprise that market is gung ho about the luxury segment. I personally believe Samhi has been a bit late to this party and deliberately started investing in upper upscale assets only post Covid. If you see all upcoming projects of Samhi, almost all of them are either new upper upscale projects or renovation/rebranding of the existing asset to upper upscale properties. And Samhi will be at a slight disadvantage when it comes to developing new upper upscale hotels versus the peers who did it few years back as costs have gone higher.

So, market might be assuming that Samhi will be in need of incremental capital to tap into the “perceived high growth” area of upper upscale / luxury theme (which their peers are already significantly present) and with their already high debt profile, “sustainable” growth could be an uncertainty.

I think the questions are:

Is the management prudent enough to manage the debt? - I think so (of course disputable).

Is the level of continuous investment they are doing necessary for growth - Yes, it probably is.

Can both go hand in hand?

Possible, but the promoter has to be an excellent capital allocator. Is Ashish Jakhanwala & company one? Yet to prove, but recent announcements like converting an office building in Hitech park, Hyderyabad into an upper upscale project (may be first ever such conversion as voiced by Mr. Jakhanwala himself), getting into long term variable lease, etc. points to being prudent, while being creative on capital allocation.

I think market will take some time to get some certainty about these things before valuing it closer to it’s peers and if that certainty doesn’t comes along, it may remain at a discount to peers.

33 Likes

If you divide the number of hotel rooms it has with its market cap wouldn’t one come to the conclusion that it is being valued quite less than the replacement cost?

With operating margins set to climb to near 40% in H2 I am optimistic of its prospects in this calendar year, near term HMPV worries not withstanding… that being said, for me, barring ACIC who has 15% equity and 1 director on board and can be said to be a sticky large shareholder, no promoter entity is a bit of a killjoy… Other long term FII shareholders have exited the company or are rushing towards the door…

Other leading domestic hospitality chains can easily organise and shell out 2500 crores to get a minimum majority stake in SAMHI. As they are being valued at a premium by market this would also be beneficial to minority shareholders who would get capital appreciation…however the management, not having any skin in the game would probably be least likely to entertain any such proposals as this would put an end to their privy purse and esops…

The triangle in formation is looking jittery …I would have to wait till the 17th unless it breaksdown before that to know the technical fate…

2 Likes

The volatiltiy and carnage in general is making me revisit my valuation bias

Mgmt gave a target of net debt to EBITDA level around 3.7x.

However, post the money payable for the whitefield bangalore hotel (205 cr) it is revised back to 4.5x in the latest concall citing the acquisition.

In H1 2024 presentation the net debt was 1879 cr + 205 cr which takes it to 2084cr. Assuming they will reduce it further by 50 crores in H2 the net debt figure I am getting is 2035 crores. Lets round it off to 2035 crores at end this FY.

They have done 195 crores EBITDA adding ESOP. in H1 (mgmt includes esop and one time expenses in their EBITDA for the Debt /EBITDA level calculation)

For achieving 4.5x the EBITDA for H2 would have to be 255 crores.

At current FY end they should be reporting 65 crores+ net profit.

Assuming a couple of months later the FIIs do come back to their senses and the market does take notice of its improved performance by giving it an EV/EBITDA valuation multiple of 20. The market cap can therefore rise to 7100 crores by May 2025 roughly translating to Rs.320 per share. (famous last words ![]() !)

!)

Voila!

5 Likes

EBITDA of 450cr is really on the higher side, it should be somewhere around 420-425cr.

Basis that the share price can be around 280INR. Also, many PE players are looking for an exit in this year, that could be a overhang in the short to medium term.

6 Likes

I am just going by what the management has stated in the lastest conference call.

Number crunching done on the basis of this :

Ashish Jakhanwala - “Post the acquisition of Bangalore, the net debt increased to Rs. 2,080 crores.We had done an update call post the Bangalore acquisition, wherein we did the math, we had an intended target of 3.5x, 3.6x net debt to EBITDA end of FY’25 because of the Bangalore acquisition, where wehave spent about Rs. 205 crores to Rs. 210 crores some more expense towards that asset by the end of the year. On our base of our financial statements, the leverage will be about 4.5x net debt to EBITDA.”

There was bullish commentary all around. Some other excerpts from the transcript.

Ashish Jakhanwala - As we move into seasonally stronger second-half of FY"25 higher revenue led primarily by ARR growth and strong flow throughs to EBITDA, will result in further margin expansion.

Rajat Mehra - With ACIC Portfolio conversion to managed hotels under Marriott now completed, we should see material marginal improvement over the coming quarters.

As Ashish mentioned, the seasonally strong H2 should result in material expansion of PAT as compared to H1 levels on the back of higher EBITDA and stable depreciation and finance costs.

You are ofcourse right about the PE funds /FIIs exiting for which there is an acute supply demand mismatch… blame it on the strong dollar or the unwinding of the yen carry overtrade (we have japan based investment banks here that are exiting)

As for the EBITDA for the full year, I hope your figure is extremely conservative my friend.

2 Likes

In a broader outlook, return ratios for FII’s have continuously dropped in last years due to introduction of LTCG and STCG, with depreciation currency, 4 year low GDP growth for 1st half and revised STCG and LTCG in July, FII outflows are more than 3 lk cr out of which 2.5 lk crore are post budget when Madem raised capital gain taxes. My assumptions is FII inflow is not in near future untill some nonsense decision taken by FM are reversed. Stress is visible in economy, paid 2900 Toll tax last month Delhi- Ayodhya with fuel cost 8000:grinning:![]() to and fro. Have we considered any stoploss here in SAMHI hotels as i see a grim picture going forward. If rupee depreciates further don’t know how long PE investors will sit quietly.

to and fro. Have we considered any stoploss here in SAMHI hotels as i see a grim picture going forward. If rupee depreciates further don’t know how long PE investors will sit quietly.

11 Likes

This week, I sold my entire holding at 198 and bought Syrma SGS. There are so many moving variables in Samhi and with hotel industry for that matter. When I invested in this small cap, my expectation was to get good gain but it’s really flat since a year.

On the other hand I can see fundamentally sound growth prospects in Syrma for the next few years.

10 Likes