Thanks for inputs. A few points here:

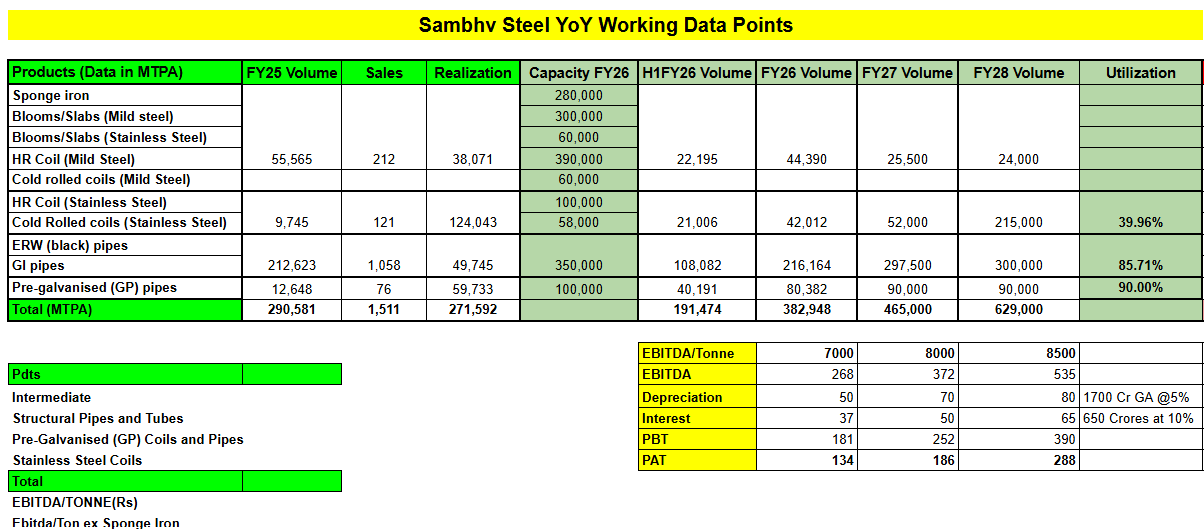

- ERW Pipes and Tubes realization obviously is directly a part of Steel price fluctuations which vary almost each month. Steel prices have struggled in Q2, a bit of drag should be visible on the realization and on the EBITDA/Tonne front.

- GI/GP Pipes realization again a bit stretched. It should be close to 70-72000 odd per tonne. Also feeling the heat of stressed Steel prices.

- SS Coils and Sheet- Avg realization rather here have ranged between 120,000 to 125,000 per tonne which should grow as they start catering to 304 and higher variants. So a good respite here.

Stainless Steel again is a very specialized play with limited entrants, Deep technical and operational efficiency needs and benefits such as higher EBITDA per tonne and better acceptance in the markets. The EBITDA per tonne in the segment could do 13k-16k depending upon the SS market which has come a bit alive in FY26 after a very poor FY25 (Jindal Stainless calls are a beast to understand things better). Although the industry is still demanding restrictions on Chinese imports for time being but it can take anywhere between 8-12 months for something concrete to come around.

Sambhv has a lot of leeway to grow their SS segment mind you Jindal at such large volumes is able to grow almost double digits each year (Fy26- 9-10% and FY27 for now is expected at 9-10% as well). The transition from ERW and GP to SS and GP(in terms of percentage split) will help the company maintain higher margins and lower coorelation to steel prices (SS Scrap prices impact will inch higher).

Regarding the new capex, the internal accruals rightly will form good enough chunk it seems and they always can take debt to cater the expansion. Going by the history they’ve done pretty solid ramp up with the last debt they undertook and have been able to bring about excellent operational and financial strength to the balance sheet. The bet in largely any steel company always is on the balance sheet strength and timely execution of the capex followed by successful acceptance of the products which leads to a profitable utilization at plant level hence making it a cash cow.

Having followed the promoters during their interviews and plant visits- They seem to have everything in place, been able to do a commendable job in maintaining all KPIs till now. Reaching scale in such short time with such balance sheet is not as easy as it appears for a traditional manufacturing business. I am fairly bullish on the prospects and believe that the company is an innovation driven business and going by the trends it seems but obvious that they’ll keep catering to newer segments in future as well.

Invested and Biased.

12 Likes

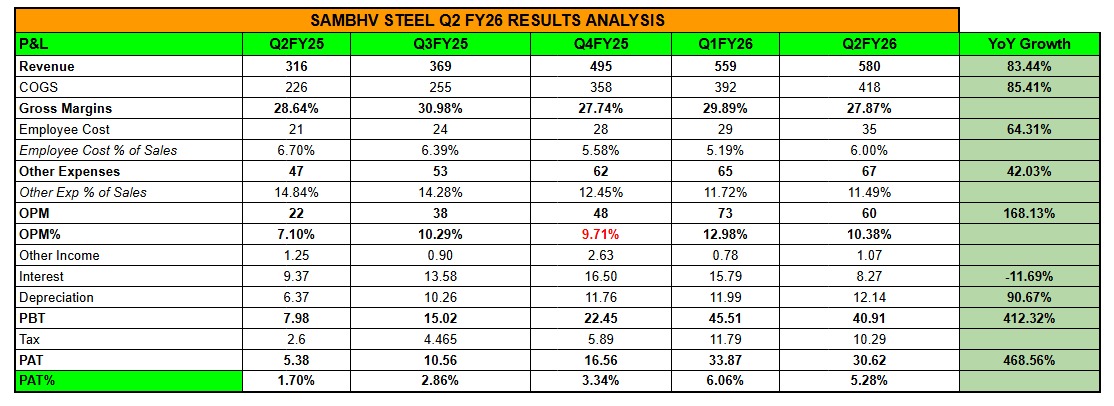

Sambhv Steel Q2 Nos are out:-

3 Likes

Q2 Earnings Call Highlights:

- Over the next 4-5 years, a fully integrated facility with a total finished product capacity of 1.2 million tons per annum will be developed in phases, with Phase-1 targeted to be commissioned by Q4’27.

- Phase I- 3,60,000 tons per annum of stainless-steel coil with backward integration for which around Rs. 810 crores will be invested, around Rs. 125 crores will be invested for additional 25 MW power plant for cost efficiency. (Debt + Internal funded) - Revenue potential 2400-2800 Crores.

- Out of 935 Crores total capex, 200 Crores incurred, 600 Crores odd debt and rest internal accruals.

- Given soft prices, EBITDA per tonne guidance at 7000 Rs for whole year.

- On why SS capex vs MS?- Stainless demand is growing fast, there is not much production in the market in India and operational efficiency will grow for the company with scale.

- Realization in SS 300 series vs 200 series - 1.25 Lakh per ton in 202 series and 1.85 Lakh per ton in 304 series.

- ERW series- 6000-7000 EBITDA per ton, GP- 1500+ ERW margins, SS broadly 14-15000 per ton.

- On EBITDA margins- 12-13% sustainable, SS margins on Absolute are higher but on percentage almost at par with Pipes.

- EBITDA per ton in the quarter was down due to moisture effect in Iron ore and

- Guidance: 4500 Crores revenues in FY28 with 10-13% EBITDA margins.

- Post capex revenue split:- 60-65% from SS division and 30-40% from ERW and GP pipes.

Overall with this new capex announcement with complete focus on stainless steel- the company will transition to become a large stainless steel player in the country and the current HR Coil led cyclicality to a large extent will be shifted to SS market dynamics. Seems like a good pivot to focus on higher EBITDA per tonne segment and grow operational efficiency with scale.

Disc: Invested

8 Likes

Go India Small Cap Day - Sambhv Steel & Tubes Ltd.

A very insightful webinar for deeper understanding of the company — a must-watch.

Disclaimer - Not Invested, but interested in investing.

2 Likes

Company announces expansion plan for Cold Rolling Mill (CRM) with Bright Annealing (BA) Line and Continuous Galvanizing Line (CGL), Situated At Village Kuthrel, Tehsil Raipur, District Raipur, Chhattisgarh– (“Kuthrel Unit”).

Have been able to work a bit on the numbers front ex latest announcement:-

The company has pivoted completely to focus on the Stainless Steel segment for next 2-3 years atleast as per their capex plans. EBITDA per tonne profile should better itself each year courtesy the SS segment gaining significant share in revenues. Being an integrated player has significant advantages in a time when the steel prices are hovering at around 5 year lows (Steel prices hit 5-year low! Value drops sharply; top factors for steep fall - The Times of India).

Interesting to see how the current dynamics play out for Non- integrated ERW manufacturers vs the Integrated players like Sambhv Steel. In any case, increase in Steel Prices eventually will help absolute numbers both on realization and EBITDA per tonne front. What we’re seeing is the numbers during a very tough market environment wherein the prices of Iron Ore (the key RM) haven’t fallen as much as the HRC prices which guides the pricing of the end products.

Nonetheless, considering a 40% utlization in FY28 on the new capex- the EBITDA per tonne on blended basis can be 8500-9000 to be on conservative side- EBITDA number can range between 550-600 Crores depending upon market scenario. FY29 later will be the peak capacity utilization year for which one can expect maybe 70%+ utilization.

Overall a possibility of EBITDA 3.5x-4x (FY25 base) and 4-5x PAT (FY25 base) seems like very much doable if everything falls in place in the next 3 years.

Disc: Invested

6 Likes

Some positive move in the steel prices finally.

Mills raise flats prices: Leading mills raised list prices of hot-rolled coil (HRC) and cold-rolled coil (CRC) by INR 750-1,000/tonnes (t) in the week ended 19 December, after keeping them stable for sales in the beginning of December compared levels prevailing during end-November.

https://www.bigmint.co/insights/detail/bigmints-india-steel-index-rebounds-before-year-end-positive-momentum-may-continue-707809

4 Likes

Q3 sales update reported by company. Good jump YoY. However QoQ flat - 15% higher volume of SS which is having higher EBIDTA & minor dip in pipes, tubes category. QoQ good ramp up seen in SS which is going sign particularly when they are targeting huge capacity addition in this segment.

Off late good recovery in steel prices, also government policy to impose 12 to 11% import duty will be supportive for the industry. However no decision of same for SS product. However concall highlighted about compulsory ISI certification is helping local players. However as steel prices started rising in late december, Q3 result might be similar to Q2 in terms of realization.

My take - FY27 will be consolidation phase for Sambhv bcoz not much new capacity addition is coming. So YoY growth will be tapid 10-15% by achieving maximum utilization level. Game changer will be FY28 onwards. If import duty comes in SS category along with new capacity addition that will be bonanza.

Valuation is now reasonable at 25 pe on TTM EPS which is inline with Jindal stainless steel (After FY28 it will be more ss company than steel company so comparing with JSS). Also recent uptick is steel prices supporting all steel company stock price (e.g. APL apollo at ATH). However FY27, we might see higher interest, depreciation & staff cost before actual sales comes in FY28. If stock remains rangebound till that time, it will be great buying opportunity.

Yesterday, stock locked-in ended for almost 1385 cr. (Almost 50% market cap) - may be that’s why stock fell.

Disclosure: I entered yesterday for tracking position. I will wait for better price/time to buy more.