Salzer Electronics Notes

Salzer Electronics Limited is engaged in offering Total and customized Electrical Solutions in Switchgears, Wires & Cables and Energy Management business.

End user demand

Financial Performance

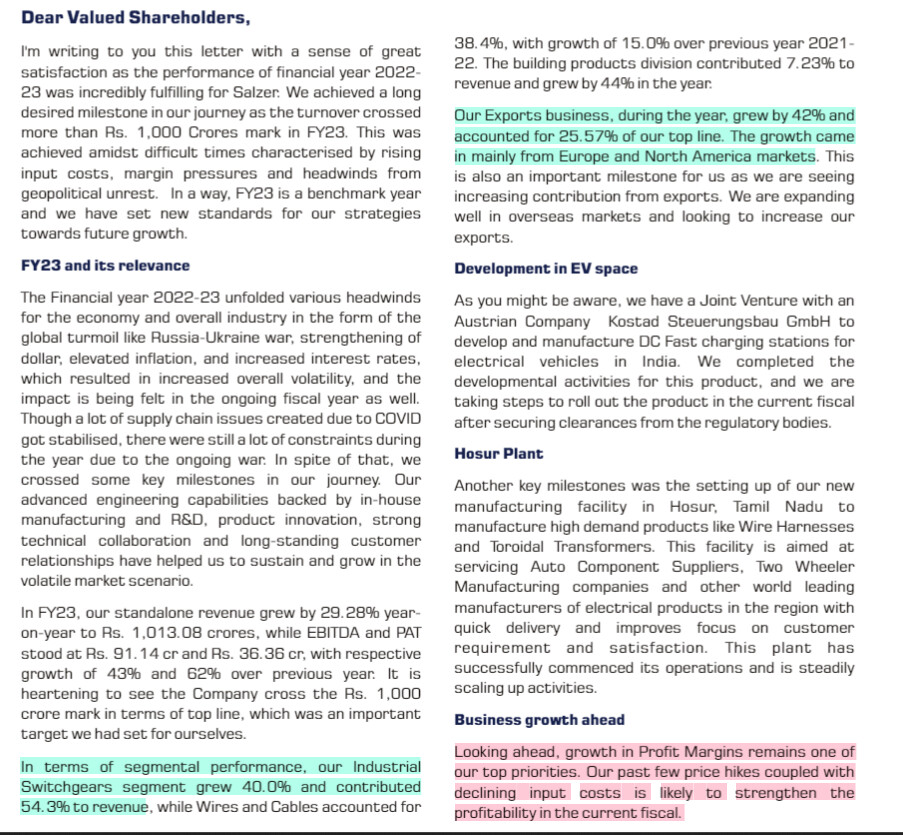

- FY23 revenue grew by 29 to 1013 Cr

- EBITDA grew by 43% to 91 Cr and margins were at 9%

- Subsidiary Kaycee industries grew 42% to 42.3 Cr and PAT grew 87% to 3.5 Cr

Product Mix

- Industrial Switchgears at 54.3%

- EBITDA margins ar 11.5% for this division

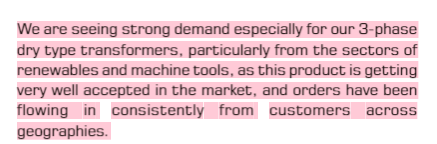

- 3-phase dry type transformers grew 180% in FY23

- Wire harness grew 18%

- Wires & cables contributed 38% and grew 15% in FY23

- EBITDA margins ar 6.5% for this division

- Building product contributed 7%

- EBITDA margins ar 2.7% for this division

- In the switchgear business, 65% of the sales comes from the toroidal transformers, three phase transformers, rotary switches, wire harness, and isolators.

- “Our segmentation in the wire and cable has been more into agri segment and our distribution is through Larsen and Toubro. And that’s the reason, given the agri segment is a seasonal market. So, when it goes up and down we are struggling. We’re trying to bring down the dependency on that particular product segment, but it is taking a time, it will take some more time before we see 8% to 10% margin improvements. 8% to 10% EBITDA margin in the wire and cable at least two years from now.”

Customers segmentation

- Products are mostly sold under Salzer brand - “Majority of the business that we do is selling to them under our brand. But we also do certain branding businesses for some OEMs. But the majority of the business is we sell to them under our brand.”

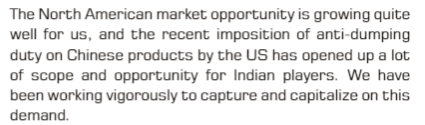

- Continue to see steady growth in exports to America, Brazil, Argentina, Chile

- Exports to Americas grew 55% in Q4FY23

- Exports contributed 26% in FY23, growing 42%

- “Top 15 customers for us might be contributing around 45% of our sales approximately. That is the concentration that we have. We don’t have a single customer giving business beyond 10%. So, customer concentration is very, very low.”

- 15%-19% business coming from renewables

- “I think on the renewable side, we have good businesses coming from solar inverters, the business, solar inverter manufacturers for our transformers and Wire Harness. And we also get AC/DC contactors not for the renewable business, but for the HVAC market in North America. For that also, I said that I think this quarter onwards, we have started seeing the revenues from that business also.”

Demand drivers & outlook

Management Verbatim -

- “On the switchgear front, growth was driven by high margin products like toroidal transformers, three phase transformers, wire harness, rotary cam switches, and isolators. All these comprised approximately 65% of our switchgear division sales.”

- “There is a growing demand for a lot of projects such as roads, bridges, buildings. The government’s focus on Smart Cities development is also expected to spur demand for a lot of electrical products in our portfolio. Even the private investments continue to happen in a big way in India, which is also increasing the demand for all our products.”

- “There’s increasing demand for renewable energy sources such as solar, wind, and hydro power, which has opened new growth opportunities and demand for switch gears, transformers, wires, and cables’

- In first 3 quarters, experienced slowdown in W&C business due to high inflation and slowdown in agri market

- Going forward from exports side, if US gets into recession, there will be an impact on Salzer business

External Links

CG power 120 Cr capex in power transformers and distribution transformers

Global demand to grow by 6%

Wire harness demand to grow because of EV push but industry is competitive

TAM

The global switchgear market size was valued at close to USD 90 billion in 2022 and is projected to reach USD 145 billion by 2031, registering a compound annual growth rate of 5.5% during the forecast period of from '23 to 2031.

The size of the Indian switchgear market was estimated at USD 9.75 billion in 2022. During the period 2023 to 2029, it is projected to grow at a CAGR of 7.12%, reaching a market size of USD 18 billion by 2029

Large TAM, small co no TAM concerns

Supply side dynamics

Product Pricing/RMs behavior

- Company raised prices after RM price hikes to recoup margins and as RM prices are coming down, margins should improve

- “We used to be at around 13%, 14% EBITDA margin levels in our switchgear products which considerably dropped to around 9%, 9.5% in FY22 because of the raw material price fluctuations. So, which we gradually started improving in FY23 and we are at around 11.7% as of today, “

- “So, the more transformers that sell, then the blended margin inside the switchgear business will be slightly down compared to what we will sell more of the contactors or switchers and terminal blocks and things like that. So, there is a slight change in the EBITDA margin within the switchgear businesses, there are certain products like rotary cams switches or isolators or cable ducts that can give us 17% EBITDA or 16% EBITDA and there are also certain products like wire harness or three phase transformers or toroidal transformers for example, which will give us a 11% or 12% EBITDA and also sometimes we sell into certain sectors where we are new, where we have to get the business. So, then the price we have to be competitive, and the EBITDA margins in those sectoral sales also can be little down. So, that is the reason that we have not gone to 12%, 12.5% EBITDA margin, but we are at around 11.7%”

Differentiation/Value Proposition

- Largest manufacturer of Cam Operated Rotary Switches, market leader with 25% share

- Wide distribution network in 50 countries and access to L&T’s local network through more than 350 distributors

- In-house manufacturing and R&D enables superior customization of products

- Amongst few players in India, to offer total & customized electrical solution

- Branding partner to various large OEM’s in India

Patent Applications

“There are certain products that we have applied patent for, like one for rotary switch again a new technology rotary switch we have applied patent, there are some contactors, some contactors we have developed new which we have applied patent for and there is also a wire management, the cable ducts we call but the broad name is wire management system, we have applied a patent for that. There are also new designs, new concepts which we have applied for patents.”

Switching Costs/Network Effects/Economies of scale

No concrete data but some indirect examples -

- Preferred supplier to GE, Schneider and only approved supplier of Nuclear Power Corporation

- Largest supplier of rotary and load break switches to Indian Railways

Competition

Fragmented nature of the industry with several players

- Management on competition in toroidal transformers

- “Toroidal transformer is nothing but a transformer, a little different transformer, it can replace the normal transformers in the market. So, any transformer, a small transformer, I’m not talking about the large transformers on the road, the distribution transformers but these are small equipment transformers that you see inside a stabilizer, inside a UPS that’s a common equipment that I can sight you can see it, a stabilizer a transformer inside a stabilizer, is a stabilizer which we can, a toroidal transformer can replace. A toroidal transformer is a little different in technology which is highly efficient, sometimes the shape and size can be adjusted to suit the requirement of the customer, these things cannot, it will have low magnetic noise, these advantages will not be there in a normal EI core traditional transformer. So, that’s the difference between a traditional EI core transformer and a toroidal transformer. So, in the competition there are hundreds of manufacturers of standard traditional transformers in the country. If you take toroidal transformers there used to be very few but now a lot of people have started making toroidal transformers also, because the whole technology people are converting from EI core into toroidal transformers because of the high efficiency and the advantages of flexibility in shape and size. That’s the difference between toroidal and transformers and application is wide application, medical equipment, any equipment. That’s a toroidal transformer that is being used.”

- EV Fast chargers

Management

Capital Allocation

- Acquired 74% stake in competitor Kaycee industries in FY20 and business has scaled well with better ROCEs than Salzer base business

- To do preferential issue of 47 Cr for promoters to increase stake in the company and use funds for growth

- Forthcoming capital allocation decisions

- Hosur plant for 15 Cr to meet demand for toroidal transformers and wire harnesses

- In the first phase, the company will use 15,000 sq ft and balance in the second phase, with commercial production expected to begin in March 2023.

- “Creating this facility at Hosur with proximity to the presence of large Auto Component Suppliers, Two Wheeler Manufacturing companies, and other world leading manufacturers of electrical products in the region would gain more momentum with quick delivery and improve focus on customer requirement and satisfaction. With this new manufacturing facility, Salzer aims to provide timely delivery and high quality products to customers in India and abroad”

- JV to manufacture fast chargers will require 12-15 Cr

- Working capital expenses

- Some concerns around capital allocation -

- Subpar ROCE around 10% as W&C business is a drag to overall business

- Company trying to enter into EV fast chargers which could be competitive market again

- Analyst concern around lack of focus and management’s response -

- “We started off as a rotary cam switch company that’s how the company started three decades ago and there is a limitation for a rotary cam switch within India or globally because the market size is limited. And then the reason that we ventured out and started making various other different products is that we wanted to grow on scale and also be with the customer connected with many products. And that’s how almost all the top switchgear companies across the world have grown including Schneider, including Siemens or Eaton or even the Indian companies like Larsen and Toubro or Havells for example. L&T is a switchgear company, but they have 25 products within the switchgear segment. So, that’s how this business happens in the market, the business trend is like that… We actually went a little more diversified started making transformers, wire harness and also various other products that may or may not fall under the switchgear definition, but it sells to the same customer, the same customer uses this, sometimes we get a customer for rotary cam switch because of transformers or vice-a-versa. So, that’s the advantage of having the large product portfolio and trying to expand all the products and as you rightly asked how and which product you’re going to expand, as the opportunity comes we are allocating capital and expanding capacity dynamically as the opportunity comes to us. Last year was the year for three phase transformers because the growth in three phase transformers was close to 78% or 100%, no no, 250% actually year-on-year. So, when the demand came in, we had to be dynamic and we had to expand the capacity and then we had to capture this market. So, that was the reason that from 25 crores in FY22 we were close to around 75 crores in FY23 on that business and it continues to, the growth has slowed down but it continues to grow at around 30%, 35% in this year. So, that is how we manage the product portfolio within the segment.”

Terminal Value Decisions

- EV chargers optionality (Formed JV’s with Kostad Steuerungsbau GmbH & EMarch LLP to enter EV market)

- “Long term vision is to be a global electrical solutions provider. That’s what we are looking at. So, anything to do with electrical solutions, we want to be there. And we want to be a first mover. So, that was one of the reasons we got into electric charging, because we thought that EV is going to be the future in the next 10, 15 years, at least a two decade business from now, before the technology can change or whatever happens. So, we thought, we have all the capabilities, we have all the components that will go into a charger, and why not make a charger. And luckily we got a JV partner to manufacture that and that is how we are into that is the reason that we are into that. We have a reason for this, because we can use our components. And we have the technology and we can see that, the future business is there. The future technology is there and as an electrical company we want to be in that space that’s the reason we’re doing that. ”

- Management has come in this division with some target of 500 Cr revenue from EV chargers, but they are not openly saying much about this division

Past Execution & Future Guidance

- Walk the talk (Mix bagged)

- In FY18, management said “We definitely see a constant improvement on the EBITDA margin; I think if you look at year on year basis, I think we have almost increased by around 2% almost. We would constantly try to increase the EBITDA by at least 1% going forward in the next one year, 0.5% to 1% is what we expect this EBITDA to increase.”. But margins have not expanded since then but came down

- Achieved more than this - “FY2019, the acquisition itself will add us at least 10% of our revenue, so we should be growing at least by 15% minimum if everything goes normal, so overall we expect to clock at least Rs. 535 Crores for next year approximately. “

- Future Guidance

- Achieved internal target of 12% ROC

- “We will continue to not just focus on profitable growth, but also on capital efficiency and enduring to improve our working capital cycle and being a cash flow positive company continuously.“

- Top line growth guidance of 20% and PAT growth of 25% for at least 2 years

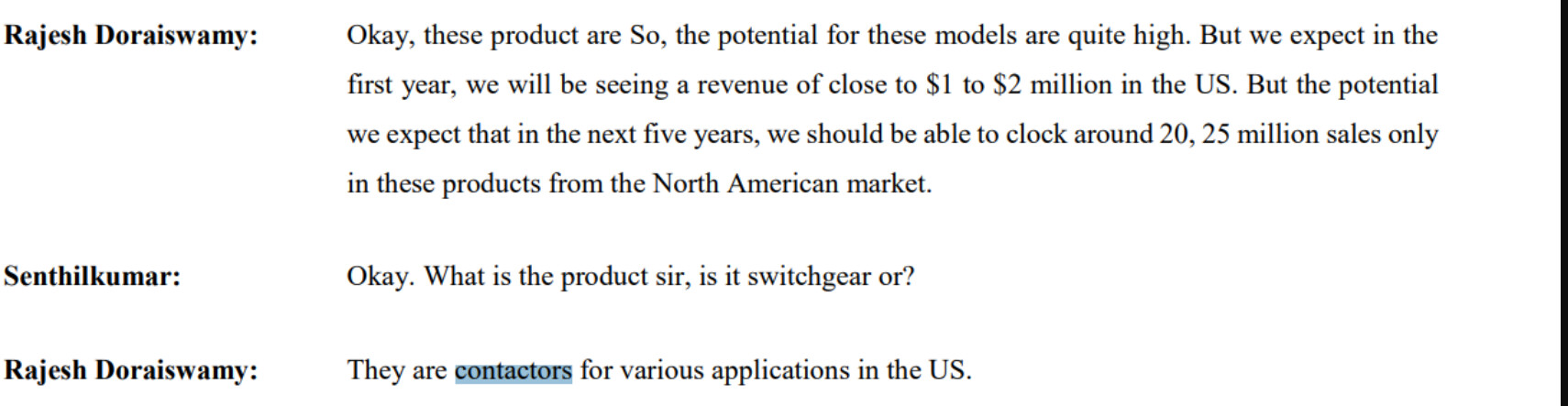

- Expects to sell $20M of newly developed product contactors in NA market

- Business split in 5 years - 60:30:10, 60% from the industrial switchgear business, 30% wire and cable, 10% from building electrical. EV charger would be a subsidiary and could have equal revenue if it scales up

- Margin expansion to happen because -

- RM prices have come down

- Increased scale will drive some operating leverage

- Target to reach 18% ROCE

- “We are working to improve our ROCE to close to 18%. That’s what our target here internally is. And one of the reasons is the long working capital cycle. I think that is where the reason that the capital employed is higher. So, as I have been telling, I think, we are working to reduce our inventory, bring down our receivables. So, these are the 2 major contributing factors for higher capital deployment. “

- Execution

- Co. had some plans in the EV conversion kit business recently which has not scaled and management accepts that and is going slow on that venture now. The company faced some ‘teething troubles’ per the management to build cost effective product for Indian market

Valuations & Summary

The business is at 17 PE and valuations look very reasonable given the growth prospects. Management guides of 20% topline growth with margin expansion if RM prices remain benign. But the reasonable valuations are somewhat justified as the market isn’t sure of management’s capability and execution prowess. Over the years even though the range of products have increased in the switchgear segment but the margins and ROCEs have not increased much to inspire confidence. Some doubts on capital allocation have been there as market sees Wires & Cables business have dragged margins, upcoming EV fast charging business may or may not work out, EV conversion kit business has not gone anywhere. The end customers are bigger in size and may have higher bargaining power, supply side is fragmented with several players trying to capture demand in sunrise power, infra and renewables sectors.

But no company is a perfect investment and given the valuations and growth prospects, this seems worth tracking. The company may be in a sweet spot at the moment with tailwinds in power, infra and renewables sector and maybe able to sustain growth in the near to medium term. With top line growth coming good, there is a very good chance to increase margins gradually and EV business is an additional optionality at the moment. Management vision and execution will decide if business can change gears and create sustainable wealth.