IPO of Salasar Techno Engg Ltd is closing for subscription today and the Co is issuing shares at 108/- to be listed on BSE and NSE main board. The post issue equity would be Rs.13.28 and for FY 17 the PAT was Rs.18.76 crs on a consolidated turnover of Rs. 367 crs. For FY 18 management guidance is of 475 to 500 crs. A more detailed analysis will be posted by me in next couple of days. In the meantime more details can be be accessed from its RHP :

https://www.nseindia.com/products/content/equities/ipos/debt_ipo_current_seflncd3.htm

Disc: am applying in the ipo

1 Like

There is nothing cast in stone in Equity markets but I am quite confident after seeing the growth, quality of its balance sheet, op performance, commentary by Skipper and KEC management regarding the sector’s outlook and my interaction with the management of Salasar.

1 Like

What is the source of Management guidance of 475-500 crore for FY’18 ?

FYI IPO Notes

by Nirmal Bang

by SMC online

http://www.smctradeonline.com/Admin/ResearchReports/636354727286240132_SALASAR%20TECHNO%20ENGINEERING%20LIMITED%20-%20IPO%20REPORT.pdf

by Way2Wealth

by HEM Securities

http://www.equitybulls.com/admin/news2006/news_det.asp?id=210640

by SP Tulsian

https://www.sptulsian.com/free-zone/ipo-analysis/Salasar-Techno

by IndiTrade

http://www.inditrade.com/UploadResearch/636355431282091250_Salasar%20IPO%20Note%20DS.pdf

interaction with management during their road show

This Rs 36 crore IPO gets bids for nearly Rs 10,000 crore; subscribed 270 times.

Salasar Techno Engineering’s Rs 36 crore initial public offer (IPO) has received a massive response from the investors with the issue getting subscribed 270 times with a demand worth Rs 9,700 crore on the last day of offer.

Read more here: http://economictimes.indiatimes.com/markets/stocks/news/salasar-techno-engineering-ipo-subscribed-270-times/articleshow/59635466.cms

1 Like

What is the date of Listing for Salasar.

25th July. GMP is 102-105

1 Like

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=0a624b78-0a72-490f-bb82-2965a00e228d

http://www.bseindia.com/xml-data/corpfiling/AttachLive/08b53afc-a88c-4959-a34a-9e5cb3d719b2.pdf

Good results from Salasar techno with topline increasing to 125 cr from 82 cr & EPS to 6.14 from 3.45 YonY.

1 Like

Con call transcript on Q1 Fy 18. Management expects to finish with a Topline 475 to 500 Cr this fiscal with EBITDA margin of 9.5 to 10.5%…Big hope on Reliance Tower orders

http://www.bseindia.com/xml-data/corpfiling/AttachLive/c809b4d3-b24c-4435-8849-b1b41cf8d3da.pdf

GOI program of Complete electrification of villages by 2022 will help salasar to exploit the opportunity who are the suppliers of Power transmission towers, Flag poles, electric poles and a whole range of electrification accessories.

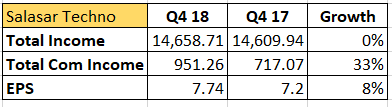

@Yogesh_s Salasar’s Q4 results is not good on the revenue side but profit growth seems to be fine. Would like to know your comments.

1 Like

Q4 FY 18 results are good. they don’t look so good in comparison to Q4 of FY 17 because Q4 of FY 17 was unusually strong in terms of revenue and also PAT. Q3 and Q4 are seasonally strongest quarters for the company.

Source: Capitaline.

1 Like

Hi

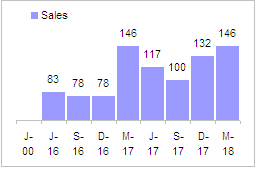

Salasar has posted a 39% QoQ revenue growth (41% growth in EBIDTA) and a jump of 12% from Q4FY18 to Q1FY19. Operating Margin remains flat at 9%.

Below is the presentation.

Rgds

Deepak

Sir, got the following info on screener website

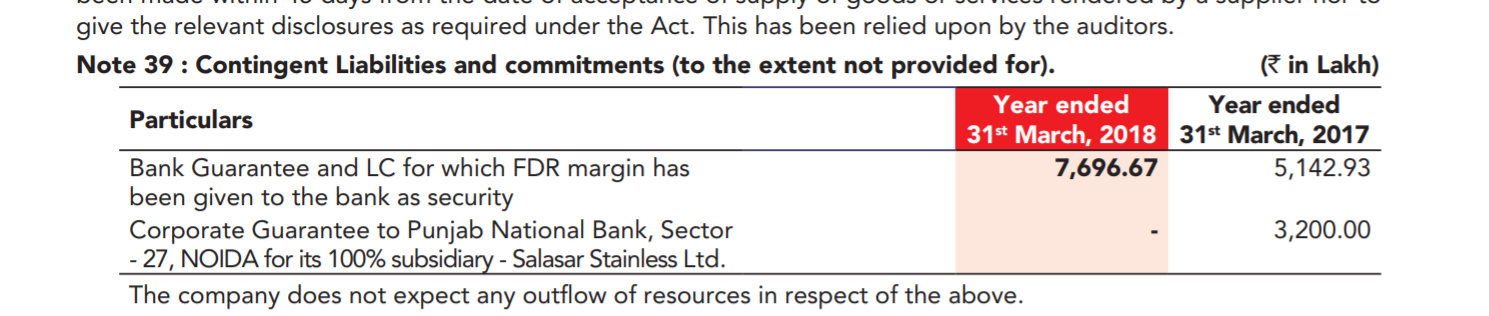

Contingent liabilities of Rs.243.16 Cr - what we should make out of it ?

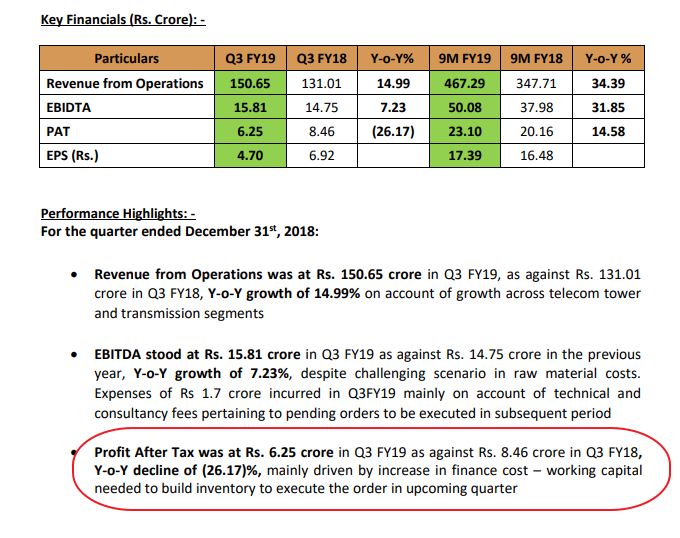

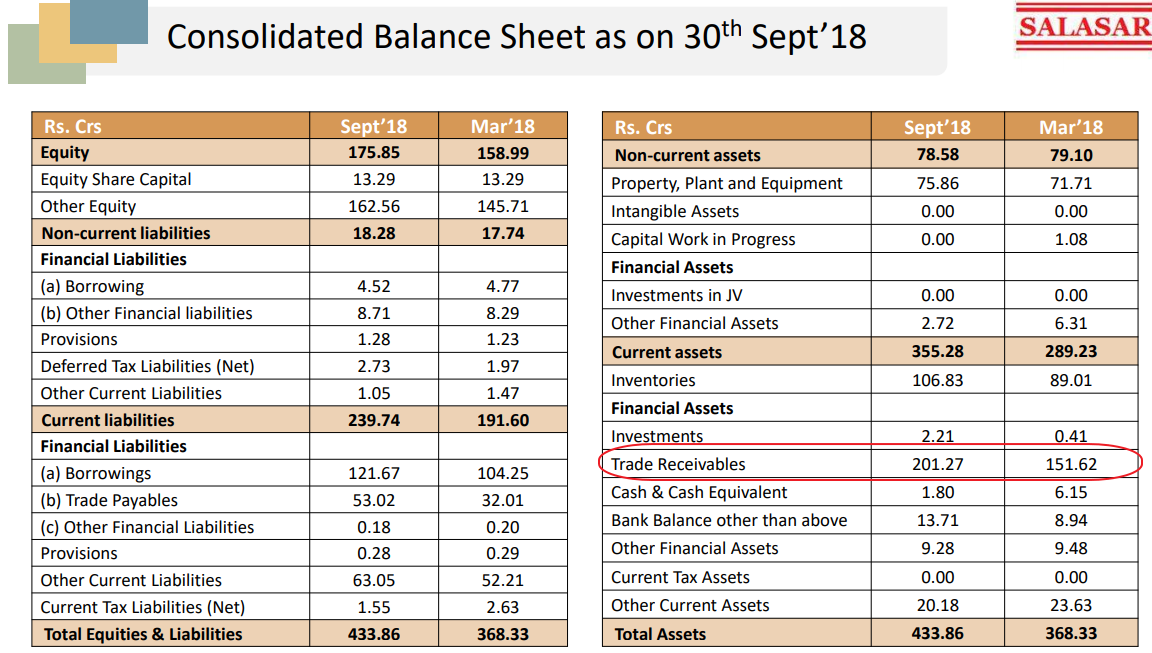

@Yogesh_s Q3 results are out with 26% drop in bottom line due to increase in finance cost. CFO has resigned. Stock price has taken a beating. You did highlight about Trade Receivables earlier.

Your views please?

Results are poor. On the top line they are getting impacted by the headwinds faced by telecom players (except Jio) and on the bottom line they are seeing a sharp rise in interest costs. Even the balance sheet is not looking good.

When the business is down, they should be able to reduce the receivables as they should still be able to collect cash from the orders delivered earlier. But they are saying that they need to invest more in working capital for upcoming orders. I don’t buy that. They are not able to get advances from customers for these orders nor they are able to charge higher margins by passing on these working capital costs. Raising working capital when there is credit crunch in the market is tough.

Overall, I like the field they are in but not able to grow fast enough for their size. Also balance sheet is going from average to weak. They could still come back and this quarter could be a one-off weakness, but there are better bargains in the market. Also when liquidity is in short supply in the market, companies with deteriorating fundamentals go down a lot.

Disc: I have recently exited bulk of my position.

1 Like

Beware!

This company is being pumped through social media!!

3 Likes