-

Transportation Logistics and Fintech two-sector where they will see more growth

-

Focus and growth will come from the US

-

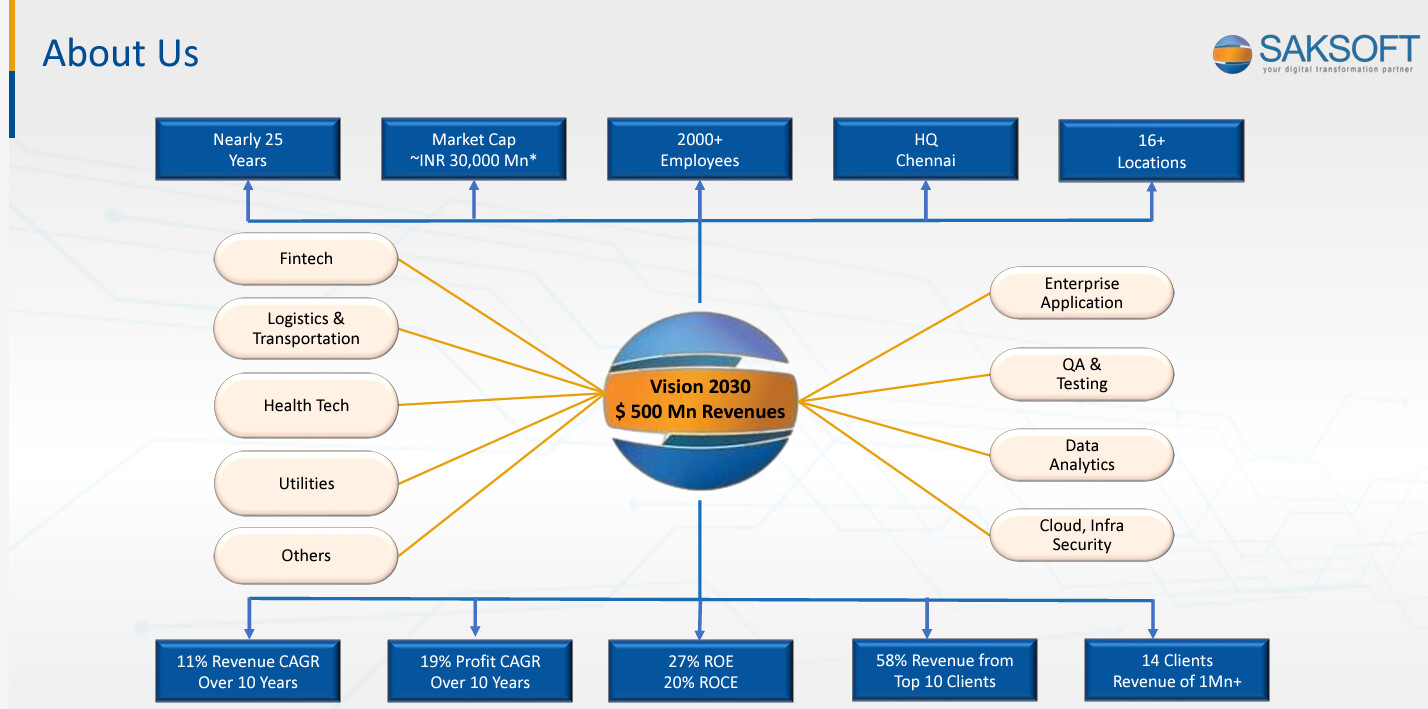

If they grow 25% YOY, They will get 500 million by 2030

-

Seeing 18% to 19% EBITDA margins

-

Confidence of hitting 100 million in this financial year

3 Likes

Promoter of happiest mind is very old , A trust founded will work as his successor.

1 Like

Q3 Concall Highlights:

EBITDA margin reduced due to choose to invest in sales engine to achieve $500mn revenue vision by 2030.

Q3 was tough due to US market head wind, recruitment cost of new employees to achieve $500mn. Q4 will be good, but head winds are there. It is reality check, as wake up call to make company stronger.

All acquired company were profitable when acquired and are profitable now.

Anticipated interest cut in US helps to spur demand.

Q4 EBIDTA margin at 18% is aspirational.

In short, company aspire to grow 22 to 25% to achieve $500mn revenue by 2030.

Disclosure: Invested

3 Likes

Q2FY25 Highlights:

- Revenue grew 7.1% q-o-q from 201 to 215 crores, although majority of it came from the acquisition of Augmento

- EBITDA at 17.08%: Lower than 18% because they gave wage hikes in July. Management said that they should see the margin back at 18% next quarter.

Management is now guiding between 870-1000 crores for FY25. They have confirmed that they have enough order book to meet 870 crores, however 1000 crore mark might be a bit difficult. They would still be able to reach close to that mark if the sales team they have been working on for past few quarters start delivering result.

Wrote my detailed thoughts here:

2 Likes

Looking for the financial model of Saksoft. Can anyone help me out?