Saksoft post outstanding result.

Net sales Sept 2018 is 23.93 Vs 13.92 in sept 2017.

Net profit Sept 2018 is 6.84 Vs 4.38 in sept 2017.

Saksoft post outstanding result.

Net sales Sept 2018 is 23.93 Vs 13.92 in sept 2017.

Net profit Sept 2018 is 6.84 Vs 4.38 in sept 2017.

Latest investor presentation. Is it only name dropping with Jargons or company means all this? Can Valuepikrs in IT industry thro some light?

The numbers are good, but the it’s business does not have a moat. Many IT companies doing the same thing. I don’t think they have pricing power.

The true test of how good the market considers the business, will be when IT sector is in downtrend.

Nothing special. Just a small size average IT service company. May show small spurts of growth once in a while if they win a good contract. Don’t expect any wonders.

It appears to be a well managed company with a high promoter stake. Would wait for the stock to get cheap. IT sector is currently doing well.

As per my understanding there is something special about Saksoft such as consistent dividend player, consistent earning, Low debt, net cash positive balance sheet, high promoter holding & last but not least quality of acquisitions in recent years.

Paying Dividend for a high promoter holding is self explanatory. Money goes into their pockets.

IT companies have no requirement for money. So Low Debt and net positive cash is generally the case.

Promoter holding is kept high to ensure stability in share price.

IMO, these are not positives for an IT company. But, non-negatives.

I would like to see how the numbers turn out in bad times. Let the IT sector take a downturn.

I partially agree with your views regarding any IT company in general but what differentiate Saksoft with others are their descipline, consistency in earnings over the years despite being such small sized IT company. They are giving sign of becoming mid sized company if they continue to perform consistently YoY. Seems well managed company with the kind if investment they made in the past & the manner in which they are acquiring capabilities by choosing the quality of company they acquire. Please advice on the valuation at which Saksoft is trading at present please. Thanks

investor presentation

@rshankv and @aerofire and @kumars1672

Doing an information dump on Saksoft here post studying the different verticals in the hope of reviving this thread:

They bought https://www.acuma.co.uk/ 1 in 2006. As per website… “Business Intelligence, Analytics, Data warehouse, Information Management, Cloud enablement and migration along with support, training, web development and testing.”

I’m 2013 and 2015 they added Electronic Data Professionals and https://www.360logica.com/ 1 which “A leader in software testing services and quality assurance, 360logica offers high-end software testing programs and test solutions to independent software vendors (ISVs), software product companies, and SMEs.”

So up until 2015 they were just another fly by numbers development and testing company and more of a human farm/body shop. In 2015 they rebranded from “Traditional services to Digital Transformation services” and began pursuing the likes of AI, Machine Learning, Big data, IOT etc… ie the latest fad words. This is when things get interesting… in 2016

They acquired https://dreamorbit.com/ 1 which

(DreamOrbit is an innovation driven Software Product Engineering company that engineers Platform Independent, Cloud enabled solutions in IoT, Mobile, RPA)

And finally https://www.faichi.com/ 1

(Faichi Solutions, is a technology company specialising in solutions and accelerators for the Healthcare companies)

Since this rebranding to digital transformation their operating profits from 2015 to 2020 have gone from 26 to 63 crores and op margins have increased to 17/18 percent from 10/11 percent. So all these additions have been doing some good even though they’ve only been acquired within 5 years.

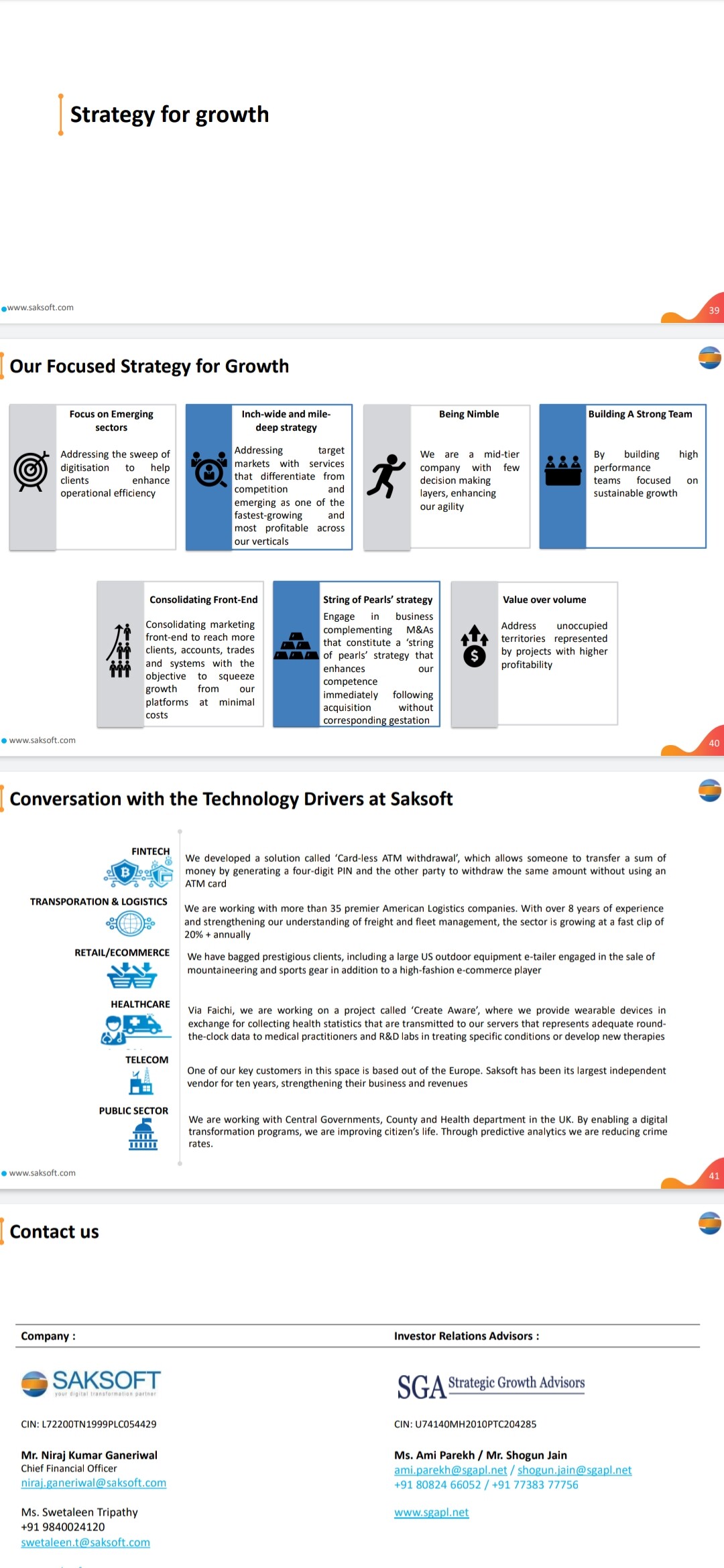

They now seem to be in a position to handle digitisation in telecomm, healthcare, fintech, logistics, retail, ecommerce and even public sector(though this has low margins and non sticky clients so management isn’t pursuing this too much).

These are examples of work they’ve done ie case studies in each vertical:

Fintech:

Built a cardless cash system enabling consumers, businesses and governments to instantly deliver cash to Recipients via

their mobile device

![]() Creating a Loyalty Management Solutions for the institution

Creating a Loyalty Management Solutions for the institution

![]() Ensuring Security through rigorous performance and security testing.

Ensuring Security through rigorous performance and security testing.

![]() Designed & initiated Cloud Optimization involving Database & Application migration from MySQL to AWS Aurora

Designed & initiated Cloud Optimization involving Database & Application migration from MySQL to AWS Aurora

Database

![]() Migration of customer’s entire infrastructure to Amazon Cloud Services

Migration of customer’s entire infrastructure to Amazon Cloud Services

Transport and logistics:

Digital Transformation Solution including order booking (via dedicated portal on cloud), shipment tracking (via IoT Solution),

real-time carrier status (via Mobility Solution), generating invoice (via collaboration tools), to predict peak load time (via

Machine Learning)

![]() Creating a cement vessel berth reservation system (CVRS) & stevedore application for the port

Creating a cement vessel berth reservation system (CVRS) & stevedore application for the port

![]() Designed IoT based Fleet Management software with features like Unit Information, Vehicle Tracking, Maintenance were built.

Designed IoT based Fleet Management software with features like Unit Information, Vehicle Tracking, Maintenance were built.

Server based event processing engine was built to capture GPS as well as many other vehicle operational parameters like

speed, engine on-off etc.

![]() Development of freight management software that automates operations right from order request to delivery, therefore

Development of freight management software that automates operations right from order request to delivery, therefore

increasing performance and reducing overall OPEX

![]() Order Tracking using UiPath RPA

Order Tracking using UiPath RPA

![]() IoT Application for monitoring of machines, remote access using custom protocols, CRM module to manage problems and

IoT Application for monitoring of machines, remote access using custom protocols, CRM module to manage problems and

incidents along with a chat system, mobile application, reporting and statistics.

![]() Creating a virtual warehouse for real-time workforce monitoring & asset tracking

Creating a virtual warehouse for real-time workforce monitoring & asset tracking

Healthcare:

![]() Designed a secure mobile platform that provides consumers with the necessary tools for aggregating, organizing and sharing

Designed a secure mobile platform that provides consumers with the necessary tools for aggregating, organizing and sharing

their medical health records. Built a framework for downloading data from the Electronic Medical Records using FHIR.

![]() Development of Analytics Platform for PHM and transition to Value-Based Care using Advanced Population health

Development of Analytics Platform for PHM and transition to Value-Based Care using Advanced Population health

management (Prediction and Machine Learning), Post discharge patient communication (Artificial Intelligence) and Value

Based Care Analytics (Performance and Regulatory reporting)

![]() Designed data warehouse & implemented SAP BO. Due to customized analytics and reporting, now the client is able to

Designed data warehouse & implemented SAP BO. Due to customized analytics and reporting, now the client is able to

respond faster during emergencies.

![]() SAP SuccessFactors implementation for a hospital chain.

SAP SuccessFactors implementation for a hospital chain.

![]() Oracle data warehouse for a Pharmaceutical company.

Oracle data warehouse for a Pharmaceutical company.

![]() Patient After visit summary (AVS) using bots. This helped in improving patient engagement. The visit is documented and

Patient After visit summary (AVS) using bots. This helped in improving patient engagement. The visit is documented and

available anytime to patient as well as provider.

Retail and e-commerce:

Created customer360 dashboard (using Hadoop, R & tableau) which will help them to profile a customer, forecast their

sales and help in conversion rates

![]() Leveraged Big Data and improved their average order value by 53% through personalized marketing.

Leveraged Big Data and improved their average order value by 53% through personalized marketing.

![]() Building and managing their B2B and B2C ecommerce stores. Currently the stores are for US and UK. We also built their

Building and managing their B2B and B2C ecommerce stores. Currently the stores are for US and UK. We also built their

backend system to manage orders and inventory. Faviana wants to go fully ecommerce by 2020

![]() Building and supporting their ASP.Net Storefront based ecommerce portal.

Building and supporting their ASP.Net Storefront based ecommerce portal.

![]() Migrated their legacy portal to a new Magento 2.0 platform and supports their engineering needs for the portal

Migrated their legacy portal to a new Magento 2.0 platform and supports their engineering needs for the portal

![]() Provides product engineering services to Trader Interactive in the areas of web development. It also has a dedicated QA

Provides product engineering services to Trader Interactive in the areas of web development. It also has a dedicated QA

team for third part testing.

![]() Dedicated QA Testing team for Target

Dedicated QA Testing team for Target

Public sector:

Digital Transformation project to use data from multiple sources. We were able to identify a customer journey (cradle

to grave) & service user journey.

![]() Providing assistance with the SAP Predictive Analytics tool for modelling and predictive visualisation to understand the

Providing assistance with the SAP Predictive Analytics tool for modelling and predictive visualisation to understand the

movements of the organized crime groups

![]() Patient data was collected from around the UK from numerous NHS Trusts, Primary Heath Care Trusts and local Heath

Patient data was collected from around the UK from numerous NHS Trusts, Primary Heath Care Trusts and local Heath

Authorities. The data was used to identify early signs and trends of bowl cancer.

![]() Worked with the university to identify patterns and trends that cause students to drop out causing a drop in funding

Worked with the university to identify patterns and trends that cause students to drop out causing a drop in funding

to the university. We helped identify interventions required to ensure students do not drop out and maintain their

attendance

![]() Created Berth Reservation System and helping the port to improve efficiency

Created Berth Reservation System and helping the port to improve efficiency

And this is their strategy for growth

Recent concall Aditya Krishna says a similar story… “We have been witnessing reasonable demand from some of focused verticals of Fintech,

Transportation and Logistics, and Healthcare and e-commerce, renewing our confidence of a

poised growth opportunity ahead. Our expansion into the infrastructure managed space in 2019

was timely. With the pandemic, the relevance of cloud, remote working, virtual desktops have

increased, and is an enabler for the growth at Saksoft.”

Sorry for the long post. The case studies took up a lot of space.

Is there any potential here based on the above?

Sidenote: Q3FY21 was their best ever quarter registering 12 crores(26 percent higher YoY) and debtor days improved from 80 to 100+ days in 2015 or so to under 60 days for the first time in Q2FY21. return on assets and capital employed steadily improving and are now at record high levels as their acquisitions get time to perform. They are also net cash positive and have minimal debt now approx 27 crores which can be easily covered with their cash in hand ie 68 crores. Best position they have been in debt wise in a decade too. Technically charts show a multi year breakout too with good support forming.

Negatives are that latest quarter 60 percent of their revenues were from their top 5 clients which is shockingly scary since they are exposed to one sided renegs/losing huge revenues if losing a client… and since majority of their revenue is from the USA they are exposed to currency fluctuations and issues in the US. Also I dunno If they have any sort of moat. At best they are just a nice well run small company in a sector with Tailwinds which has slowly but steadily improved on all facets over the past decade

For a size and scale of this company, they are carrying 150 crore worth of goodwill on its balance sheet, if I knock it off, the entire networth or the balance sheet is gone.

Just for instance, 250 crore worth of networth, 150 crore worth of goodwill, this result in 100 cr worth of tangible networth and against this the company has 90 crore worth of cash on its balance sheet.

I failed to understand the moat in this.

Barely few clients in the portfolio, company with long history still not been in a position to create sustainable market for itself and this is at a time when IT industries flared up in last two decades.

Paltry sum of revenue growth even during the period of pandemic, this is after focus on telco and healthcare, is an area of major concern.

Investor presentation has a dedicated section on investment thesis. Rest all gyan in the presentation is just gyan and I don’t see any material uptick in numbers, except the noise.

Current valuation, adjusted for Goodwill, is super stretched.

Disclosure: No investment.

Yup @blueeyedinvestor After my post above I did a bit of scuttlebutt and found nothing exciting about the company at all. Its one of those grow by acquisition companies which in itself is a red flag. Their actual growth is horrible with plans for growth through these new subsidiaries. Was an interesting technical bet at 330 or so but nothing else. Agree with you. I decided to just forget about this company and throw it in the lessons learnt bus.

Disc: not invested.

Yup @Shakti_Srivastava . I’m happy for them. Nice company and management. When I studied this company back in February they looked like they were on the verge of a turnaround due to both commentary and technicals and have set a good 12 crore per quarter base since then. Management is very open too. While it’s been a very profitable few months since February ie a 2X bet already… This was just the retracing of a very undervalued bet to its right price imo and from now on for further re rating they need to break their 100 crore revenue barrier. They may do it but there is a chance that they could stay stagnant for a while too. If they do get their various subsidiaries that they’ve bought out to continue firing they could have a profitable few years… though, once they hit a point then future growth would then have to come from further acquisitions which is a coin toss. I’ve posted a detailed note above regards the pros and cons of saksoft. I hope they help you if you are researching this company. I wouldn’t bet against them continuing a run both profits and re rating wise in the short to medium term. Cheers.

Hi anyone tracking this company recently or any updates?

Noticed there has been lot of changes and can be seen on price level too.

Good to have someone’s recent view

On February 15, 2022 that Saksoft ) has

completed the acquisition of Singapore based MC Consulting Pte. (www.mcconsulting.com).

MC Consulting Pte Limited is a Singapore based company specialising in providing technologybased business solutions. Over the last 15 years, they have custom developed multiple solutions

that improves the functioning of a seaport and public sector agencies.

Speaking on this acquisition, Aditya Krishna, Chairman & Managing Director, Saksoft said:-

“MC Consulting’s domain expertise and experience in providing smart seaport solutions aligns well

with our Logistics & Transportation focus. This acquisition fits into Saksoft Group’s strategy of Inchwide-Mile-Deep focus that helps us reinforce our niche in the otherwise crowded market”

I think this company is still undervalued compare to other smallcap IT players. Lot of potential to grow

( # Disc: invested)

Company continues to post good numbers. Revenue grew by 42.8% in Q2FY23 compared to Q2FY22 and 10.7% over Q1FY23. Would like to see EBITDA margins going up from 15-16% to 25%, if that’s possible, and lower client concentration. Still tend to believe PE of 16x basis TTMEPS is on the lower side.

Does any one have any connect with exiting employees in SAKSOFT. I been holding this for 5 years suddenly 40% growth from last 4 Qtrs. so want to know what is happening and know more about management

Any one can help to understand the difference of business between happiest mind,latentview and saksoft ?

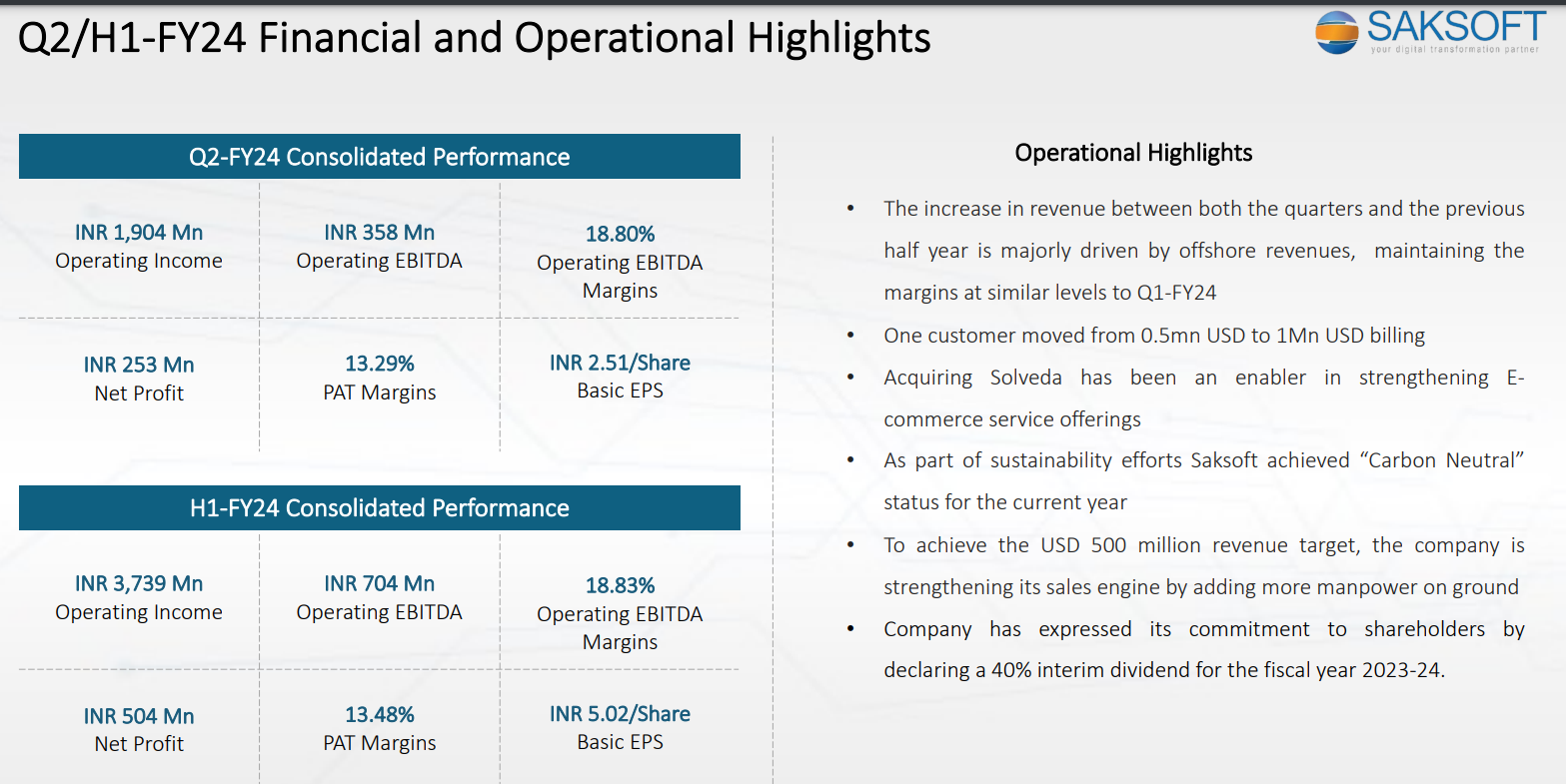

One more quarter Q24 with very good results … any insight any one have … con call in awaited for Jun Q … waiting to hear management commentry

Another quarter of steady growth.

Investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/18ddb9ed-ee7e-410d-a5f4-f4230cd7b77f.pdf

Disclosure: Invested