This 2 years old report totally got it wrong

The short thesis had factual mistake, and most likely lost all their capital (co quadrupled from there on price & more than doubled on revenue)

Shorting is not an easy game to play

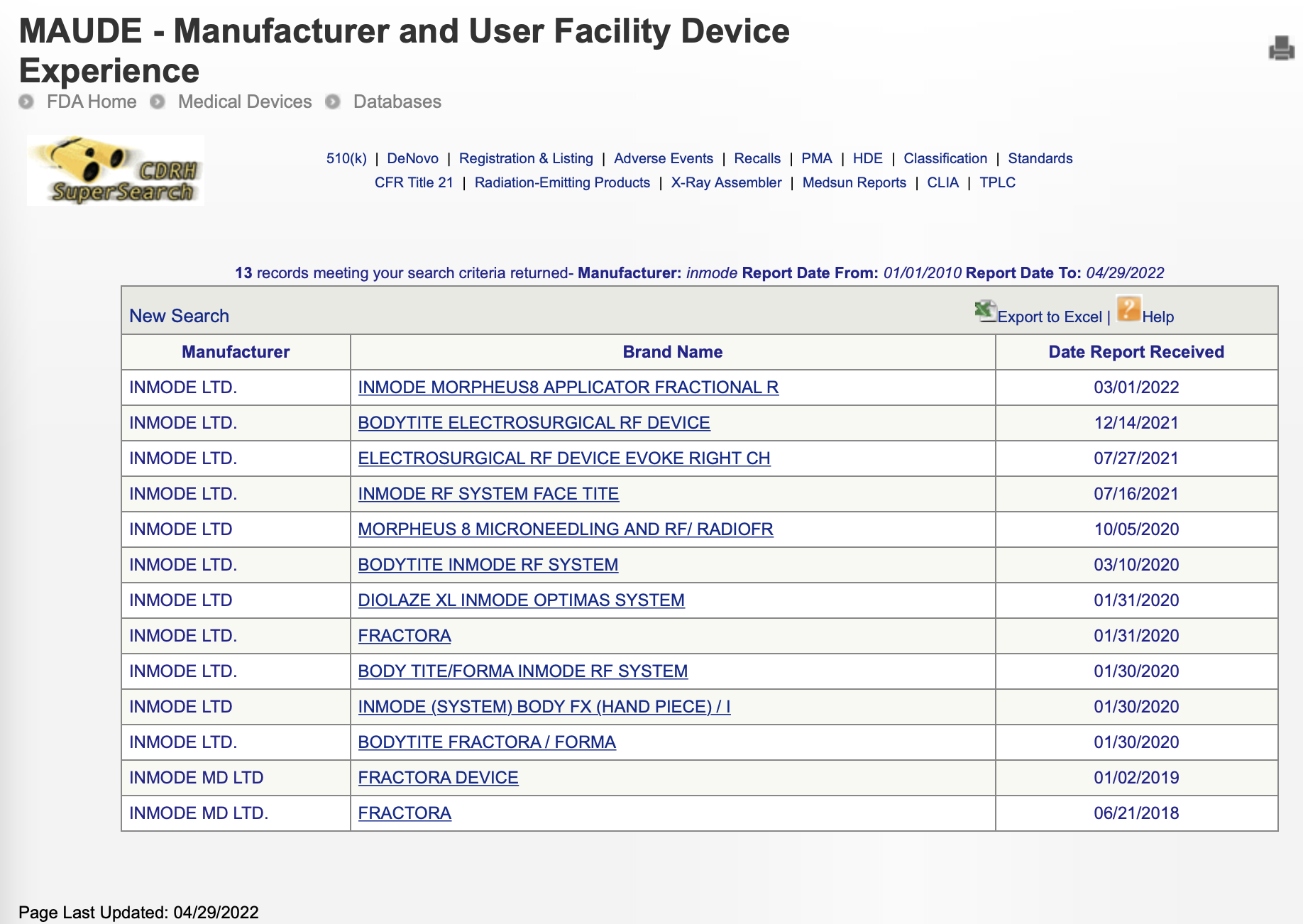

Factual mistake part : check usfda website. Inmode has one of best track record of adverse events. 7 out of 1 million scans they have done.

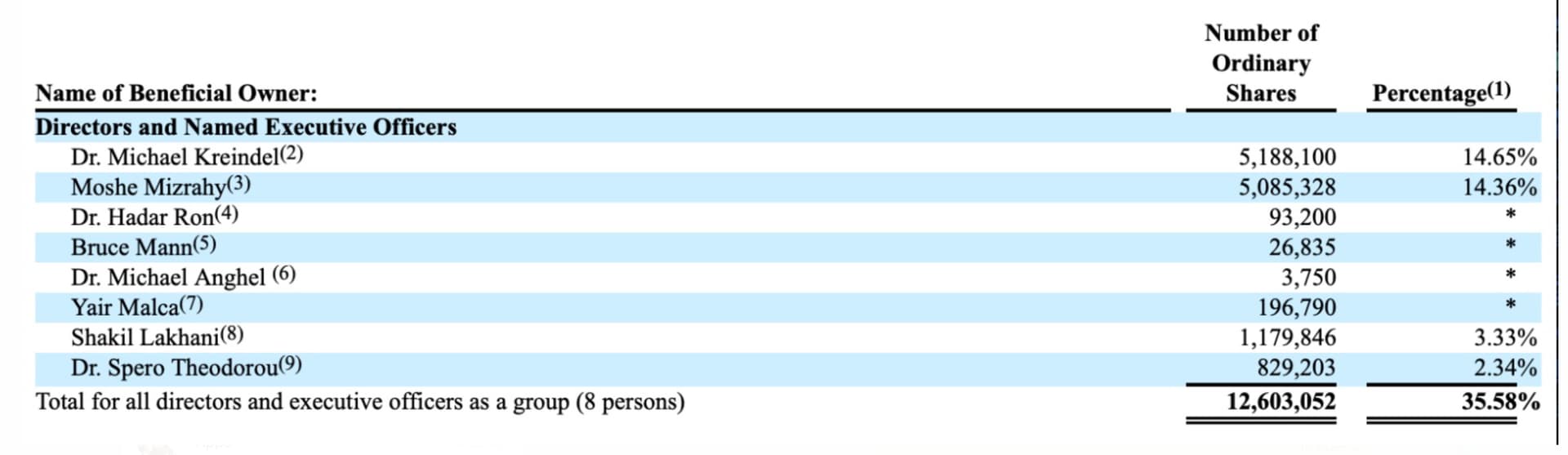

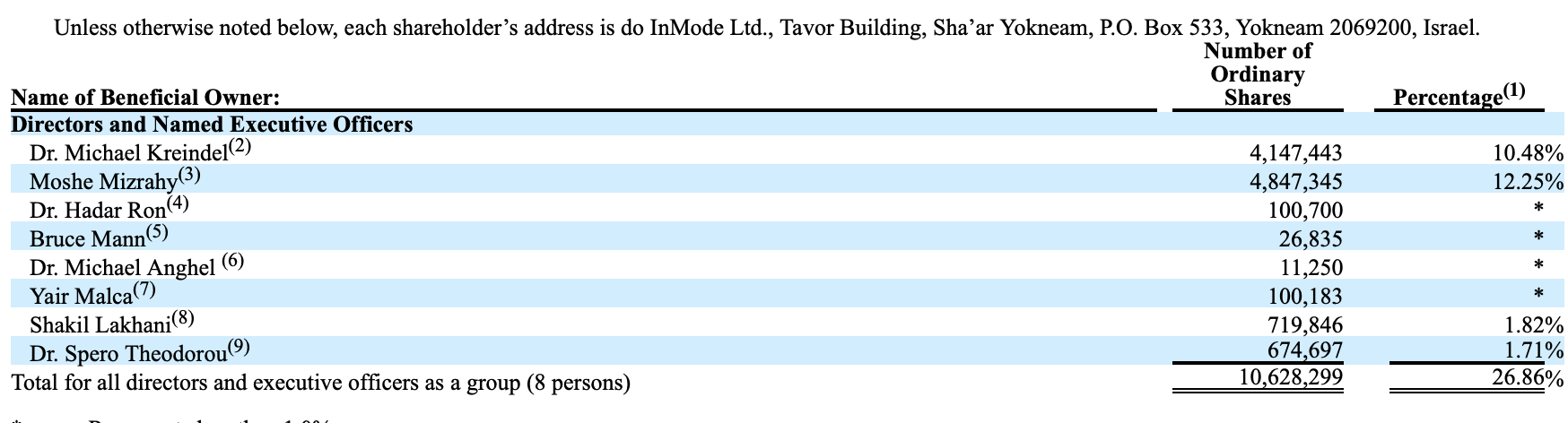

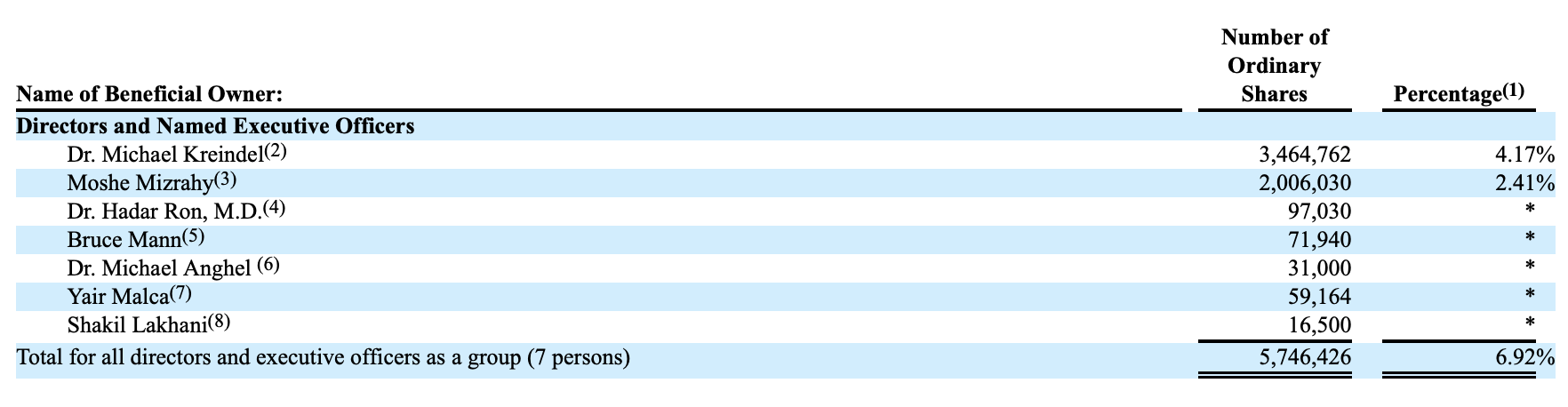

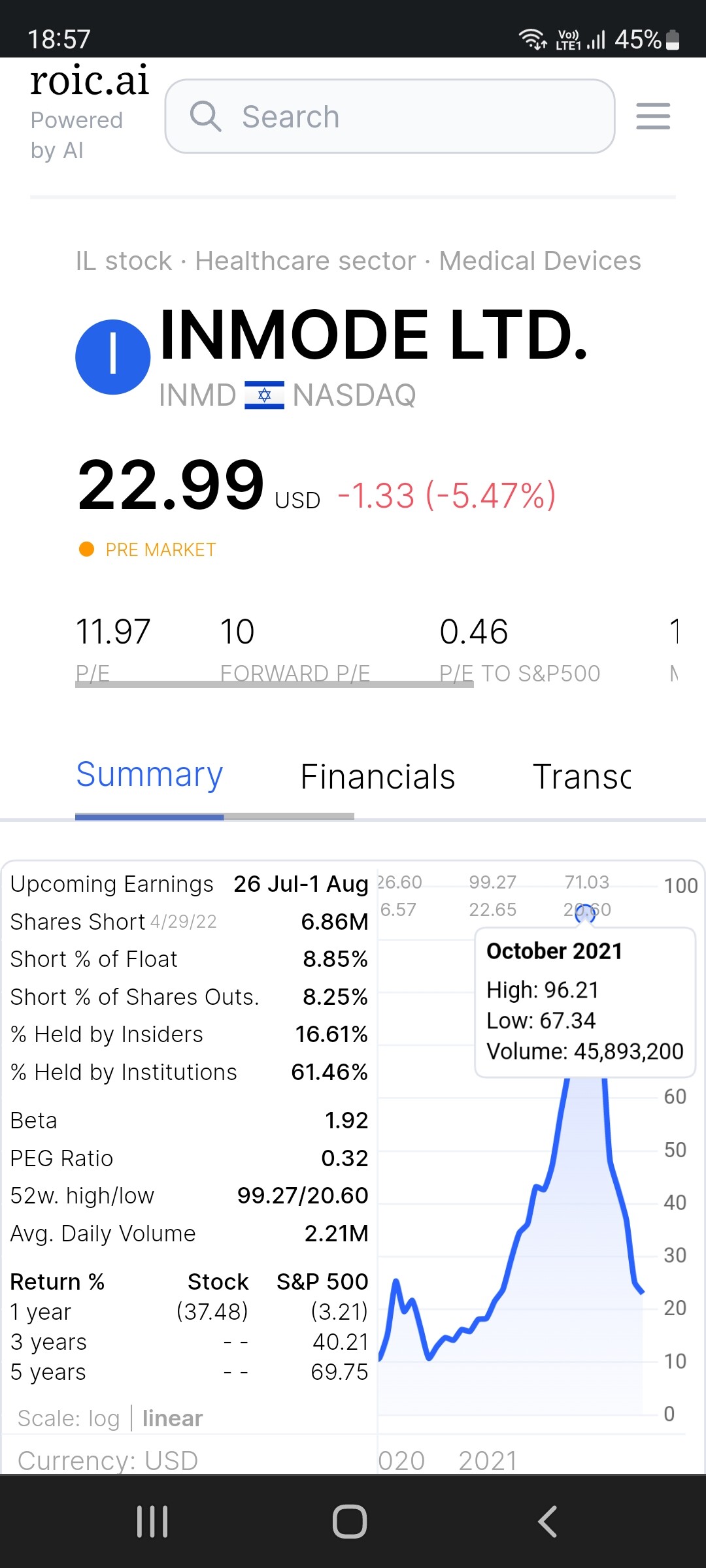

There was a split in between 2020 and 2021. So insiders sold almost 75 % of the holding.

Having said that this does look like a good Risk:Reward as they have a strong balance sheet. But its better to find out why insiders are selling that too large quantities.

Already shared in my very first post but looks like it’s easier to quickly reply than watch a 40 minute video

No, market is not punishing for this or that. This selling info has been very well known for years. Stock peaked in October 21 along with rest of market

We can smack any narrative on price movements, but that only shows our ability to follow price, not the causal relationship between the reality of company & stock price

Insider selling is never easy to digest but that leads to lots of speculations. From 2020 to 2021 holding went down from 21 Mill shares ( including spilt ) to 5.7 Million. So Im not sure market knew this all along. Price may be coming down along with the selling or insiders panicked and sold along with the market fall. Its as good as anyones guess. But this is not giving any comfort.

Dear Sahil,

I have no idea about INMODE 's non India business, but when it comes to their medical devices business in India, especially Dermatology - they are a long way off.

The market is already quite saturated already with high end Israel / American machines at one end and the cheap Korean / Chinese machines at the other end.

INMODE is quite a late entrant in a market which is already flooded with low end Chinese machines and where the entry barrier is extremely low ( only India business).

Please do the remaining scuttlebutt since I have absolutely no idea about non India business.

I went through the video you shared and came across a good report (link below) recently written after their FY21 results.

The report has raised a question about stagnation in recurring revenues, do you know any specific reasons for that? Given the increase in number of devices, shouldn’t the recurring revenue increase at a faster pace? I haven’t looked at Q1 numbers yet, do you see any pattern change over there?

Dr saab, thank you for sharing the feedback

Value of human life is close to 0 in our country

India mei we would want to do everything “for cheap” whereas inmodes entire selling point is “quality & safety”

Comparing inmode with Chinese machine is like comparing Tesla with byd or tata Nexon. They operate at different price points.

Presence in india is for namesake for inmode. Their main market is developed market. The TAM is 2 lakh doctors out of which 1 lakh are in usa. That gives us a good indication for the people who are in their TAM.

Of course their machines have few takers in india, one machine costs 1 cr. The only difference would be in terms of 1 having 7 adverse events per million procedures, other having 70 or 700. But really, would we pay double or triple per procedure for safety? Possibly not.

If you know of any doctor who uses inmodes machines, i request you to please put me in touch with them so that i can understand the scuttlebutt on the machine itself better.

Also, can you please also share names of high end Israel/American machines which are used? Would love to read more on them.

All other questions : the answers are in the concalls, investor presentation, video please watch them.

Although Inmode is a good company, I would desisit from putting it in the TESLA mode. It is not the market leader in its segment, even in USA ( at least in Dermatology, and most probably other specialities too). Although that doesn’t make it any inferior as an investment bet.

On your second point, Indian market seems very appealing to them because of the massive doctor population here They are trying hard to establish their presence in India medical community but haven’t been very successful yet ( Imagine their TAM growing 10 fold to 20 lac docs if they can penetrate the Indian market).

On your third point, Inmode doesn’t have as exorbitantly expensive machines as mentioned. Their average machine price is in the range of 20 - 30 lacs while some other’s lasers are priced at around 50L for the same technology. What matters here are the post sales service and marketing support you can provide to doctors, in which the company is still in nascent stage in India. I would say it lies in between the chinese suppliers and the more premium suppliers. Of course, you can’t ignore the Chinese here since they will provide a similar technology to you at 1/4 th the price… Too tempting to ignore completely…

Finally, the more premium companies in this segment are FOTONA, LUMENIS ( America), ALMA ( Israel) and BTL Aesthetics ( Australia) to name a few. These are truly global companies. Don’t know if any of them are listed anywhere.

Ankur, the laser machines are commodity. The more interesting part of the business are the radio frequency treatements (these are the machines which sell for 1 cr or 150K$).

Any feedback on the RF machines ? This is the space where they claim to have IP protection, better machines than competition etc

I’ll study to he 3-4 names you’ve mentioned as well, thanks for sharing.

Here are the notes from the investor conference for those who still havent seen it:

Needham investor day conference notes

Did 31% YoY Q growth. In medical equipment category, Q1 is slowest, Q4 is best

Supply chain problems still there: electronic component shortage, high prices, logistics

GM suffered by 1.5% due to RM & logistics inflation.

Record Q for consumables. Little bit lower GM.

Consumables: 4Q: 11%, 1Q: 13% of revenues.

Is pipeline drying? See consumables. 120k surgical in Q4. In Q1: 160k consumables for surgical.

Did not benefit from corona, did not get hurt. Lost biz in China, Korea, Japan.

Have 3 suppliers per component. Tougher negotiations for components. Delivery time, prices, volumes.

Lost all biz in Ukraine. 3M$ / year (~1% of sales). Russia cannot transfer money. Sanctions. Russia is about 9M$. Lost 50% of it in Q1. (Total ~3% of sales)

CFDA slower than used to. 2.5 yrs wait for 2 more platforms. (Only approved for 3 platforms). Partially due to Covid (busy). They are not against foreign companies. Hospitals are full of equipment from overseas

95% of deals are financed with loans or leasing in US. Interest rate wont change the economics drastically. 3000$ to 3100$ to 3200$. Payback period goes up by 1M only.Interest rate on leasing has not gone up yet

Recession demand: Depends on how deep recession would be. If its like 2008./09 it will affect us. People who spend 5k or 10k on aesthetic surgical treatement are notreally affected. Botox etc people might postpone.

FDA issued warning to apex medical company: Reason: coz of safety issues. FDA adverse effects apex jplasma: 70 adverse effects reported. Inmode has 7 from 1st day from body tite. Body tire, necktite, we are measuring temp every 1 microsec whenever temp goes above proton temp, system stops immediately. When you apply LU plasma, you cannot measure the temp. Going from 44 to 47 creates burn. People who buy JPlasma looking for cheap product: 60k$. Bodytite 130k$. In Colombia, insurance companies send them a letter that they won’t get insurance if they use JPlasma equipment. This would happen in other countries too. Never happened to Inmode

5700 in US: minimal invasive, non invasive, hair removal, hands free everything included is 5700. Surgical (minimally invasive) is around 2k. Mainly plastic, deem surgeons for face. 20k such doctors. Aesthetic doctors. We’re about 10% penetrated.

EmpowerRF: 7procedures we can do with it: vaginal contraction, SUI, pelvic floor restoration, lavivaplastry, tone: muscle simulation after pregnancy, Morpheus8: laviar treatement. Aesthetic, medical gynaecology. Minimal invasion laviaplastry. 1Q was 1st Q of selling it. Maintaining 20M$ guidance for empower.

VisionRF: original plan was 1Q. Now plan is 2Q2022. 50 systems in Canada launch.Dry eyes, wrinkles, accutite: lid tightening. Launch in US in Q2 or Q3

40k gyaenacologists in US. 15k ophthalmologists in US. After 1Q we will give firm estimate for visionRF sales.

Competitive advantage: Everything any competitor can do: We can do & more. In a tradition medical study: laser, non invasive RF: We have everything competitors have. We have another segment Hands free: We have some competitors, but no one has hands free for face or body. Coming out with 2nd gen. For surgical (minimally invasive) procedure, we have no competitor, we are alone. We have the technology. Do we compete on laser? Partially. We do have it, but keep it as complimentary tech (not the main focus). Want to be 1 stop shop. Widest portfolio. On laser, don’t have great IP protection. On Surgical, minimally invasive, ablative, fractional RF, we are the leaders (nobody else has the tech).

Competitor: Thermi. Started in US. Mono polar RF not bipolar RF. Sold to Spanish company. Tried to run in Europe. Changed hands again. We don’t see them in US.

R&D spends: 2% of sales. R&D should not be measured by % of revenue. What matters is productivity. Coming up with 2 platforms/indications every year. Competitors develop 1 platform every 3 years. We must see the quality of R&D. Very good engineering team. Best knowledge base for bipolar RF. 10M$ of R&D spends: mechanical, clinical, electronic engineering, we do everything in-house.

Gross margins: 85% of gross margins are sustainable for us. It’s determined by uniqueness of the technology. Best laser is 70k$. We are selling 130k$. 85% GM is a must. It is not a nice to have. Everything has been developed with that aim in mind.

Competitor settled, they can only use micro needling, cannot use fractional RF. Their tech does not have return electrodes. Do not crate any effect any effects in epidermis. If they use this, they need to pay us money.

Longer term (2023, 2024): ENT (sleep apnea, soaring) , Erectile dysfunction (shock wave & bipolar RF).

2 key takeaways: Competitive advantages, TAM (key drivers of sustained growth period).

Disclaimer: Have a small investment, positively biased.

Hey would be good to know how has last few months worked for you, what strategy you followed and now what are your strategy on these recession/bear possibility…thanks

Are you holding on to your picks, buying the dips or coming/already come in substantial cash?

Last few months have been a source of great learning for me, personally. I had the privilege to meet many many great investors in person. Learn from their experience. Internalise their mistakes & reflect on my own. A few learnings:

Averaging down: My previous self found lower prices attractive for a co which i have already studied deeply & have conviction on. Easiest canonical example here is IDFC/IDFC bank. Lower prices? Sign me up for backing up a truck & loading up. WHat i learned through experiences of seasoned investors is that often times, markets can be leading indicators to fundmentals which is why technicals possibly should find space in the portfolio of any fundamentals investor. Note that this is not to say that every “breakdown” is a sell, what to do with that signal is up to each investor. But i am now more likely to think “market is signalling to me that it vehemently disagrees with me, what might I be missing?” More aggressively trying to find anti-thesis pointers, trying to understand the psyche of the investors & non-investors alike for this specific co & revisiting my data which might be source of my conviction. Even the best of investors only have a strike rate of 5 or 7 out of 10. Making mistakes is the name of the game in a probabilistic game. It is important to be even more aggressive in seeking out anti-thesis than one is in seeking thesis pointers for investments that we have made. Because we might love a stock, it surely does not love us back. ANother co where technicals led fundamentals is angel one. Co made a 2022 & then started trending downwards. I sold at 1700 after the fundamentals confirmed it.

Recession is coming what can we do?: I can do no better to quote the father of investing who spoke on this very subject this year & extend it. Buffett’s original: When inflation is high, Warren Buffett says the best thing you can do is ‘be exceptionally good at something’ My modification: When recession comes, become even better at what you do, indispensable to society & create tremendous value for everyone you meet. My plan is to become a better software engineer, a better investor & most importantly a better human being.

The PE bias: Probably the least talked about bias in investment community but MOST important bias that exists is the PE bias. 99% of investors are affected at least 50% of time by this bias. We look at PE ratios. We already form an opinion on whether we want to own the company or not. Then, we try to look for confirming evidence that supports that bias to own a low pe company. Such is the hold that graham’s original value teachings have on our psyche that a low pe becomes the rationale, & business analysis becomes a tool to rationalise the decision to own a low pe stock. In the market there are no absolutes. In fact, there are no rights or wrongs. Having said that, we have to be cognizant about fact that what are other investors thinking. In essence learning#1 urges us to be humble & first ask the Q why this stock is LOW pe. Is it low pe because we just had a 53% market crash (true for small caps for 2018 to 2020 low). Then it probably is ok to own a low pe stock. But if we are in middle of roaring bull market, the base rate of success going after low pe stocks is low. Why is it low? We will cover this in learning#4. Most important thing for us is be skeptical. THis means, for a low pe stock, we need to ask “why is this so cheap?” Start by finding anti-thesis. Talk to investors & ex-investors. While investing is a lonely pursuit it is paradoxically more social than possibly any other pursuit. It is like a group of people driving together towards a destination each in their own individual cars. For a high pe stock being skeptical means finding out whether it truly deserves a high valuation. What are its competitive advantages, its TAM, its execution capabilities, its industry structure, its right to win. Other problems with PE is that earnings might not be normalized which is why business analysis matters. If we dont know the E, how can we know the PE? Abnormal power costs abnormal freight costs, abnormal RM costs are just some of the problems our cos are facing. Look at this co. Screener PE of 28.8. This is where the layered cake approach comes in. Type1 market participant looks at price alone. Type 2 at the screener PE. Type3 might see the P&L. Type4 will reach the annual report. Type4 will be at an advantage because they will realize that large part of Other expenses is actually “freight costs” which is why the jump from 9cr to 17cr in Q4 is abnormal & a more reasonable other expenses in a normalized environment would be around 13 cr. THis would add 3cr to PAT Mar-22 Q. We would end up with 8 cr PAT. Typr4 investor wont stop there. They know that we are truly paying for company’s current earnings power & that biz is not seasonal. WHich is why they would be comfortable to annualize the Q4 pat to get 32cr of earning power. With some margin of safety they would estimate co can do 25-30cr annual profits in a year as it stands today. That same co goes from being 29 PE to 18-20 PE. THis is why business analysis matters. How can we value that which we do not understand? We are valuing cashflows. We need to Understand the cashflows.

Are the markets efficient or inefficient: WHat makes the market efficient? it is the hardwork of alpha chasing investors who make the market efficient. Imagine a low pe co which is doing truly great work. Hard working investors will find that co, understand it, build a position & help others understand it. THis means the very act of chasing alpha actually reduces alpha & makes market more efficient. it is through these hard working investors that alpha gets created in being created so, gets destroyed. i met many such investors in last 4-5 months and am convinced now that it is definitely a useful exercise to ask ourselves why this population of 1000s of investors might have skipped a low PE company. It is worth discussing with them with the understanding that all communication is biased. By separating the biases from the facts (more on this later) we learn to understand the true nature of reality. I am not saying that one needs to trust or rely on this cohort of alpha chasers blindly, i am saying though that one needs to sample them, talk to them & understand their general population level opinions & understanding of the co we are seeking. Because these are the people who make the market (at least partially). The very act of chasing alpha makes market more efficient & drives down alpha. THis has been one of my key learnings.

In God we trust, everyone else must bring data: True to our theme of blindly relying on western investment idols & ideals we believe in the power of scuttlebutt. What is not appreciated enough is the type of scuttlebutt. Anyone who understands science understands 2 important facts: (i) anecdotal evidence is not a substitute for statistical evidence (ii) Every human has biases. In god we trust. Everyone else must bring data. In doing scuttlebutt i have observed that most humans, unknowingly only communicate with their biases. Very few are willing to bring data to the table. Unless the purpose of the scuttlebutt is to understand their opinions, their opinions distort the reality field & helps kill a good investment thesis. Lots of examples. IT professionals being excessively bearish on IT. Saying there is nothing great happening at any of these cos. Chemical professionals knowing how hard it is comply with environment norms & how difficult it is to run these factories & thus dismissing possibilities of these cos ever getting good valuations. Banking professionals claiming to know inside & out of banks based on past history of the banker (of course, because people dont evolve or change or improve, they are static). The human mind registers negative experiences with 2x impact of a positive experience. THis is why it is important to rely on a broad sampling of professionals or scuttbebutt experts rather than 1 or 2 or 3. If that cannot be done, find other sources of data. Use digital scuttlebutt, Read google maps, google app store reviews, rely on unbiased statistics which average across biases of many people. See google trends, website traffic analysis. Trust in a God if you must, but please request everyone else to bring data, not narratives or opinions.

Who am I?: Perhaps most important thing in investing is to know ourselves. This is itself a moving target because we constantly learn, evolve & become better versions of our older selves. I have been trying to develop a framework for the type of investments that i am most comfortable doing & why. I am ready to share some initial thoughts on my investment framework (which will of course evolve over time).

Disclaimer: Any co i mention is purely for knowledge sharing purpose , it is not an investment advice

All of market participation can be boiled down to the market economics of demand & supply. Price action folks look for demand & supply of stock. Investors should look for demand & supply of goods & services produced by companies. There is a lot to impact here.

Demand side

What produces a demand for the goods or services of this co? What basic need is being met? The ability of the investor to answer this question precisely tells us about their understanding of the business. A pitti engineering investor should know about eddy currents & what is the use of the laminations pitti produces. A SBCL investor should know that the shunts help measure current in BMS or smart meters which is needed either to ensure that we do not short the circuits by mistake by running excessive current through electric circuits or in the latter case to precisely compute present electricity being drawn to better plan demand & supply & create a feedback loop with producer. The ideal investment opportunity: In an ideal investment opportunity this answer would either be a critical application product, a lowest cost good or service, a critical human need (a need not to die which is what pharma fulfils), a habit (liquor, cigarette, burgers, pizzas). One would realize that this innocuous looking question actually helps us understand the competitive advantages or moats in the business. Related questions like “Which other product/service can meet this demand? How realistically can it do that today?” will help us understand risk of substitution, technology obsolescence eg: diagnostics of disease is the need. Diagnostic kits kilpest makes are the goods which meet that need. However, one talk with microbiologists tells us that RTPCR kits are not only game in town. We have ionized protein methods, rapid antigens (which are 10x lesser remunerative than rtpcr), biopsies for cancers. Answering these ancillary questions will actually help us understand the industry structure, threat of competition, competitive intensity & threat of obsolescence much better.

How rapidly is the demand growing?: This tells us about the industry growth rate. Rising tides lift all boats. We ought to invest in a sunrise sector at any cost & run away from a sunset sector at any cost as vijay kediaji tells us. Demand for EV is growing very fast. Demand for solar panels is growing very fast. This is why shunts will do well. MCUs will do well. (note that i am only talking about the products doing well, not companies). Demand for diagnostics is growing well. This is actually a latent demand because the patient does not even know demand is there. Doctor did but was unable to help because 90% of our govt hospitals did not have a good lab. Any co which helps govt labs meet this unmet latent demand will probably do well too. Estimating the growth of product/service demand helps us understand the base rate of success. With higher base rates, market will be willing to give higher valuations (provided the TAM/opportunity size is also large enough).

Is the demand cyclical or seasonal or structural or shallow cyclical?: One should now immediately appreciate why pharma or chemical cos are hard to analyze. Each molecule is a microcosm of economic forces in & of itself. Demand for cold medicine is seasonal. Demand for AIDS medicine is not seasonal but is slow growing (2-4% per year). All domestic discretionary spending demand is seasonal. Indians spend more around festive season in Q3. All footwear, jewellery, auto cos will see more demand in Q3. Part of the Demand for build materials is cyclical because they are closely linked to real estate demand. One needs more structural steel tubes, more PVC pipes, more paint, more MDF panels for furnishing in a real estate up cycle than a downcycle. This makes demand partly cyclical for these building material companies. Same for capital Goods. Capital goods demand would arise out of capexes. Pitti’s motors will sell more when capexes happen. A very good mental model to use here is: to what extent is the demand in sector for replacement & to what extent is it for a fresh sale? Replacement sales should be given higher multiple specially if they are consumables since this is a steady certain predictable cashflow. Refractories, ramming mass, V-belts, even bearings & bearing rings to a lower extent deserve a higher multiple because of predictability of cashflows.

Note that these questions do not need to be answered once & forgotten. The answers to these questions for industries & for companies are dynamic & evolve over time. Eg: pre-covid e-com retail was a secular trend in India, US, UK. Covid made it megatrend because of the demand for e-retail skyrocketing due to closure of physical retail. However, the 2nd level thinking was that opening up will make same tailwind into a headwind & turn e-retail from a megatrend to a nothing burger for a couple of years at least. This was right time to sell vaibhav global if an investor were answering these questions internally & looking out for datapoints which can help answer the questions with data (US UK declare retail sales breakup monthly). Biggest learning for me: Be prepared with questions al the time, know what data to look at to answer the questions.

is the demand for this product or service part of a value migration?: IT infra is migrating from on-prem to cloud. From SAP to oracle. SAP-onprem to Oracle-cloud is a secular megatrend confirmed by wonderful numbers from oracle even in Q3 (where is the recession?). Demand for shivalik shunts is part of a secular value migration from ICE to EV. Demand for Pix V-belts is part of secular value migration from Chains to Belts. Demand for NIIT CLG services is a secular megatrend of L&D outsourcing. As raamdeo agrawal sir says: value is always migrating from A to B. We need to find which co is helping migrate value to B & latch on to them. In music streaming, value is migrating from downloading from pirated websites & physical CDs to streaming. Even as of today, there are 900M mobile phone users but only 300-400M music streamers.

Supply side

An Analysis of the supply side tells us about the probability of success of the co we want to bet on.

While the demand side analysis is for industry as a whole (if co makes many different products WE MUST analyze each distinct product or service individually as an industry), supply side analysis is part industry part company focussed.

How many cos can produce a good or service to meet the user’s demand for the goods or services? How is this likely to evolve in the future? Are there any barriers to entry? Any barriers to scale? Any durable competitive advantages for any of the cos?

In other words we are analyzing how concentrated the profit pool is & is likely to remain in the future. Barrier to entry in MCU is very low, barrier to entry in shunts is very high. Understanding this forms the backbone of understanding the value chain for the EV industry. There are probably 1000 steel producers in India. Steel is a true commodity. How many cos produce V-belts? How many sell it in US from India? Why is a new entrant likely to fail? An analysis would reveal that V-belts are sold under brand by some cos & the brand itself acts as a switching cost in the customer’s minds. The large number of SKUs & tooling needed act as an entry & scaling barrier. Diagnostics has low entry barriers. with 1cr capital anyone can set up a shop. How easy is it to scale though to 10 labs or 100 labs? Not very easy. Barriers to entry are low. But barriers to scale are high. How many nation wide cos have successfully scaled in B2G diagnostics while keeping their receivables in check? Answer is 1. That, is a concentrated profit pool. When it comes to shunts, the supply side is actually shrinking, Redbourn engineering has gone bust. In india, for smart meters, 3 cos won shunt contract: Redbourn, isabelle, shivalik. Shivalik was only indian co. Redbourn went bust. What did that do to the profit pool? Supply side shrinking is one of best mental models one can apply to find good opportunities IMO.

How rapidly is the supply growing?: I like the MDF industry. I like rushil decor. However, the supply is growing too fast here. Demand is growing at 15% but so is supply. + the threat of cheap imports which has happened in past & likely to repeat once US demand goes down & freight rates go down can lead to supply glut. Through this Q, the investor is trying to monitor fro supply glut. Semiconductor industry is cyclical. it takes 4-5 years to set up new fabs. But what do you think will happen when all fabs come online together? How fast is supply growing has to be seen in conjunction to how fast demand is growing. supply growth outpacing demand growth is a recipe for disaster. All auto ancs see EV migration. All of them want to set up MCU, BMS units. There are literally no entry barriers. All of them are doing JVs with some co or another. This is why i am keeping away from sterling tools despite the high growth which MCU unit can afford them. Too hard to predict the end state. Who will win? There is no good answer i have found for what barriers to entry or scale are here. In fact what i have found is that most auto Ancs are setting up MCU & BMS units. What will this do for shivalik who is sole producer of BMS/Auto grade shunts in india? Your imagination is as good as mine.

Is the supply cyclical or seasonal or structural or shallow cyclical? Does supply require large capexes ? That would make supply cyclical. If capexe are small & modular, then supply would be secular. Secular supply is better imo because it is easier to track. Otherwise we have to get into who is doing capex when & when it is likely to ramp up. Semicon fabs are one clear area of cyclical supply. Same for Steel (setting up EAF takes 2-4 years). Services co can create supply on short notice by hiring more IT engineers. Nice. Their pace of hiring & growth rate of hiring gives us all data we need to estimate supply.

is the co we want to own gaining or losing market share? : The litmus test of competitive advantages is marketshare gain. If our co is not gaining market share, then i would not want to own it. All a co has to do to gain market share is to grow faster than industry. EVs gaining market share from ICE, shivalik gaining market share from other shunt makers, that makes it an ideal investment from this POV. We want our companies to always gain or at worst maintain market share.

Some of cos I’ve been adding to in current fall

1.Financials: idfc, iifl

2.Fmig:pix,ramming mass co

3.Auto ancs: racl, shivalik

4.IT:mastek, intellect

5.FCF machines:niit,saregama

6.Health:krsnaa,laurus

7.Consumer:mirza

also studying Rolex & 1 solar co

Will try to analyze the cos i own in this framework over course of next few months.

My ideal company:

A company which gives a critical application consumable , an aspirational or need-driven product or provides cost-saving services to customers with the demand for its products/services growing fast (10% at least) & with value migrating to the industry in which the co operates (eg: ICE to EV, fossils to Solar, on-prem to cloud, unorganized & PSU lending to private banks/NBFC). Value migration forms the 1st step of industry-level market share gain. I want our co to also be gaining market share in the products & services it operates in. mastek growing faster than digitization. RACL growing faster than global auto demand, pix growing faster than gates & v-belt globally. I want my ideal company to perate in an industry with barriers to entry and/or barriers to scale. I want the supply side to ideally be reducing or at worst remaining same (demand growth should outpace supply growth).

Companies that this are perfect for me to own.

Disclaimer: Any co i mention is purely for knowledge sharing purpose , it is not an investment advice

Regarding value migration - isn’t this more of industry specific case. In some industries won’t the early phase of migration be marred by high competitive intensity, cash-burning growth and rapid changes in market share - e.g - Telecom in its early days( remember the number of players during 2G ) or currently the electric 2W space.

Isn’t an investor better of to seek consolidating industries in that case? During consolidation phase leaders would have been established, cash generation will stabilize and entry barriers will be more established.

In fact, a high revenue CAGR of recent years might itself become a trigger to attract rational\irrational competition for the industry. What do you think?

Thanks for such a detailed write up of your thoughts. I am glad I asked for it and you could pen it down for many to read and learn from them. It is good to write down our thoughts and open them for discussion with different kind of people to evolve our own thinking.

A plethora of knowledge in your write up, some points which triggered some thoughts with me wanted to share. These are just my opinions and I can be wrong in my assessments…also thoughts keep evolving…

IMO we have tendency to sometimes under estimate while sometimes even over estimate our or others hard work. We must appreciate all hard work, intelligence however the biggest virtue is one’s attitude. Once a CFO of a leading Business group in India told me this - The biggest learning he got during his entire tenure is to be “Humble”. That was the take away for him close to the end of a stunning career!

So coming to Markets, Markets are already efficient even without any of the hard working investors. We/They exist because of the market and not vice-versa. The real constituent of the market is the underlying investible businesses that exist there. It is they, who ultimately make the market efficient. It is their consistent results with time, turnarounds, subsequent cashflows or bankruptcy, business improvements/deterioration - which sooner or later would be visible to every investor and the Market would bring the value to justice as per the “doings of the company” and not the “doings of the hard working investors”

Of course hard work of the investors is paid of handsomely and I have great respect for that, however they form only a part of the market and do not make the market (efficient).

IMO - The act of underlying business performance being more visible, consistent (consistently better or worse) makes the market more efficient. Sooner or later the real picture always comes to surface in this Market and that’s what makes it efficient.

That’s good to know. How did you get chance to meet many of them?

Beautiful quote and even more beautiful modification!

I share my learnings widely on twitter. Some such well networked investors reach out to me to discuss with them.

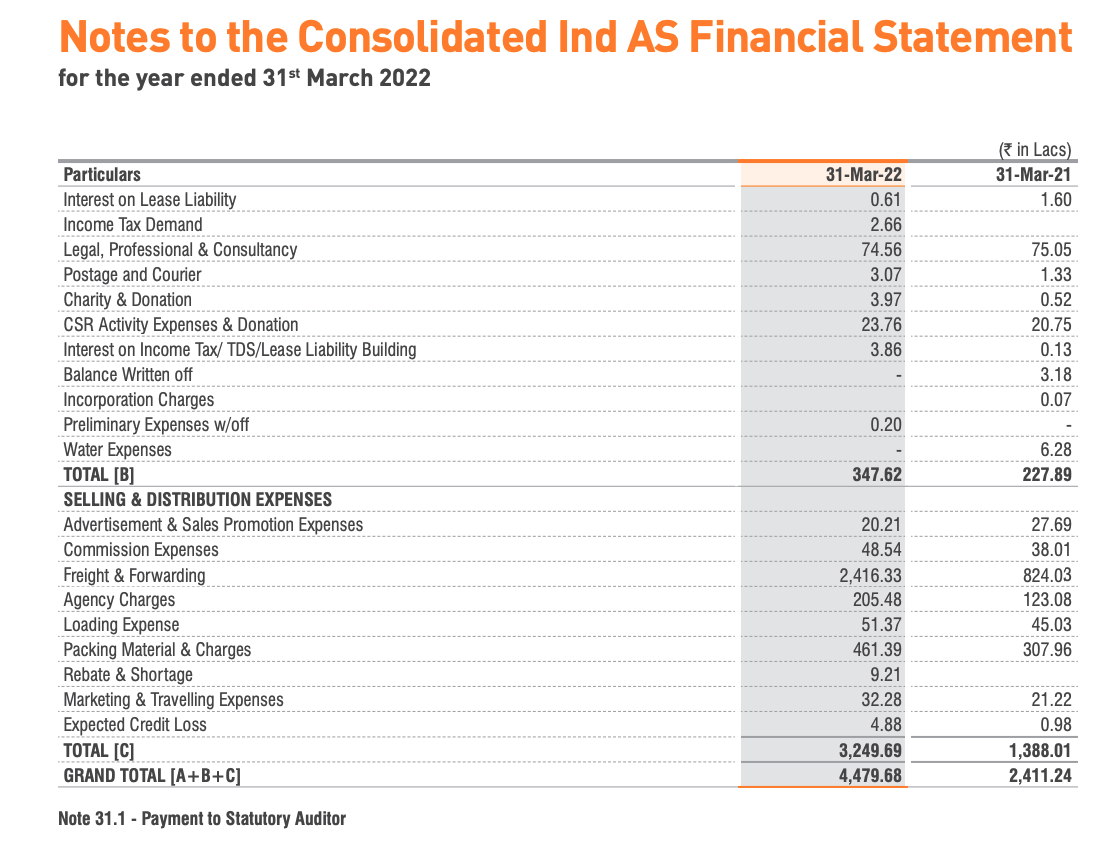

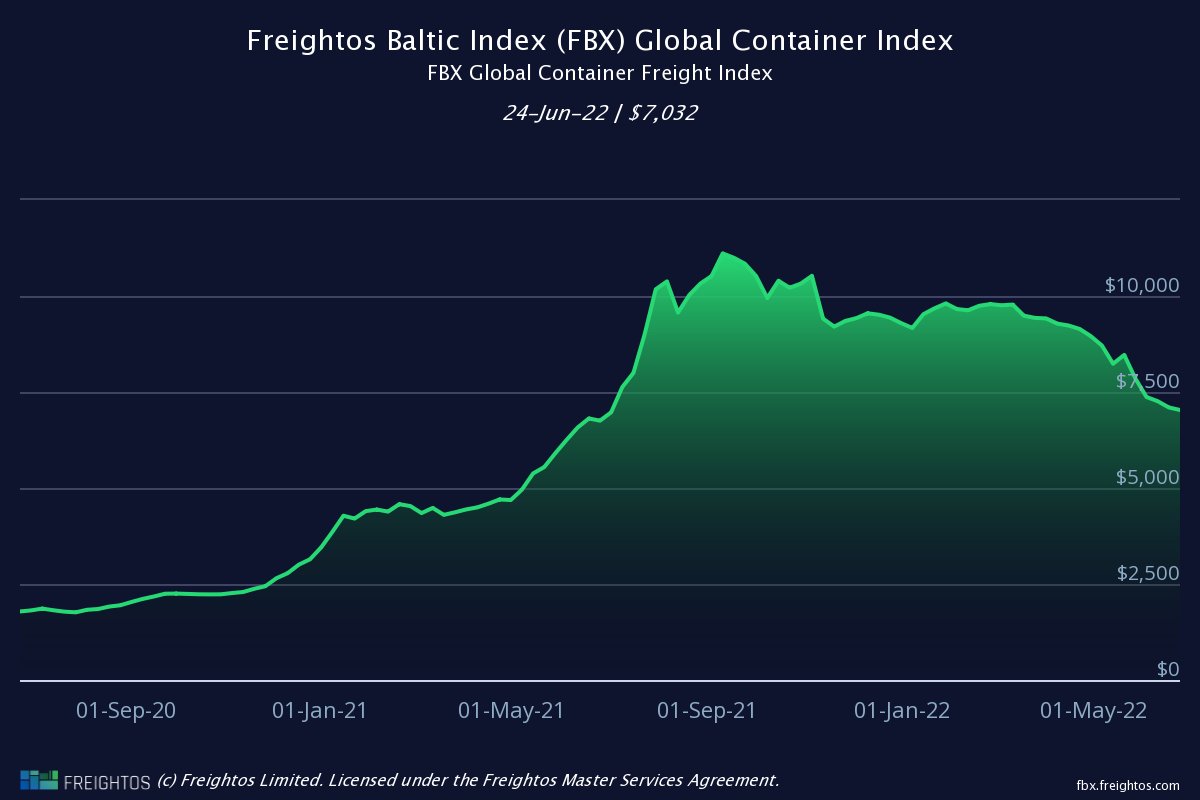

Just wanted to add that this understanding of raghav has proven to be correct, FY22 annual report just came out today. Look at other expenses notes to consolidated statement (note 31)

The freight expenses are up 3x from 8cr to 24cr. I believe this has artificially deflated true profitability of the business which could come out more prominently in FY23 as freight rates normalize (not to pre-covid but compared to FY22 rates). True P/E for raghav could be closer to 18-20 rather than 28-30. We will learn with time how accurate my estimates are.