Thank you for the explanation Ashwin!

hello sahil, hope do you well , my question arises , what iss the thought process in investing in RPPL, in my opinion SH KELKAR, Orienatal aromatics would play better at least they had barrier to entry, please give your opinion on this also, thanks in advance.

1 Like

slow growth

overvalued

Thus, these 2 are ruled out.

How do you quantify barriers to entry? I want to know your thought process first before i answer with what i think.

1 Like

my two cents as new investor, in F&F(flavoursand fragrence) less than 5% cost for smell and taste only 5-6 international players, 80% flavour we taste comes from what we smell and 75%emotion triggrer by smells, e.g if love britannia butterscotch biscuit or any other and in fragrence like if you choose fogg perfumes , once you become habitual , its very diificult to replace brand and flavours, just because of consumer emotional attachment, hope it work, thnks in advance .

2 Likes

I will now take your answer, and create an equivalent one for rajshree substituting as few characters as I can:

packaging costs less than 5% cost for fmcg items. Only few large players in India. No competition with China since most companies want to source locally, logistics does not work in terms of importing from china. The packaging of a fmcg item is important to ensure it remains hygenic, has the appropriate shelf life and that it does not get contaminated. Also the way the brand is displayed the colors which come on the packaging, make the customer habitual , its very diificult to replace brand and colors, just because of consumer stickiness.

How does that sound for rajshree?

1 Like

hi.

i have this in my portfolio….

my reasons for buying…

- very concentrated profit pool (OAL is supposed to be 6th largest in the world…virtually no peer in India)

- Probably the only one in aroma chemicles which has a USFDA approved plant

- growth projections and margin expansion both indicated by management in concalls…(management is capable and known to walk the talk IMO)

- most importantly…its developing the moat switching cost…once their R&D done aroma chemicles enter the process chain of an FMCG product…it wont be changed soon…

- Significant Capex Plans

i would love ur comments on this one…

i am actually looking for a counterview…

3 Likes

Remember…

“Human beings are creatures of habit…”

A person who develops a certain taste or aroma wouldnt like change in it…and a company selling that product would never like a change…in either the flavour or the aroma of the product…

and that is where i feel lies the moat…

1 Like

Concentration of profit pool only impacts predictability of earnings, that too to some extent.

Largest driver of returns in India is growth. Anything else doesnt matter as much if growth is low.

Also, If buying price or entry valuations are high margin of safety is low.

Sorry i cant provide one because i have not studied the co. I can only provide generic gyaan

1 Like

ya so my margin of safety is probably high…

coz i am invested from much lower levels…

and as for growth…the company’s revenue has been growing much faster than industry average…

Do read more into this one…if u get time…

I would love ur deeper view

1 Like

Hi @sahil_vi

I particularly appreciate your ability to say no to even study stocks based on some specific parameter, love the clarity of thought. I find it hard to give stories a miss without at least spending some time on going through details - I tend to give a lot of benefit of doubt to “things that can go wrong”, which I think is a weakness as an investor, and one that I am trying to work on.

Curious to know your conclusions on an investment decision on Strides. Seems to me from your posts on the Strides thread that it ticks most boxes - growth, optionalities, management. But from a margin of safety point of view, how does one build in the possibility of potential adverse US FDA action? Also wondering if you have studied Healthcare Global (Aditya Khemka’s largest bet).

P.S. I have been adding small quantities of Strides below 800 and it is now nearly 3% of my PF.

3 Likes

It is okay for a growing infra company to have a negative FCF. The reason is typically for a medium-sized project, if a company executes well, it will complete the project in 2-3 years. The money that gets struck will depend on the type of model they opt for like BOT, HAM, EPC etc., Besides, sometimes the projects get delayed and this means higher inventory, no cash flows until the project is complete. In the meantime, if the company wins more projects, they need more capital to grow and so higher working capital. So FCF will be lower. Most of the time the generated cash flow is not even sufficient to fund its own growth, that is why they take loans or raise money through equity. Infra companies once in a while monetize the completed projects in order to fund future growth.

Please bear in mind that this is for the companies which are growing fast.

So, it is not necessarily a red flag for infra companies to have negative fcf. But try to understand why FCF is negative through concalls and annual reports. Also try to look at the common sizing of balance sheet, especially how much of the past receivables are recovered in percentage terms. This will give a better idea.

Listen to the recent GR infra IPO call. You will have a better understanding of the cash flows and working capital of a fast growing infra company.

I am also a novice in analyzing infra companies, other experienced guys like @ashkrithik can add on.

2 Likes

Alok Jain Mi25 seems only small cap momentum and no element of fundamental. Intel sense seems to give some weightage to fundamental. But someone who claims to follow copy book dual momentum theory is capital minds Deepak Shenoy. Good part about AB sir’s strategy is there is more details available unlike others.

Can you share your views and feedback on Marketsmojo Model Portfolio. Algorithm driven techno Funda portfolio.

1 Like

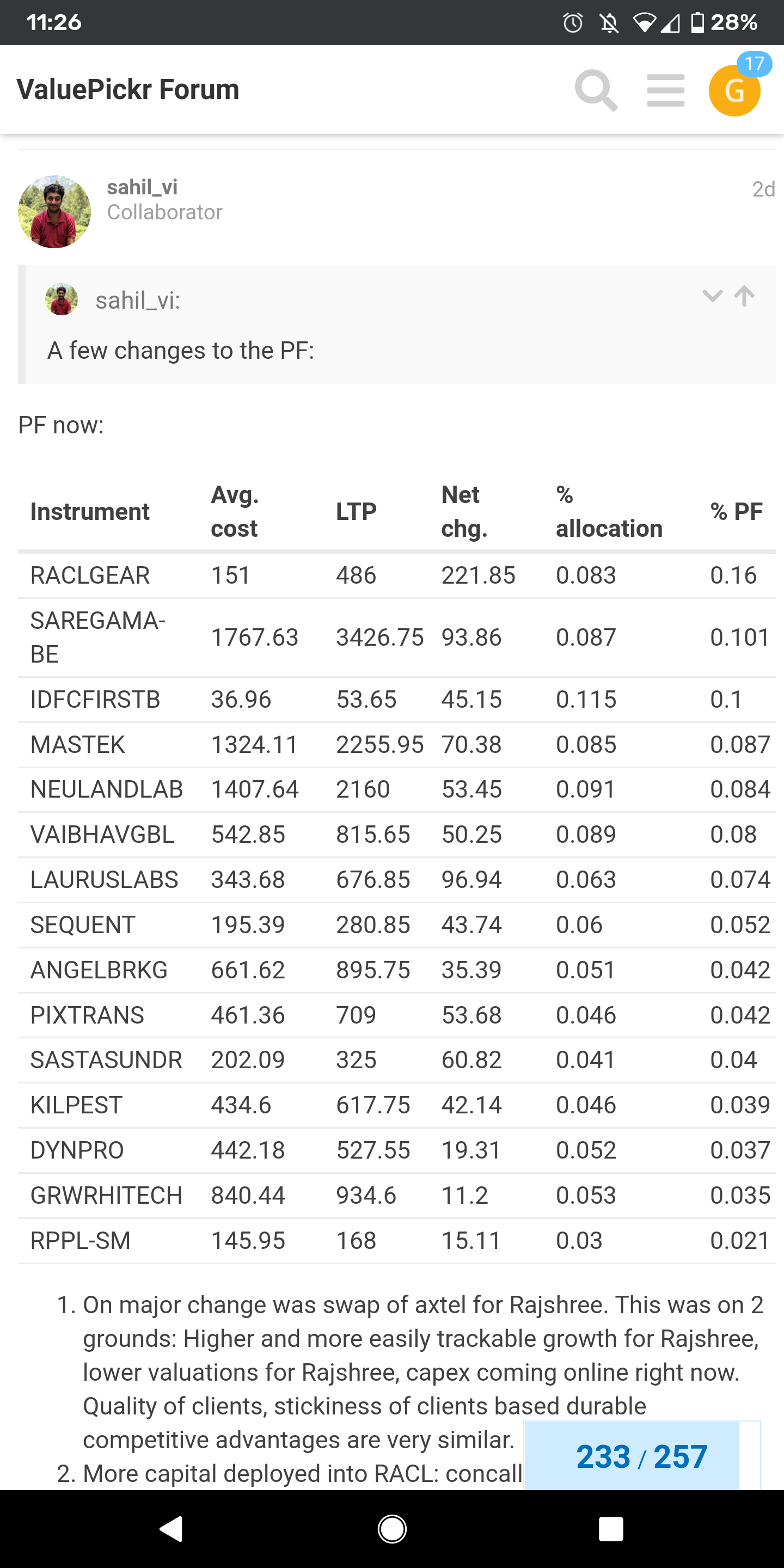

Hi Sahil … Quick Question. Within 8 months you have rejiged your entirely portfolio except couple of stocks. Is it due to bull market momentum or degree of conviction higher in these stocks than previous one and do you see holding these stocks now for long term? What I am trying to learn/ understand how do you decide to replace the existing set of stocks with new one?

5 Likes

Gaurav, have you read the entire thread (each post)? My sense is that either you haven’t or if yiu have, not properly. Otherwise you would find answers to your question already.

Will summarise:

- In the very beginning I had mentioned that I expect my pf to have high churn. Why is that? Because as a learner as someone who has only studied say 5% of all listed cos and then selected 15 how can I ever claim that my set of 15 cos are the best for my pf ? Unless I have studied 4000 companies I can’t claim that my pf will have low churn. Because as I learn more I realize that this new company is better quality, higher growth, lower valuations. Then it would be disservice to my pf to stick to an inferior investment (a superior company can be an inferior investment) knowing fully well I have found a better one. I have never claimed that my pf will have low churn : it won’t until my knowledge grows exponentially (which it has in the last 1 year mind you).

- I have covered in glorious detail how I decide to sell a co in a previous post. Please find it.

- I will summarise my methodology quickly here : for each pf co as well as candididates I read as much as I can on public info and construct a bull and bear case of earnings growth projections and the exit valuations projection. Then I apply my human judgement to decide whether A can replace B keeping in mind a fee directives:

- A can replace B if the cagr growth I expect from A in the future (from the time of evaluation) is much higher (say 10-15% higher)

- I have to ensure that pf always has high diversity in terms of lack of correlation of cash flows generated by businesses. If you observe most pf have become spec chem + pharma heavy now and imo this is a big risk since any adverse sector specific event impacts everyone a lot.

- If you see the oldest changes, most replacements were due to finding higher quality companies or higher diversification (uncorrelated cash flows) per unit change. Changes more recent in time are mostly due to co’s valuations running far ahead of growth expectations. A co with 15% topline growth and 20% bottomline growth can’t trade at 75-80 pe AND generate higher than 20% returns it’s as simple as that.

- As my knowledge keeps compounding (I place very high value to attending sector webinars and reading sector reports) I am able to understand myself better as an investor. For example I am simply not able to own a co which produces commodity where prices have gone up due to demand supply mismatch. I have also found that my peace of mind is directly proportional to the perceived durable competitive advantages the co has. Or the predictability of cash flows. As this compounding continues I expect the churn per unit time to be lower. As an example in the initial parts I used to own direct infra plays. I am very very unlikely to repeat that now. I understand the sector much better. I understand my apprehension about that sector much better now.

- Warren Buffett owned 400 stocks during 1950-1960 his highest return decade. For an investor with low capital managing their own money, churn can be okay depending on WHY one is doing churn. MOST cos I enter do not have momentum when I enter them they’re beaten down and unloved. Eventually mr market starts appreciating them (either correctly or due to overall bull market) and valuations run ahead of themselves my future return expectations go down and I have to sell in order to ensure that my future returns meet my own criteria.

- Another factor which I expect will drive lower churn in future is the bull market itself. Slowly over the last 1 year every damn sector has starred participating into the bull market. There were areas of opportunity and unloved sectors some time ago. For example recently microcaps have started moving very fast for no good reason. This just shows the broadening of the bull market and also the reduction in the opportunity pool. My probability of finding a co which does better than current pf cos keeps going down. In a roaring bull market when something is cheap we need to start by understanding why it is cheap and why we are correct and not the broader market. Efficient market hypothesis is incorrect that does not mean market is never efficient.

Sorry, No. I have not studied it.

15 Likes

@sahil_vi : As far I could understand, you have options hedge against drawdown risk. You called it kind of insurance. Do you have any other plan to mitigate deep drawdowns like Stop loss, trailing stop loss, Cash , liquidbees etc .

1 Like

No. Holding some little cash from incremental salary. Will deploy basis q1 results.

Thanks for detailed Response Here!

1 Like

Hello Sahil Bhai,

Only if you get some time to spare ,will request your feedback on below 2 companies.

I am invested in both of them and currently in SIP mode.

- NDR Auto(Under Valued) (Solid customers with very strong balance sheet and cash on hand)

- Gufic Bio(Fairly valued or over valued)(Story is developing and they are creating niche for them selves)(Please check their latest concall to headstart with)

Regards,

Ankit

1 Like

Counterview is look at the impact of change in prices of raw material on its EBITDA margins…just check in last quarter how margins suddenly fallen from around 28% levels to 15% around…so if raw material prices can propel its margins…then it can also impact in negative way…so there is some element of commodity nature… However definitely they r increasing speciality portion…but its definitely a risk…

1 Like

Hi @sahil_vi

Have been evaluating IDFC First Bank for a fresh entry. I’m fairly convinced about the rerating triggers, but have been grappling with the question of IDFC First Bank vs IDFC Ltd. I found the following post from you on the thread:

“I will still stay away from it because imo it is important to not get greedy in a bull market. That additional 50-60% return comes at the cost of some probability of the reverse merger failing (however small it is). Not worth disturbing the compounding story, incurring ltcg and stcg and then the uncertainty of regulatory landscape.”

Since you already have a position in IDFC First and you don’t want to disturb compounding, you are not considering switching to IDFC Ltd, which makes sense. Ofcourse the other possibilities around failing demerger etc hold as well. But from a fresh investment point of view, my sense is that IDFC Ltd offers better risk reward that IDFC First Bank - possible optionalities for more upside with equal potential downside?

Would love to know your views on this.

1 Like