Sagar Cement (SC) is likely to be one of the key beneficiaries of the huge development in Andhra and Telengana in the next few years.

Demand Scenario

Amaravati, is planned over 217 sqkm and would require an investment of 4 lakh crores (ref: Big plans for new capital - The Hindu). Telangana already has over 24,000 cr of infrastructure projects under construction. The govt has cleared lift irrigation projects worth 35,000 cr.

New high-speed rail line announced between Amaravati and Bengaluru

New stable governments in TN & Kerala

Huge investments planned in infrastructure projects like the proposed East Coast Economic Corridor, Dedicated Freight Corridor, Diamond Quadrilateral High Speed Rail and National Waterways.

Decision to use cement instead of bitumen for a large number of big road projects

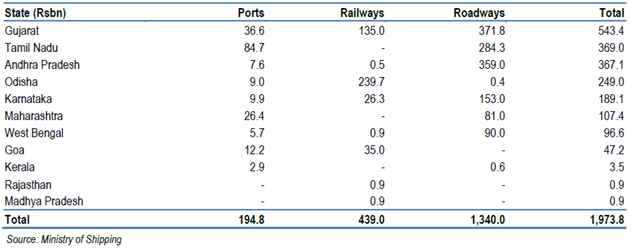

Investment Plan of the Govt related to infrastructure:

Supply Scenario

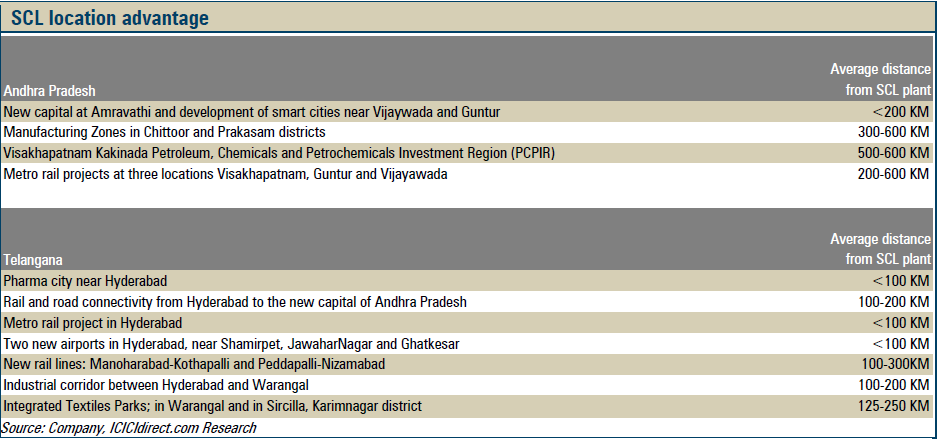

Capacity at strategic locations:

3 MTPA of cement and 2.1 MTPA of clinker at Nalgonda, Andhra PradeshAcquired BMM Cements in Sep 2014 with 1 MT cement and 25MW captive power plant at Anantpur, AP at an EV/ton valuation of $87/ton

Sales is well spread geographically, tough majority comes from AP & Telangana.

BMM Cements had 3000 acres of land. In Dec 2015, BMM AP govt approved a 20 year mining lease for 1200 acres containing limestone reserves of 155 million tons. This provides raw material guarantee.

The company has setup rail siding to reduce transport cost. 20% of transport to move to rail thereby increasing operating margins.

The current capacity utilization is at 56% leaving ample scope for increasing utilization. BMM Cements also had a captive power plant of 25MW capacity. Access to captive power will also reduce operating cost. With the completion of the acquisition, SC will consolidate results from Q1FY17.

Financials:

The stock is available at a market cap of around 1200 cr at a PE of 23. The current replacement cost of cement is about 800 cr/mtpa

Risks

Aggregate demand does not pick up due to delay in infrastructure spending or lack of turnaround in housing sector

Adverse Govt policy related to price ,specially for low cost housing projects

Spike in input costs

DISCLOSURE: I hold the stock and other cement stocks.

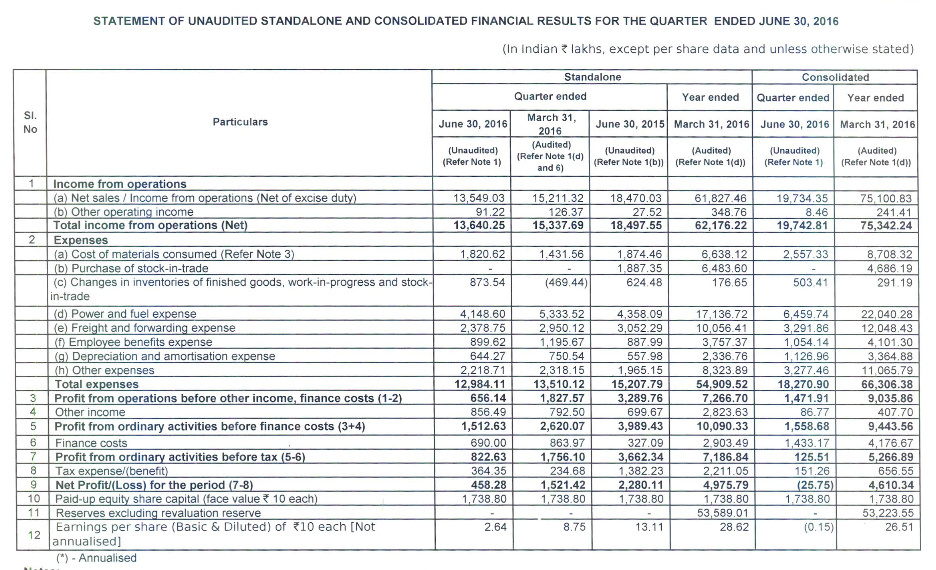

The Company consolidated net Income from operations increased to Rs. 197.43 crore Q1FY17 from Rs. 184.98 crore in Q1FY16. The Company earned net Income of Rs 136.40 crore from Sagar Cement and Rs 61.93 crore from BMM. Top line expansion was primarily achieved on the back of strong volume growth, which helped partially negate the impact of lower realisations.

EBITDA Margins decreased to 13% from 21%. Thus, EBITDA decreased to Rs. 25.98 crore as compared to Rs.38.48 crore in Q1FY16. The Company suffered net loss of Rs 0.26 crore in Q1FY17 compared to net profit of Rs 22.80 crore corresponding previous period.

The Company board has accorded its ‘in principle’ approval for the acquisition of the entire assets in the grinding unit of 181,500 tons per annum capacity in Bayyavaram, Vizag district, Andhra Pradesh, owned by M/s Toshali Cements, Hyderabad, at a cost of around Rs 60 crore (including transaction cost. Post acquisition, the company proposes to increase the capacity of the said unit to 300,000 tons per annum by optimizing the equipment already available with the company by infusion of funds to the extent of around Rs 6 crore. The acquisition will enable the company to save its logistic cost and to introduce slag cement to cater markets in Visakhapatnam, Viziangaram, Srikakulam and parts of Orissa. The transaction is expected to be completed by September 2016, subject to regulatory approvals as may be required by the company to commence its grinding operations in the said unit.

The Company cement pricing and volume were subdued in the target area of operation. Thus, realisations were also considerably lower;

The demand as well as prices in the western region remained soft in Q1FY17 as the region suffered the most from water scarcity. Prices in the southern region remained ranged, owing to acute softening of prices in Andhra Pradesh & Telangana. Infiltration from West market owing to price variance resulted in compression of demand.

The company has produced 473902 tonne of clinker and 580419 tonne of cement for Q1FY17. Meanwhile, cement sales volume rose 22.6% to 575 mt worth of Rs 197.34 crore (up 6.84% YoY). The cement net realization declined 12.85% to Rs 3431 per tonne.

The company average fuel cost per tonne decreased in Q1FY17, (down 2.6% to Rs 779 per tonne for Sagar Cement and Rs 899 per tonne for BMM) due to drop in price of imported coal and change in coal mix resulted in a decrease in average fuel cost per tonne. Domestic: International coal mix was 0.4:96. The company average coal cost stood at Rs 4330 per tonne for Indian coal and Rs 5485 per tonne for imported coal, as compared Rs 4964 per tonne for Indian coal and Rs 5361 per tonne for imported coal in the corresponding quarter in previous year.

During Q1FY17, the plant operated at reasonable utilization levels producing 473902 tonnes of clinker and 580419 tonnes of cement. **The cement plant utilization level stood at 58.04%. **

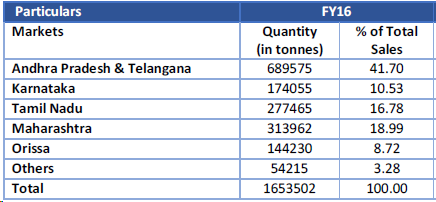

Approximately 55% of cement dispatched to various markets outside Andhra Pradesh & Telangana such as Maharashtra (15%), Karnataka (14%), Tamil Nadu (16%), Orissa (6%) and others (3%).

The company consolidated cement sales volume stood at 575156 tonne for Q1FY17. On market basis- nearly 262583 tonne cement (45.6% of total sales) came from Andhra Pradesh & Telangana, 81636 tonne cement (14.2% of total sales) from Karnataka, 92242 tonne cement (16% of total sales) from Tamil Nadu, 89165 tonne cement (15.5% of total sales) from Maharashtra, and 33493 tonne cement (5.8% of total sales) from Orissa. The company has dispatched 572527 tonne of cement by road transport and 5310 tonne from rake as compared 478345 tonne by road corresponding previous quarter.

The consolidated gross debt as on 30th June 2016 stood at Rs. 439.60 crore out of which Rs. 334.52 crore is long term debt with the remaining constituting working capital. Cash & Bank Balances held by the Company at the Balance Sheet date was Rs. 5.54 crore. The Net Worth of the Company as on 30th June 2016was Rs. 549.36 crore. Investments stood at Rs. 78.21 crore. Debt: Equity Ratio as on 30th June 2016 stood at 0.61:1.

The Company guides pick up in Government spending towards infrastructure, good monsoons and delay in new capacity addition to help drive growth forward.

The Company expects the business prospects look promising in the long term, though operating environment at present continues to witness low off-take and weaker realisations. Synergy benefits following BMM acquisition are gradually starting to kick-in as reflected by lower freight cost for the quarter and hopeful that the same would continue to contribute positively to the business going forward. Further, commissioning of railway siding operations should also help the company to increase cost savings. Lastly, acquisition of the grinding unit should also help grow and better service target markets. Going ahead, persistent Government’s actions towards strengthening infrastructure, pick up in rural demand and good monsoons should aid in driving demand and profitability for the business.

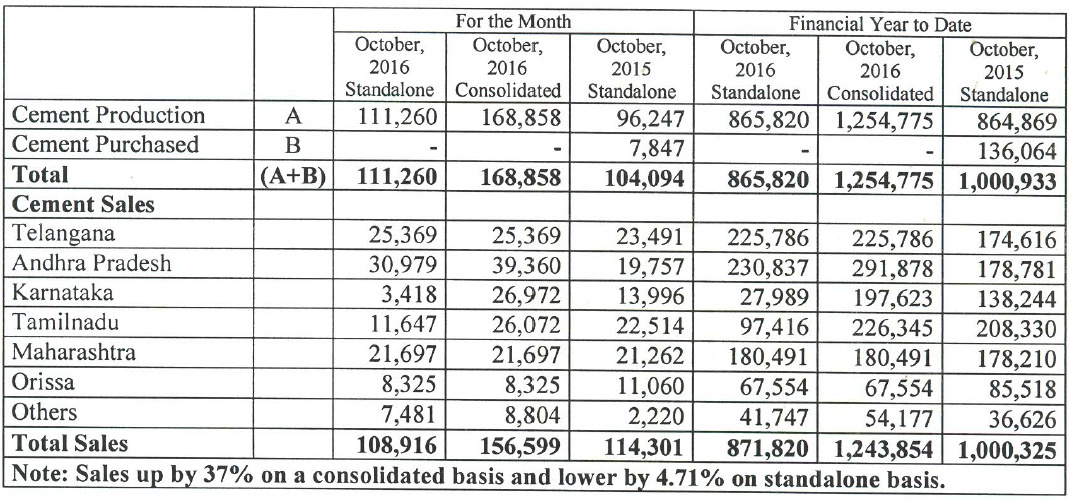

One of the most important monitorables in cement businesses is their despatches. It helps keep track of how a company is doing. Keeping tabs on companies across regions provides a good understanding of production & sales.

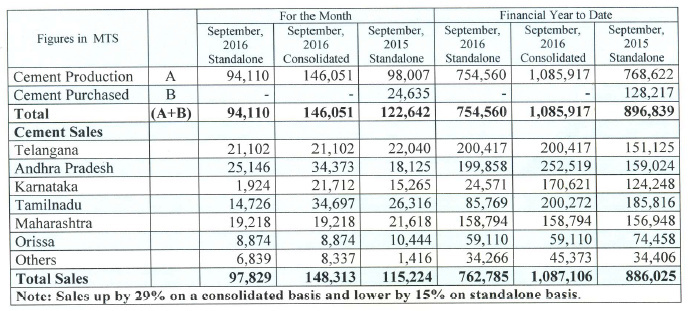

Good to see some moderate pickup in all regions except Maharashtra & Orissa.

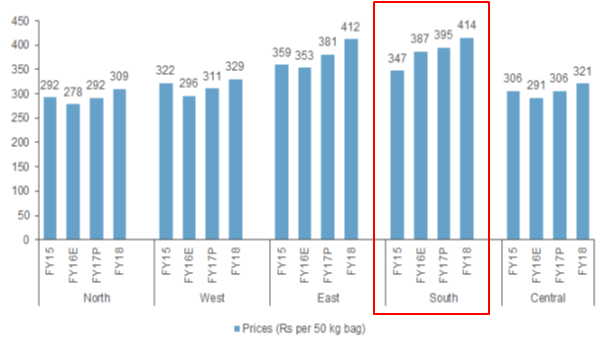

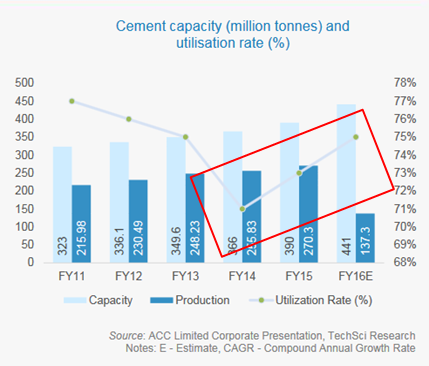

Below a slightly dated report suggests that demand is quite sluggish in southern regoin resulting in utlization and pricing power issues. And given the inevitable gap between plan and reality and the fact that stock trades at high PE, is it a worthwhile bet with margin of safety?

Sagar Cement Ltd will be investing about ₹145 crore in its expansion. The Hyderabad-based company is looking at around ₹100 crore capex this year and during next fiscal it could be around ₹45 crore.“This will include approximately ₹66 crore being incurred for acquisition and other associated costs of a 1,81,500 tonne grinding unit owned by Toshali Cements Private Ltd which is located in Bayyavaram, Vizag district of Andhra Pradesh,’’ Sreekanth Reddy, Executive Director, Sagar Cement told BusinessLine on Wednesday. “This acquisition will bring down logistics cost and facilitate Sagar to introduce slag cement in parts of Andhra Pradesh and Odisha,’’ he said.Post acquisition, Sagar proposes to scale up capacity to 3,00,00 tonnes per annum with an additional capital expenditure. The funding for acquisition will be through internal accrual of ₹20-25 crore and the rest will be debt. Investments are also being made into a waste heat recovery project.In August 2015, Sagar acquired BMM Cements Ltd with one million tonne capacity and 25 MW power

plant in Gudipadu, Anatapur district of AP.

Gross debt

According to Reddy, synergy benefits following BMM acquisition were gradually starting to kick in as reflected by lower freight cost for the first quarter and the same will continue to contribute ‘positively’ to the business going forward.The gross debt of the firm on a standalone basis stood at ₹195 crore out of which ₹118 crore is long term debt and the remaining constituted the working capital. On a consolidated basis, gross debt was ₹440 crore, out of which ₹335 crore is the long term. The debt-to-equity ratio stands at 0.61:1.As on date, Sagar Group’s clinker capacity is at 3 million tonnes, while cement capacity is 4 million tonnes.

In Andhra Pradesh and Telangana, cement prices have risen by Rs 30-40 per bag in last two days. This is clear indicator of rise in demand for cement in these regions.

Is this information can be downloaded online? Is there any charge associated for accessing the same? I’m assuming that this is a company specific report.

Thanks Abhishek Da, I can download the same from BSE. But I guess sharing of this info is not mandatory? Because I can’t find it for JK Lakshmi cement from BSE site. correct me if I’m wrong.

Will see you tomorrow @smart street Cafe and if possible discuss about cement sector basics if time permits

Below is the verbatim transcript of Pankaj Pandey’s interview to Latha Venkatesh and Anuj Singhal on CNBC-TV18.

Anuj: One of the sectors of the day is midcap cement and you have one the stocks which you like here, Sagar Cement. Tell us why do you like this stock and what is your price target?

A: We like Sagar Cement and we have a target price of Rs 975 on the stock. It is a south based cement player and southern as a region has been doing quite well from a cement perspective. This company specifically if you look at from 2008 till now, they have ramped up their capacity seven times from a smaller base of about 0.6 million tonne to about 4 million tonne odd. What we expect is that the company will further ramp up its capacity to about 6 million tonne.

Company has acquired BMM Cement in 2015 and the company has been able to turnaround this company and as a result of that what we have seen is that the capacity utilisations have gone up to about 60 percent as seen in the last quarter. Like other south based players, we expect this company to deliver EBITDA per tonne of over 900 and we expect a topline growth of 23 percent and bottomline growth of over 55 percent. So, profit expectation for FY18 is about Rs 110 crore.

We expect return ratios to double to about 14-18 percent and this stock is available at 65 EV per tonne and we have valued it at about Rs 80 EV per tonne which is what we have given to other players. So, within south based players, I think this company is rightly poised to gain further.

• Demand during the quarter remained a bit soft partially on account of seasonal weakness but also on account of lower government offtake.

• The pricing environment remained a bit volatile with prices in west languishing at lower levels for major part of the quarter picked up during latter part of the period.

• In South market, prices remained more or less steady during the quarter.

• Demand situation is expected to improve following the revival in the rural region after normal monsoon and the anticipated pickup in the government spending on infrastructure, individual and low-cost housing.

• SCL is setting up a coal based captive power plant at our Mattampally unit besides approving the expansion of our just acquired grinding unit at Bayyavaram in Andhra Pradesh.

• Contemplating to commence the production of slag cement from this grinding unit.

• Expect H2 to be much stronger than the H1 in terms of demand

• Q3 in Tamil Nadu would be bad as that is when the monsoon will be there

• In some parts of Maharashtra like Mumbai, Pune, Solapur there has been a good price increase at end of September (Rs 50)

• SCL is planning a preferential allotment and a QIP to raise 200cr of the 250 cr required for the capex to increase capacity to 6 MTPA

• Plant acquired from Toshali cements in Vizag is likely to start production from November

Sagar Cements Ltd has informed BSE that the Board at its meeting held on November 28, 2016 inter-alia, fixed an issue price of Rs. 800/- (Rupees eight hundred only) per equity share (which includes a premium of Rs. 790/- per share) for the 6,11,986 equity shares of Rs. 10/- each of the company being issued for cash on a preferential basis, subject to receipt of further necessary approvals as may be required.

Interesting to note the confidence of the company that it is issuing preference shares at Rs 800 when CMP is 690.