Company: Safe Enterprises Retail Fixtures Ltd

Sector: Furniture, Home furnishing

Exchange: NSE SME

Basic Details

Market Cap: ₹1,000 crores

Issue Price: ₹138

Current Price: ₹215 as of 26th January 2026

Listing Date: 27th Jun 2025

Financial Highlights

FY25 Revenue: ₹138 crores

Net Profit: ₹39 crores

ROE: 77%

Debt-to-Equity: 0

Revenue Growth (3-year CAGR): Not Available

Industry Overview – Retail and Interiors

The retail industry contributes over 10% to India’s GDP and around 8% to total employment, positioning India as the world’s fifth-largest retail destination. According to Boston Consulting Group (BCG), the Indian retail market is expected to reach approximately US$ 2 trillion by 2032. Infrastructure development continues to support sector growth, with nearly 60 shopping malls covering 23.25 million sq. ft. of retail space expected to become operational during 2023–25. Growth drivers for Indian retail include favourable demographics, rising income and purchasing power, increasing brand awareness, and wider availability of consumer credit. Parallelly, India’s interior design industry is expanding rapidly, with market size estimated at US$ 27 billion in 2023 and projected to reach US$ 81 billion by 2030, implying a CAGR of ~14%. The market is dominated by commercial interiors (75%), with residential interiors accounting for the remaining 25%.

Business Overview

Safe Enterprises Retail Fixtures Limited operates in the design, manufacturing, supply, and installation of shop fittings and retail fixtures. The company provides end-to-end in-store solutions, covering conceptual design, prototyping, manufacturing, and final installation, customized to customer requirements. Its product portfolio includes modular retail fixtures such as storage racks and systems, cabinets, partition systems, digital display screens, touch-enabled monitors, display tables, glass counters, horizontal stands, and cash counters. These solutions cater to multiple retail formats including fashion and apparel, departmental stores, electronics, gifts, and novelty stores.

The company operates an Experience Centre in Cochin, Kerala, allowing customers to view and experience its technology-enabled shopfitting solutions. It also has franchisees in Navi Mumbai and Hyderabad, along with distributors in Dubai and Kansas City.

Management Quality

Promoter Holding: 70%

Promoter Background and Key Management: The company is led by a promoter-driven management team with deep industry experience. Mr. Saleem Shabbir Merchant, Chairman and Managing Director, has approximately 48 years of experience and oversees business planning and development. Mr. Mikdad Saleem Merchant, Whole-time Director and CFO, has around 13 years of experience and manages the company’s financial and secretarial functions. Mr. Huzefa Salim Merchant, Whole-time Director, has approximately 14 years of experience and is responsible for production, operations, vendor management, marketing, business development, and after-sales services, effectively performing a COO role. While the business is family-managed, scaling up operations may require the induction of professional management.

Investment Thesis[u]

Positives:[/u]

In-house product manufacturing capabilities – The operations involve metal fabrication, wood works, carpentry process, painting, powdercoating etc. for manufacturing of shop fittings and retail fixtures, ensuring quality of products.

Established relationships with customers across various geographical location - Diversified revenue from multiple geographical locations across India and a portion of revenue from outside India such as USA, UAE, Oman etc. generated around 1.31%, 0.85% and 0.97% of our revenue from operations for the respective period from export sales for the for the fiscal year ending 2025, 2024 and 2023 respectively – scope for export revenue to grow as currently it is only 1% but I don’t think that furniture and fitting as export can become big because it will be cheaper for the importers to get from there own country.

Top 10 customers contributed approximately 95.91%, 96.79% and 94.68% of the revenue from operations respectively – client concentration is a big risk for them but the tie up was with zudio they can simply take zudios name and can pitch to other possible client.

Revenue from Maharashtra – 17%, Karnataka - 11%, Telangana – 8%, UP – 8%, Gujarat – 8% total 50% from these 5 states and rest from other 20 states.

Technology and Innovation - Through its subsidiary, Safe Enterprises Retail Technologies Private Limited, the company develops and distributes modular and electrified shopfitting solutions integrated with digital technologies. This platform provides scope for future product launches, supported by existing resources, industry experience, and distribution networks.

Concerns/ Risk Factors:

Limited operating track record: The company has a short operating history as a corporate entity following its conversion from a partnership firm, which may limit assessment of historical performance and future outlook.

Leased facilities risk: Operations are conducted from leased premises, and any non-renewal or disputes related to these properties could disrupt business activities and financial performance.

Customer concentration risk: Revenues are significantly dependent on a few key customers, and loss of any major client could materially impact revenue and cash flows.

Geographic concentration risk: A large share of turnover is generated from select regions, making the business vulnerable to adverse developments in these markets.

Valuation

P/E Ratio: 18

P/B Ratio: 4.4

EV/EBITDA: 12.4

Compared to peers: There is no perfect comparable to the company as per my understanding but still a comparison with the other companies in the furniture segment is as below

Growth Catalysts

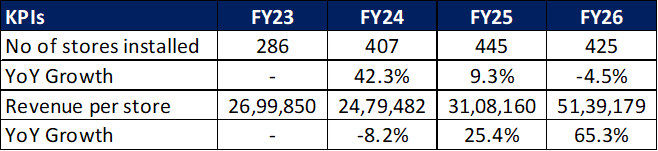

Manufacturing capacity has been expanded through a 46,505 sq. ft. extension at the Pune plant. Post-IPO, the company initiated development of an integrated Ambernath facility, which is currently under construction. To bridge interim demand, two additional units have been added in Mumbai, and Pune capacity has been doubled. This infrastructure is expected to provide sufficient headroom until the Ambernath facility becomes operational. Alongside capacity expansion, the company continues to focus on quality adherence through regular reviews and corrective measures, supporting customer retention and brand recognition.

Geographically, while products are currently marketed across more than 25 states and union territories, the company plans deeper penetration in markets such as Punjab, Rajasthan, Uttar Pradesh, Telangana, Uttarakhand, and Delhi.

Management Guidance

Management has indicated medium-term growth visibility, targeting revenue of INR 400 crore and PAT of INR 100 crore by FY28. This outlook is supported by expanded manufacturing capacity, improved execution capabilities, and sustained demand from organized retail expansion across India.

Disclosures

I currently do not hold any shares of the company but planning to add in the near time. Also, I don’t have any link to any of the promoter.

Disclaimer

SME stocks carry higher risks due to their smaller size, limited operating history, and relaxed regulatory requirements. This analysis is for educational purposes only and should not be considered as investment advice. Always conduct your own research or consult with sebi registered financial advisors before making investment decisions.

Request you guys to add something that one should consider before investing in this company and for more analysis.