@nithin_Shenoy i am considering a purchase here. Just cross checking the size of revenue from just PAP. Correct me if these are reasonable assumptions.

F25 PAP production volume 8000 tonne

FY26 PAP production volume 22000 tonne

Do anyone have idea about promoter holding in Dec2023 quarter , it shows 6% decrease , is this due to promoters selling to public or due to rights issue ?

When right issue was priced so high that the promoter only would have participated, why is there a decrease in promoter shareholding? And why the exchange wasn’t notified of the same.

Sadhana has 4 different auditors for Statutory Audit, cost audit , Secretarial Audit and internal audit what do you make out of it ?

The other expenses continue to be on the higher side, the receivables are on the higher side too and they don’t even conduct investor calls - dicier than ever

Most what i do see here is : Other than PAP sales, the dyes side of things are growing…

Its difficult to get business bifurcation however we need to connect dots by listening to other concall.

PAP will take utmost 2-3 quarter which is second half of FY 25.

However if the business is able to maintain this sales - hard to tell… I dont know how other things within this business demand are… either its for a month or say 6 month dont know.

if someone has spoken to management please share the notes

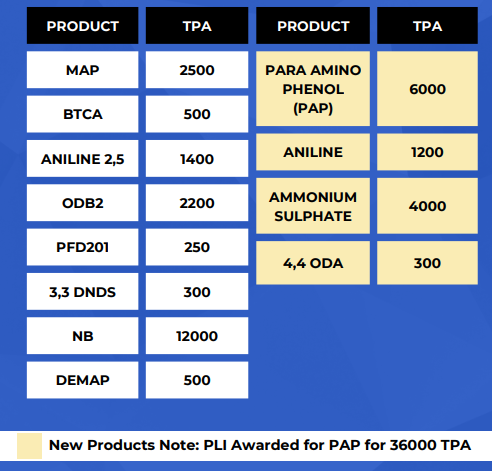

Any update on new 3000 tonnes PAP unit? In the last PPT, they have mentioned as 6000 tonnes.

If they demonstrate the success of it then they are in right direction towards 36000 tonnes of PAP.

In June’24 quarter, sales degrown. Please share your view on results. Thanks.

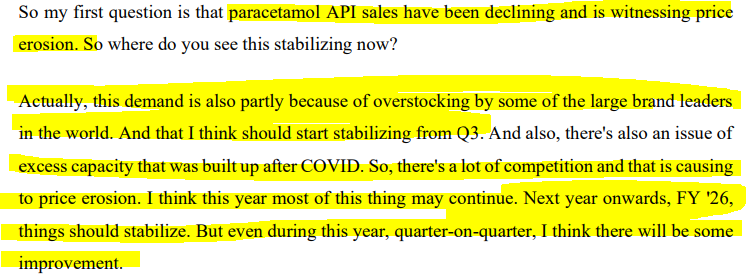

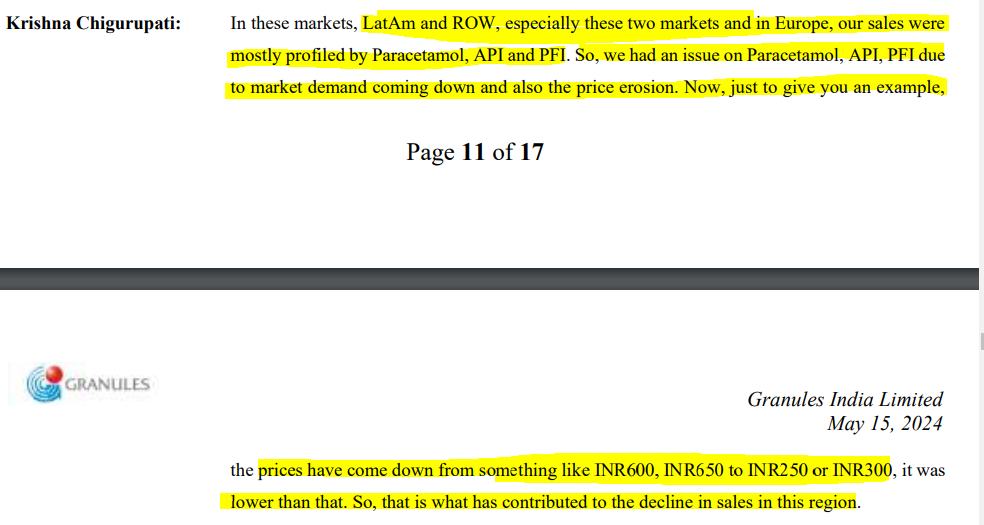

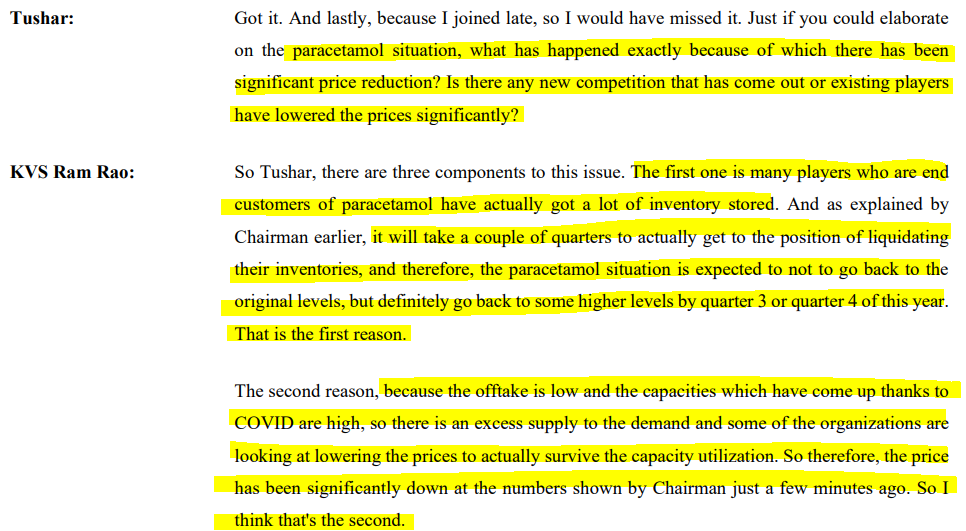

Add to the above, as per Granules July’24 concall, for Paracetamol API, its worst cycle they seen in Granules history, usually it happens once in 7-8 years. Management expectes in Q4 FY24-25 or Q1 FY25-26, Paracetamol sales expects to get back.

The market price is already at 68 and guess no one likes price dropping down too much…

But the supply side issue still persists

Granules as you can see is in back to back trouble firstly data security issue, Supply issue

, now USFDA issue

The clouds are still not yet clear… as stated above their other business are doing well that’s all…

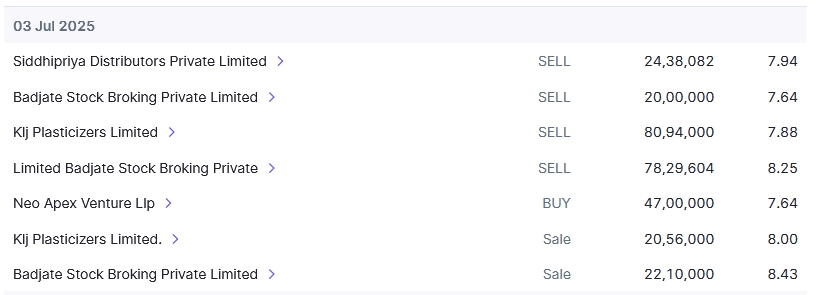

18 days of continuous selling freeze and yet there is no news which could explain this intense selling pressure.

Would be interesting to know why the price is near its book value.

Pledged shares were being offloaded is one strong theory. If fundamentals are what they actually are and Promoters ensure to infuse some more money, it should get back to saner levels. But that’s rarely the case.

I am also assuming its the pledged shares which have pulled the prices down.

Fundamentals are dicey I think as of now, but I like their technical acumen(if we are to believe their disclosures).

For ODB-2, they are the only producers of this chemical outside of China.

PAP using Nitrobenzene, they are the second only company in the world to manufacture from this method. This results in higher grade purified PAP which could be preferred in pharma industry. The residual pollution is also very less.

Historically, the share price has gone from circuit to circuit on previous occasions also.

There are some good HNIs who have invested in this company.

More than 90% crash from the high levels. Big holders are willing to sell below the book value. This is not ordinary.

More than Rs 120 cr trade receivables in March 2025 [Revenue for 2025 was Rs 166cr]. It seems that the company is facing liquidity issues.

During bad times, the numbers become questionable. Do they really have the cash they say they have? There is no way for public investors to know how bad the situation is.