Hi,

I have been in market since 1993 though started developing on portfolio since 2010. in last 8 years realized the magic of compounding. I expected markets (particularly small/mid caps) to crash in 2017 so sold several multibaggers like National Peroxide, Tata sponge, Ashok Leyland, Camline Lifescience with decent return.

My capital allocation is 50% FDs (need secured cash for kids education), 30% equity (15% MFs, 15% direct equity mostly mid/small caps), 15% real estate, 5% gold.

I am focused on building a portfolio for coming cycle where first selection gate is management quality then growth potential with focus on cash generation to be bought at decent pricing (rarely buy stocks at >15 P/E). I expect some more correction/volatility over next 6 months due to election while I am also carefully watching global macro environment. Hope to add on some value stocks over coming 6 - 12 months.

I regularly read ValuePickr to gain insight on stocks and am highly impressed by thought process of fellow boarders. I request you to analyze the current portfolio and provide feedback.

| Stock | Avg purchase price | % of PF | holding period | |

|---|---|---|---|---|

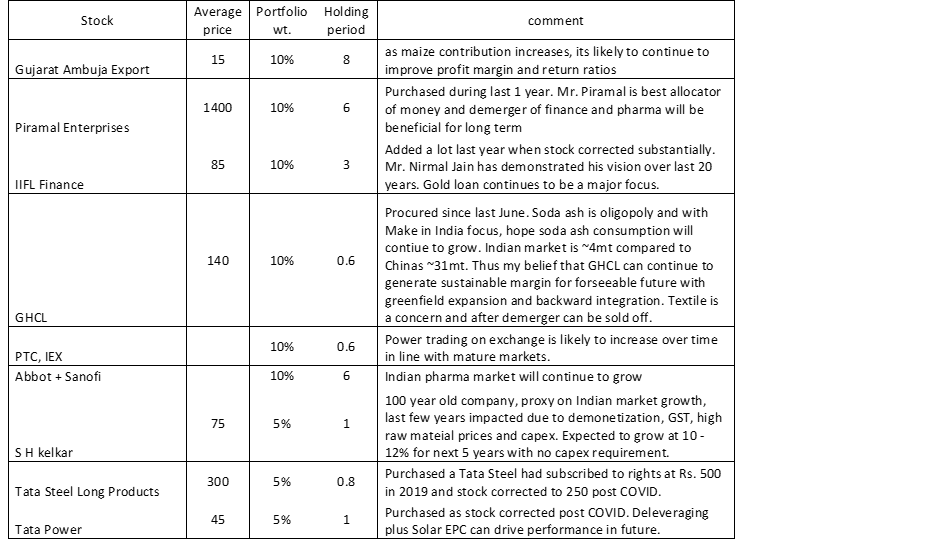

| GSPL | 125 | 10% | 5 years | Believe that gas consumption will increase in coming 5 years. GSPL is a low risk play on gas consumption in highly industrial state. Acquisition of Gujarat Gas diluted the value to a certain extent. Still holding on as PNGRB has finally increased the transmission tariff. |

| Gujarat Ambuja | 18 | 10% | 7 years | Has become a play on consumption with diversification to maize derivatives, Sorbitol, liq. Glucose, etc… Sold some shares to maintain 10% share in portfolio. |

| Piramal Ent. | 1500 | 10% | 4 years | Initiated based on pharma story and Ajay Piramal’s record. Now it’s a play on real estate and Shriram group. Holding on based on conviction that management is ethical and is best allocator of money. |

| Trident | 55 | 10% | 3 | initiated when expansion was ongoing. With capex completion operating leverage should play out. Its taking longer than expected but company is continuously reducing high cost debt and generating adequate cash flow. Entry into domestic market will be key to increase capacity utilization. Adding below 55. |

| Persistent | 550 | 10% | 1 | Entry into digital while IT infra maintenance pie should continue to deliver cash. Partnership with IBM to develop products should deliver results as they started before other players boarded "digital" bandwagon. Adding below 550. |

| Suven | 160 | 5% | 2 | Play on Mr. Jasti. Like cash generation from CRAMS. Company follows prudent policy of considering 100% R&D as expense. Any upside on new molecules will be a Diwali Bumper lottery but without it the business is valuable and will grow steadily. |

| Abbot labs | 3000 | 5% | 8 | Growth focused; introducing new products in market; removal of price caps on stents at some point will further improve the potential |

| GIC Insurance | 912 | 10% | IPO | Holding on to loss, not willing to accept mistake. Government stake/interference/regulatory hurdle does not allow management to focus on profit. |

| Capital First | 470 | 5% | 0.5 | CEO has proven track record, believe that merger with IDFC will create value. |

| MOIL | 100 | 5% | 3 | only Manganese producer in country, expansion plan set in place with capacity likely to increase by 50% in coming 2 years. It’s a commodity play still plan to hold on to it as Manganese is expected to find application in electric vehicles as well. |

| Mcleod Russle | 330 | 5% | 5 | Bought as the largest tea producer in India but tea prices are not supportive. Sold some quantity to reduce loss. Hope to sell remaining at opportunate time. |

| Lasa supergenerics | 165 | 5% | 2 | Lured by quick gain expectation, loss to retrain me that "management quality" is first criteria to be used for stock selection. |

| 10% | Tracking position in 10 - 15 stocks including PI Ind, Lupin, Indigo, Aurobindo pharma, Galaxy Surfactants, Dai Ichi, Bodal Chemicals, etc. | |||

| 100% |