If we see the Saas Play then it is good and have high margin and seeing how hiring is done there it could make some good probably unrivalled in future like when we see freshwork after a big fall is looking attractive not a recommendation but it’s major edge and only way it is beating is Indian talent pool that could be very vital for any company.

Have recently seen some new ipo namely rategain and map my India(it has saas buisness is quite smaller when compared to its overall buisness).

Rategain is a pure saas Play and can be a good contra bet and a less risky play on travel industry if we look the best bet on travel industry is either club Mahindra or Rate Gain.

These both are pretty new but looking pure buisness wise map my India looks better and is also a monopoly.

But growth opportunity and market recovery can make rate gain a good opportunity aslo but is to risky to invest right now and need to see quater results and other thing before investing.

TTBS , a part of TTML has been rechristened as a new age digital saas player. I am not sure about arrangements of ownership of TTBS by TTL parent and TTML…any insights most welcome…

Disc. Had a negligible tracking position which swelled to almost 2% of portfolio. Not a buy/sell recommendation. I myself am assessing if recent run up is justifiable but not much direct data or knowledge on the matter so far… thoughts welcome!

Tanla has been a big multibagger. Now they are going overseas. Also Subex is poised for growth… after stock reduction and becoming debt free. It can be a takeover candidate their platform business is bound to grow.

Ramesh Damani has most probably sold off rhe stake. His name doesn’t appear in the shareholders list.

Also, I had been an investor in Quick Heal, as per me, management lacs innovation and zeal. They still rely on physical distributors to push their product to the market. Receivables had been a problem. Also, IPO proceeds were on the balance sheet as FDs for years. No real attempt to grow, barring one acquisition in iran or Middle east.

From a cybersecurity domain point of view, they aren’t really a serious player though. Their core product is an antivirus and the world has moved away from antivirus to a wholistic endpoint detection and response solution for protecting end user devices.

Totally agree. This is the reason I’m not very exited about above mentioned company’s IPOs…

Including recently listed latentview and rategain…

After initial ephoria , if top line - bottom consistently don’t perform , Stock will go to long consolidation or bleed badly especially in bear market…

these happened with Justdial, infibeam , matrimony - very fancied stock during their IPOs…

Rate Gain Provided LTV / CAC in their last result presentation. Claimed it to be 11.34. They’d also provided CAC numbers in their DRHP.

However, One thing to be conscious about is there is no legal accounting formula that everyone must have to follow, some companies might exclude some costs in CAC which can show LTV to CAC optically higher than it is.

Personally, I focus on trend of granular metrics which makes LTV and CAC.

CAC is basically (Sales & Marketing Expense / No. of new customer added).

LTV is roughly (Average Recurring Revenue per Account * Gross Margins%) / Net Revenue Churn Rate

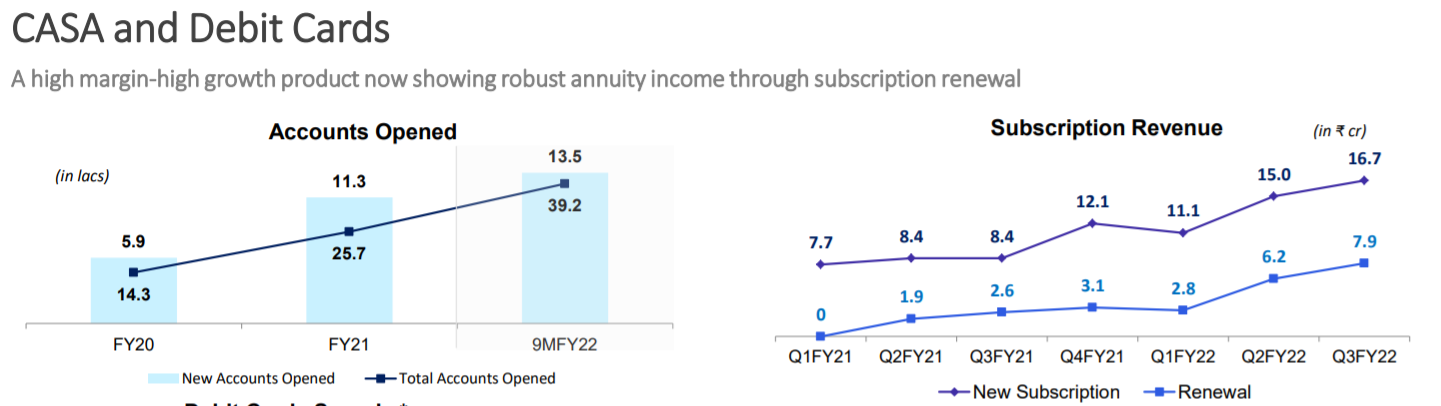

One of the unusual player in SaaS is Fino Payments who is charging for their Bank Accounts as a SaaS wherein the customer has to pay yearly fee of 450/- to keep his account active. Some portion of this fee goes to merchants. They have provided the subscription revenue in Q3FY22 presentation.

market…

market…