Climbing the wealth ladder : A very interesting read.

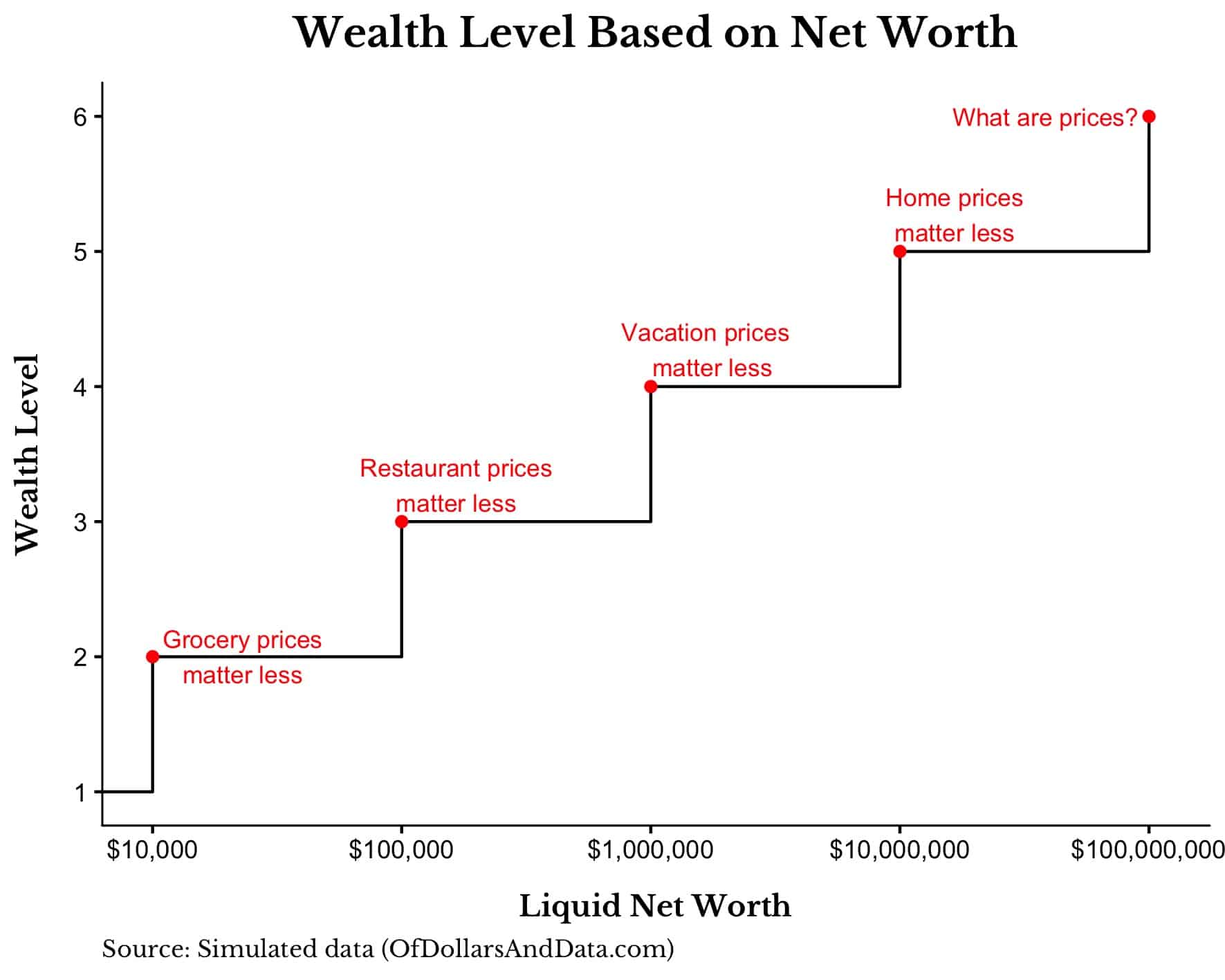

If we use the 0.01% threshold as a guide, a working-age adult could use the following amounts to determine their wealth level (note: the x-axis is a log scale):

I choose these specific levels because, for each category, the marginal spending decision represents about 0.01% of the net worth level shown. Let me explain.

Let’s say you are at the grocery store and you are deciding whether to purchase a dozen eggs for $1.99 or a dozen cage-free eggs for $2.99.

If your net worth was $1,000, this single choice (paying $1 extra for cage-free eggs) could have a slight impact on your finances as it would represent 0.1% of your total assets. However, if you were worth $10,000 (or more) the decision to spend $1 more would likely be trivial to your finances since it represents less than 0.01% of your wealth.

Nevertheless, we can extend this thinking to more expensive spending categories as well. For example, imagine you are in a restaurant where you are deciding between a burger for $15 and salmon for $25. If your net worth > $100,000 then the $10 difference is trivial (<0.01% of net worth). If you continue to scale this logic upward you will see that the marginal impact of a single decisionwithin each level of wealth could be as follows:

Level 1. Paycheck-to-paycheck: $0-$0.99 per decision

Level 2. Grocery freedom: $1-$9 per decision

Level 3. Restaurant freedom: $10-$99 per decision

Level 4. Travel freedom: $100-$999 per decision

Level 5. House freedom: $1,000-$9,999 per decision

Level 6. Philanthropic freedom: $10,000+ per decision.

When you view wealth in this way, it looks more like steps than a smooth, ever-increasing line. This is because most people in the same level of wealth consume in much the same way. If you are in level 3, you don’t fly private and you only fly first class if you are lucky enough to get upgraded. If you are in level 1, you rarely fly.

More importantly though, the best way to climb the wealth ladder is to spend money according to your level. If you are in level 1 and you book a vacation without caring about the costs (level 4), then you won’t progress further up the ladder. Until you have the money to spend frivolously within a level, you have to be strict about your spending in that level. Get this right and you have a far better chance of progressing up the ladder.

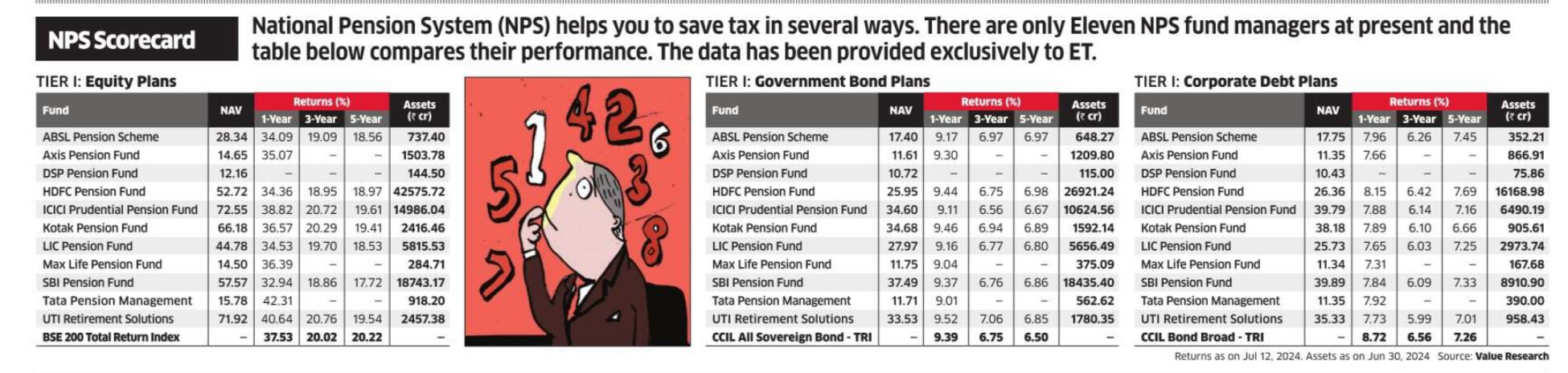

While the National Pension System(NPS) has gained a lot of traction over the past few years, it is important to track the asset managers and switch funds to the best performing ones.

Here’s a comparison of fund performance across Equity, Govt. and Corporate Debt:

Hi

I think its the case with Tier II NPS holders only since individuals like me who have their NPS in Tier I only don’t have the option to switch. I worked in PSU bank for nine years and it was mandatory for us to be part of SBI pension fund corporate debt plan only with no option to switch. My bank was Allahabad Bank. Now I left the job but decent amount still lying there, I can only withdraw 20% as per rules. I was wondering since I no longer belong to the institution why is it still compulsion to be part of corporate debt plan only. There must be option for individuals like us to switch to equity pension funds.

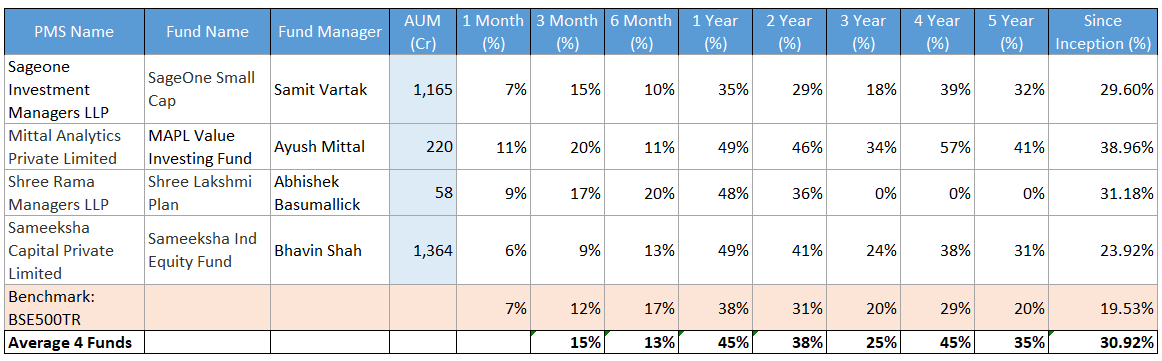

I made some changes to the PMS Benchmark, as @aveekmitra’s advisory returns are no longer publicly available.

The current benchmark is an average of 4 PMS funds, which I consider as my Opportunity Cost (in other words, If I am not investing on my own, I would distribute my corpus equally among these 4 PMS’)

Good callout! Of course, these are leading funds beating the benchmark. I have added the BSE 500 Total Returns Index which most of these PMS’ use as their respective benchmark to beat.

Important note from Delhivery CEO on quick commerce and why it will have huge challenges sustaining the current growth rate once the $40-50 million monthly burn reduces

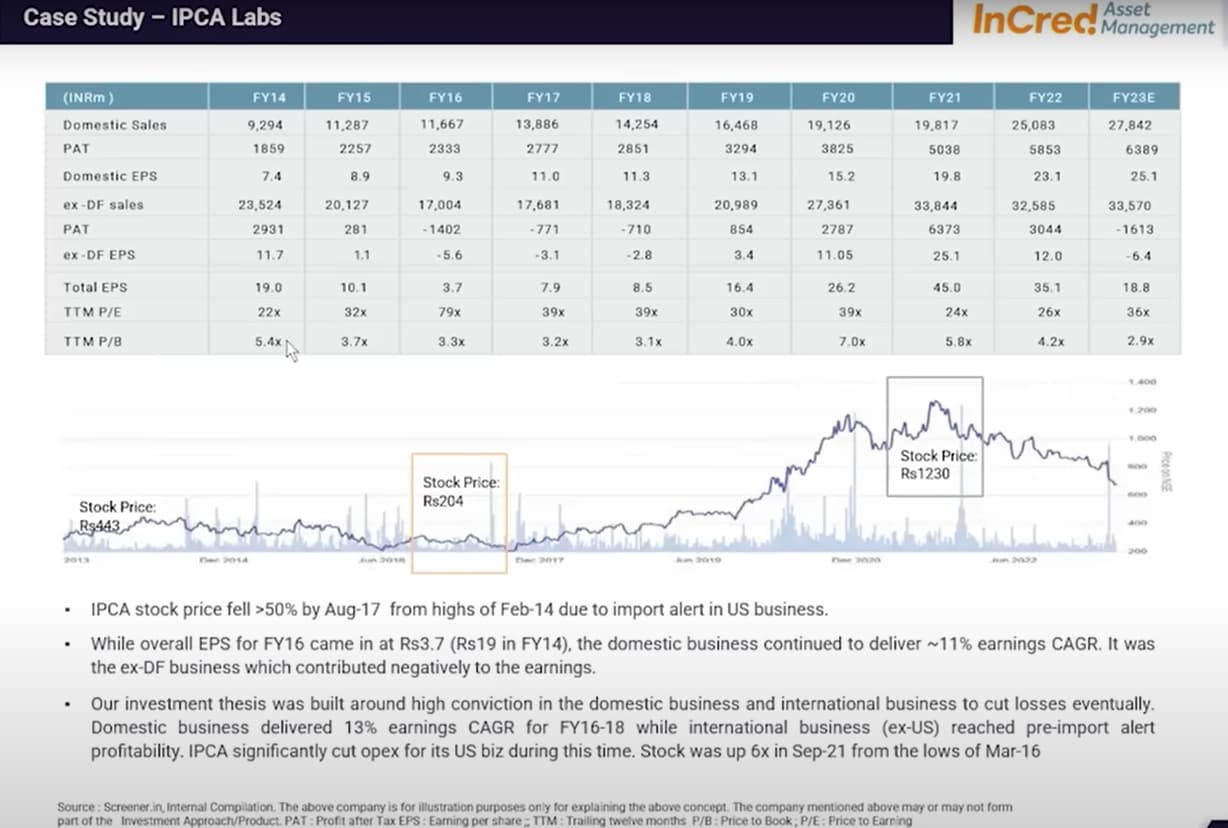

Critical ratios to check:

P/B - As it accumulates all historical profitability across a 10-12 year cycle

EV/OCF - Ignore reported PAT and compare EV (including debt) and OCF( with realized tax payments)

ignore P/E - Accounting issues, short term fluctuations, child to parent entity tax/ESOP issues etc.

A lot of attention is paid to this market cap/GDP ratio and what it means for the relative cheapness or expensiveness of a market. However, not enough attention is paid to the size of the opportunity in India , how it has grown over time, and how that opportunity will become exponentially larger if the prediction about India’s future economic growth, made by Mr Sanyal and many other commentators, turns out to be roughly right. Just think about this for a moment: If India’s GDP reaches the $29-33 trillion range by 2047, India’s market cap will also increase from the current $5 trillion to $30 trillion, or thereabouts.

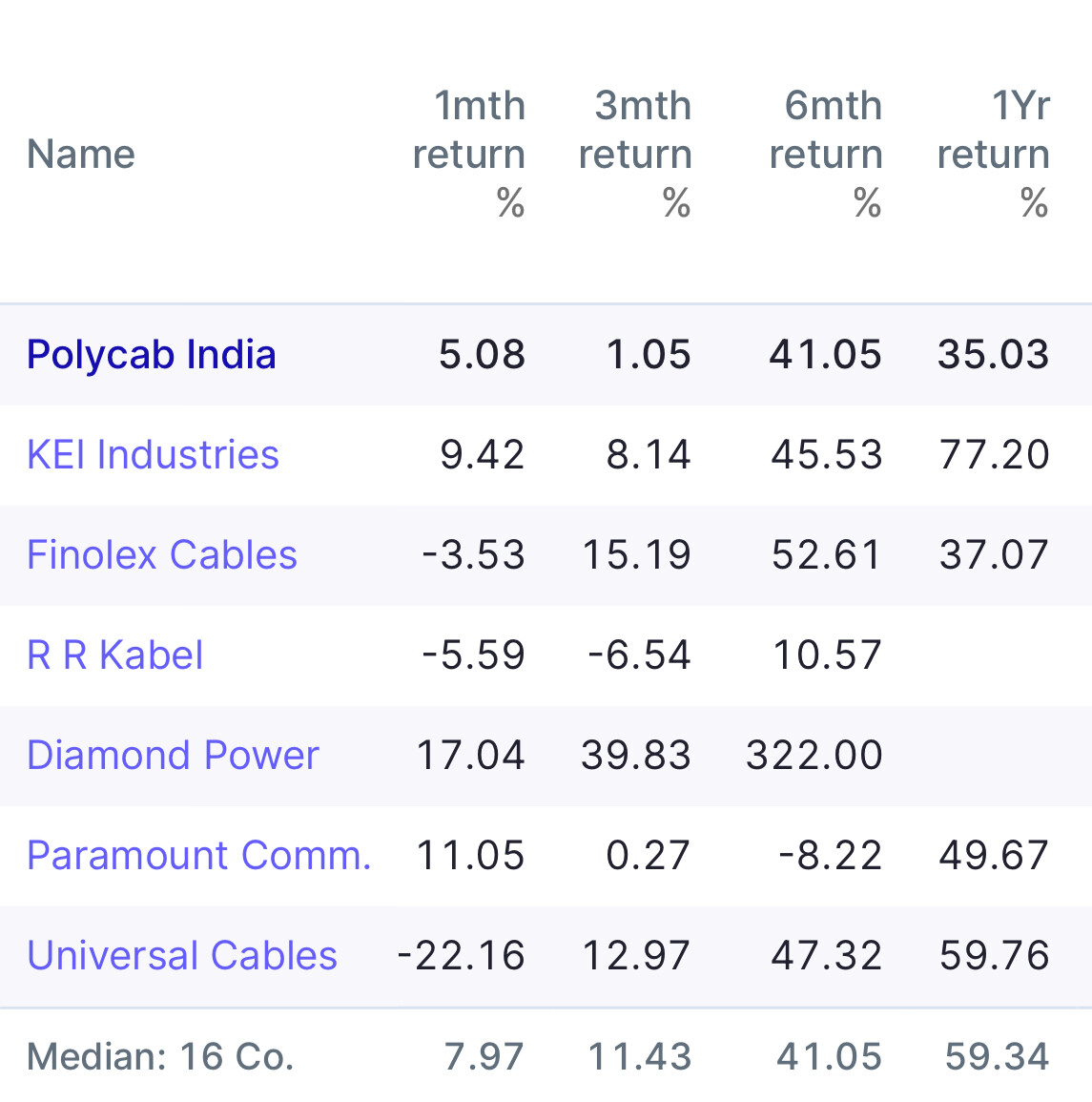

Avoid getting anchored to cost price bias when monitoring portfolio performance.

As an existing holder who is holding the stock from lower levels, because of way I track portfolio (cost price driven), I will miss that the stock has done nothing for last 3+ years

This approach misses the

huge relative underperformance even against index, let alone other stocks

opportunity cost of not deploying capital effectively

So I think we should listen to William O Neil and not track portfolios like this, here is what he wrote in his book

“To help you avoid the price-paid bias, particularly if you are a longer-term investor, I suggest you use a different method of analyzing your results. At the end of each month or quarter, compute the percentage change in the price of each stock from the last date you did this type of analysis. Now list your investments in order of their relative price performance since your previous evaluation period. Let’s say Caterpillar is down 6%, ITT is up 10%, and General Electric is down 10%. Your list would start with ITT on top, then Caterpillar, then GE. At the end of the next month or quarter, do the same thing. After a few reviews, you will easily recognize the stocks that are not doing well. They’ll be at the bottom of the list; those that did best will be at or near the top. This method isn’t foolproof,but it does force you to focus your attention not on what you paid for your stocks, but on the relative performance of your investments in the market.”

PS: Very easy to track this today thanks to Screener. Just add your PF stocks to a watchlist and track the trailing 1M, 3M or 6M returns add the end of the respective periods

The sheet you shared is very good for seeing information at a glance.

Can you brief how to add information of promoter , fii, dii and retail holding in the sheet…I understand that the information is first fetched on Data Sheet & then polished for further analysis/ plots.

Not getting a clue as to how to get this on data sheet.

You can basically leverage all the data that is present in the Data Sheet and build analysis/charts around those. Unfortunately the shareholding information is not added to that sheet and hence you can’t bring those data for further analysis in an automated manner.