Investing Accelerator Summit (IAS)

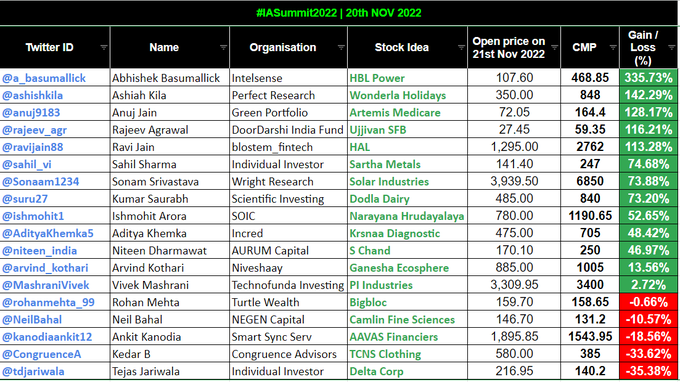

2022 Session - Performance over last 1 year. Some great picks

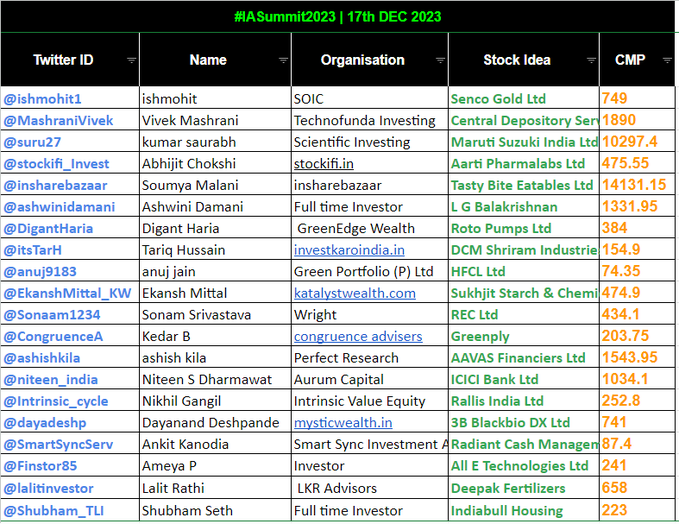

2023 Session - 17th Dec 2023

Pointers from some key presentations

[Courtesy Twitter Handle: @bhaavander (https://twitter.com/bhaavander)]

1. Senco Gold: Play on organization play in the jewelry industry. Headed by 4th gen entrepreneur Sukumar Sen. Trend tailwind in this sector for all players. COCO, COFO and FOFO stores are 3 models. The company mainly operates in COCO stores. Eastern geography player expanding there. So brand building in that region. LGV can also be an opportunity for them. Aspirational customer base as their average revenue from one is low…so beneficiary of LGV where low-cost sales are big. Same-store sales growth is also increasing where expenses don’t increase so margins can increase.

2. HFCL: Gov pressure to grow indigenous tech development in Telecom and Defence sector. Big company known for optical fibre cable but also moving into telecom and defence. HFCL is working with a lot of big names to develop RnD partnership with Wipro etc. Rerating is a big opportunity in long term when revenue from Defence becomes substantial. Dependent on gov dealings so projected timeline needs to be taken with a pinch of salt. Opp. size is big. Rerating can also due to happen in Telecom segment. Product is already tested and implemented in standardized geographies like US so high chances of acceptance and growth here. PLI scheme beneficiary. Anti China sentiment will also benefit the co.

3. Greenply : Plywood has the largest share in the wood panel sector. Type of duopoly in the sector just Greenply and Century ply in organised sector. Organized players going to continue to increase mkt share. Antifragile- not just survive but thrive in chaos. marketing becomes imp as the sector is also customer facing so brand takes time as well as effort, so that also adds to the expense. MDF is low gross business but once capex comes online, the margins come back to optimum levels. Everything is a function of place and time!

4. All E Technologies: Product engg partner with Microsoft, winning MS partnership awards for 6 times in last 15 years. OpenAI azure service access to them due to partnership. Already deployed some solutions. With marquee clients like MMT, later increasing to other travel services like yatra due to their work with MMT. Product pf from Edtech, manufacturing and customer exp solution, Banking etc. Thesis- moat may not be in the product but with the channel partnership. Co-sells with Microsoft.

Picking One- Capabilities VS Scale. needs to focus on one then go for another. Promoter is focused which is vital for a small company

5. DCM Shiram: For Rayon compared to sister company, SRF is not interesting in growing this segment but DCM has been constantly improving.They are good at partnering with the leaders when starting a new business.

6. 3B Blackbio DX: Now a microcap Kilpest renamed 3B Blackbio DX Ltd. Evolution of company in last 50 years from agrochem to covid tests to molecular diagnosis company. Recently merger was subsidiary approved with the subsidiary and renamed. The story continues after the merger. Various applications of molecular diagnostics but oncological diagnosis is the most popular and focus of the co. understanding the whole market - 25B $ industry. Indian mkt post covid growing at 7% .

Players- Roche and Abbot foreign major players. 3B is a major player in oncology reagents biz.

National competitions- Tata md, Molbio , Mylab are established players and some startups are also coming on. The mkt is growing and growth drivers like awareness, medical tourism, portability are in place. Special situation playing out, with clear minded promoters with a lot of growth triggers even inorganic opp to grow present. will be interesting to see them walk the talk. no listed player to compare but looking at valuations, long runway to grow yet. Very low PE P/S compared to healthcare cos.

7. Sukhjit Starch is the next co. the company produces sugar and starch derivates

4 units spread across. Corn is the raw material so its good to be closer to decrease logistics cost.

Co also focused on constant capex. Now back to capex after facing some issue. Captive power plant to be setup in their other location to increase margins. Competitors Rocket and Guj Ambuja Exp.

Consumption of starch is low compared to foreign countries but increasing. Promoters have skin in the game with second generation also focused on the business. They are also buying regularly in open mkt. It has been out of favor for sometime. But with capex coming back margins can expand. margins are cyclical

8. LG Balakrishnan bros are majorly focused on motorcycles, and most Indian motorbike cos are their clients. Big Capex coming online with automation to increase efficiency. Available at cheap valuation! Some major concerns - family tiff with son so succession issue. Requirement of chain in EVs But the selling by son is over now and promoter is going to take holding back. Chains are time tested tech, in motorcycles chains are still used. and high speed EVs might still need bikes.

9. Aarti Pharma : India becoming the pharmacy of the world, and the API acive pharm. ingredients is v imp. Aarti pharma is one company from the Aarti well established group great experience in the industry. Aarti pharma is focused on CDMO. Aarti pharma supplies to North America etc. They have higher margins due to specialized APIs. Large chunk comes from Xanthene. Sole non Chinese manufacturer of Xanthene derivates. Capex factory coming online in Atali, Gujarat. Focusing also on backward and forward integration so not to be China dependent.

Risks like raw material cost fluctuations due to global issues present.

Fundamentally- Forward multiple <20PE

scope of rerating.

10. Roto Pumps: Go with the flow! Simple VS Complex pumps Huge opportunity for complex pumps in India if the infrastructure industrialization is going to happen. Roto Pump is the only listed company.

Spare parts and servicability is very imp in this sector as its complex and only highly skilled or maker company can do. Room to grow Domestic mkt 1300Cr whereas Global mkt is 300000 Cr ! Small, Niche Company! Good technocrats promoter with 60% holding.

11. Radiant Cash Management: Entire presentation shared MissioN SMILE