Q1 results will be announced tomorrow… Let’s wait for it, many paper stocks such as West coast, jk paper, balkrishna have had a smart run but RUCHIRA is still subdued, probably market is waiting for the Q1 results.

Super results by Ruchira…Revenue increases by 23% YoY, PAT up by 63%, EBIT @ 14.8% vs 11% YoY

http://www.bseindia.com/xml-data/corpfiling/AttachLive/bcb52d65-9056-40f0-8f10-786a093a69fb.pdf

6 Likes

Ruchira Con Call Transcripts. Management bullish on prospects.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/37a960bc-fecd-4465-a65d-c9ec4d771c9d.pdf

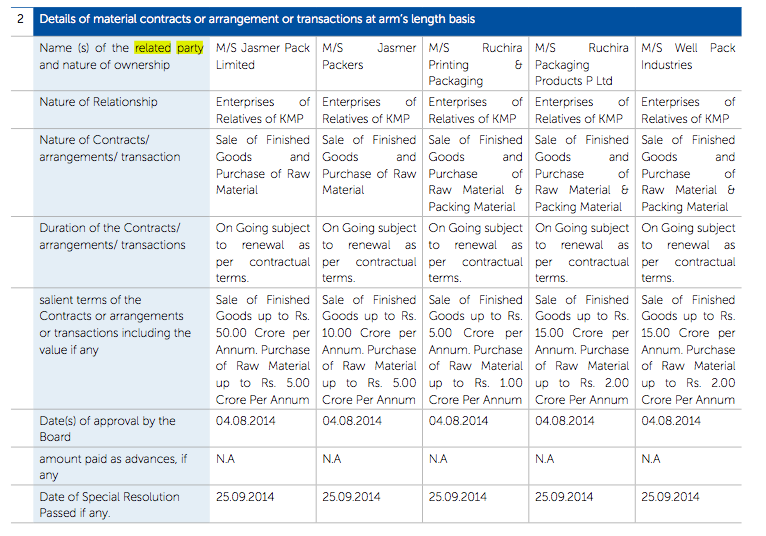

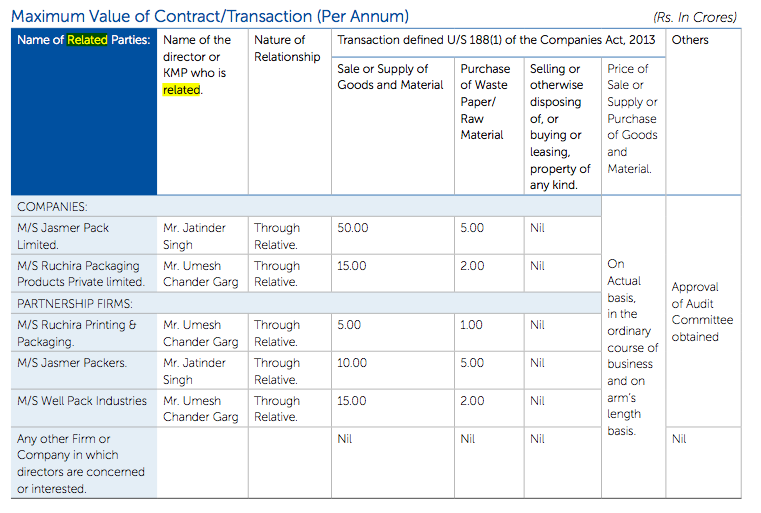

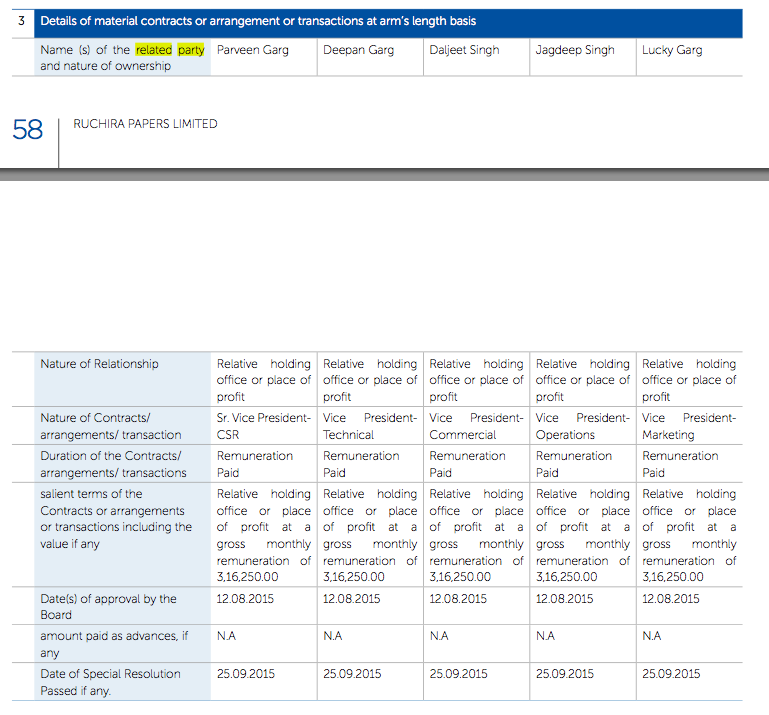

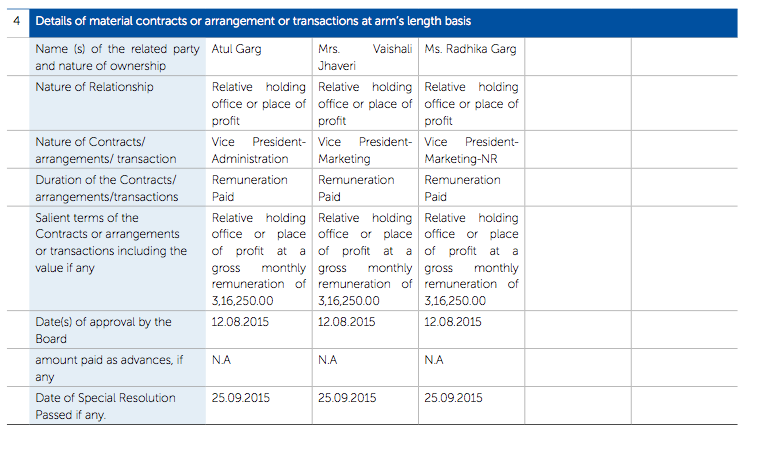

I was going through their latest annual report. Under " Related Party Transactions" they have mentioned about their family members holding various positions (all of them VPs) in the company. Moreoever, each of them will be paid monthly remuneration of Rs. 4,00,000. This was something of a concern to me.

So have I understood this right or am I making a reading error? This is apart from the top management salaries of Rs.8,00,000 per month.

Is it common across the family run companies? Agreed that company has generated good profits over the last couple of years and improving operationally, but this seemed a concern to me. It would be great if you can give your views. Thank you

Disclaimer: Invested in it over the last one year. I was planning to add more but then this concern came up.

1 Like

Thank you for this.

But in their latest annual report, it is mentioned that the salaries of all them have increased to Rs. 4,00,000 per month wef 1st July 2017.

So, effectively 8 family members drawing salary of Rs. 4,00,000 per month along with proposed Rs. 16,00,000 for 3 top men. So effectively, it becomes Rs. 80,00,000 per month or close to Rs. 10 Cr per year. This still does not include perks.

Maybe I am reading way too much into a non-trivial issue, but this is something that is of concern to me.

Dis: Invested

1 Like

Indeed. I saw the same increase in salaries, and once I came across the related party transaction, my concern grew into action.

The only question I had was whether the precise amount of the salary for all members of the group ( 3,25,000 ) was exactly below the legal threshold of a requirement. I couldn’t find anything on the net.

Some insights into paper industry…

Excellent Results by Ruchira Papers in Q3.

Total Sales increased by 13 % YOY with the corresponding quarter last year.

PBT rose by 59% YOY with the corresponding quarter last year.

PAT Rose by 45% YOY with the corresponding quarter last year.

Q3 EPS stands at 5.23 compared to 3.59 last year during the same period.

OMP stands at at 18.22% improved from 15.9% from last year during the same period.

Stocks trailing twelve months PE stands at 13.41.

1 Like

The concern now is only on their half baked expansion plan. Need to see how it’s shaping up in the concall

Entered at 174.

Sales Growth = 15.87

Profit Growth = 54.18

ROE = 23.45

Dividend = 2.25

CF Operations = 33.04 cr

Debt To Profit = 3.61%

EPS = 18.44

Hi, i came across this forum some time back and realised how foolishly i was making my decisions. Not that i have become any wiser, its just my mistakes have started looking glaring

On the paper industry i am quite confused with two contradicting thoughts which are arising from various news articles. Some articles claim that the ban in China has led to more demand from indian manufacturers and that the indian paper industry has seen a revival. On the contrary, the paper industry association has been asking for a import duty to fight the rising imports here which is making survival tough.

Can some of the members help me understand here what play is happening with regards to the paper industry in general and how Ruchira would be affected.

http://www.thehindu.com/business/Industry/rising-imports-pose-threat-to-paper-mills-in-india/article23035211.ece

@NoobsterKing: What I have come to know is that the ban in china was on the use of cheap quality raw materials and waste materials like plastic etc for production of paper. This has forced the Chinese players to use better quality raw materials and their raw material costs are now on par with Indian players. So the China ban didn’t hamper supply from China for a long period and things appear to be restored now. Ruchira papers Q3 concall transcript has a mention of this: http://www.ruchirapapers.com/pdf/Ruchira_papers_Conference_Call_Q3FY18_Transcript_final.pdf

Management salaries isse is also being highlighted by Dr Vijay Malik in his blog while analysing ruchira papers…

I’m new to stock market , was planning to buy small quantities of ruchira papers but this issue restrained me.

Can you please share the link to the blog … thanks in advance

Disclosure : Minor holding in the portfolio.

Last quarter results seems to have been very adverse … sales, margins and eps all have fallen drastically in the last quarter. However, the full year results is ok as diluted EPS has increased from 14.29 to 16.86

Any views on reasons for such a bad quarter ?

Kraft paper contributes 40% of Ebitda .This time kraft facility was closed for 25 days or 1 month so EBITDA contribution from kraft was only 26% down by 14% YOY.

Q4F17 EBITDA was 16.27cr less 14% it comes out to 14cr So EBITDA FOR QFY18 is 14.67cr.

Now in q1 the benefit of modernized plant will contribute which will improve revenue as well as margins.

Interest coverage ratio is 6 times so there is no fear of increase in finance cost till now.

3 Likes

This is now trading at 6.5 PE inspite of its good performance. Is it cheap? Historically it was trading less than 10 PE though.

-

Company has plans to expand 1lakh metric tonnes of capacity for which around 107 acres of land has been purchased. Clearance to come by October this year.

-

Planning for production of 1 lakh 33 metric tonnes this year against 1.15 lakh.

-

Management guided EBITDA margins to increase by 150 bps at around 18%.

Just trying to understand is it trading close or less to its intrinsic value?

2 Likes

1 Like

hi. management salary is an issue which has stopped me from adding to my position. also dont think the company has a viable moat around it. although i plan to remain invested in it for another 2 years.