we need to understand why promoter is consistently selling from one year or so? they have to come up with clarifications right?

The promoter is converting share warrants into equity shares as per the below link:

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=138193c6-a805-48f5-8380-36d8a4010307

I am not well versed on the basics of share warrants ( so forgive me if this is a stupid question  )

)

- Can I assume that the share warrant was issued by the promoter as a way to infuse cash/capital ?

- Will the EPS go down , since the number of shares will increase proportionally ?

Hi…

Yes - your both the assumptions are correct. The key point to note is at

what price the warrant was issued. Though it is as per SEBIs formula - some

promoters issue it at a higher price than the market price at the time of

announcing the warrant, which is a positive.

Ofcourse, the best thing is for investors - is if promoters issue

preferential shares for themselves for immediate cash infusion rather than

warrants which will get converted into shares within 18 months.

1 Like

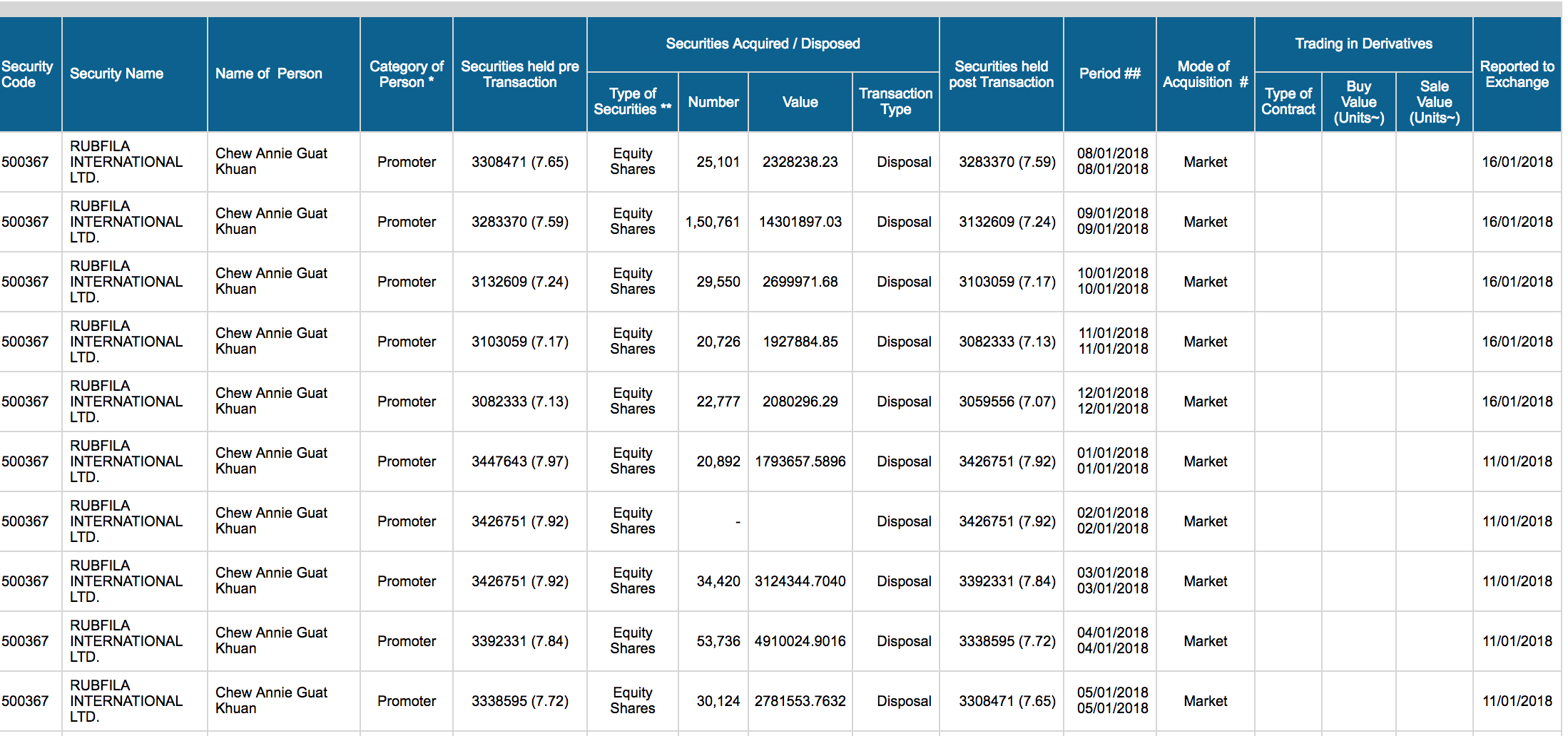

Issuing warrants to themselves (8 months back at Rs.50) and then selling whatever they hold in the open market at a price much higher than the warrant price (between Rs.80-90) has certainly got to be the oldest trick in the book? The promoter has sold 17 lakh shares between Sept and Jan this year and has plans to convert 20 lakh warrants issued at Rs.50 issued back in May. This can’t be good right?

Disclosure: Not interested.

7 Likes

I see this as one promoter group consolidating and other promoters liquidating and reducing their stake.

Just check share holding from 2014. There is a clear pattern.

1 Like

Acquisitionof shares

is thro conversion of warrants.

Rubfila has not seen a meaningful correction in the recent market meltdown. A subdued Q3 could well have been a result of the GST issues having taken a little longer to resolve. It is however evident that GST is a thing of the past & the co. could well return to its growth trajectory. A robust Q4 should clear the air.

3 Likes

Guys …can any one have latest update of Rubfila …Since all Mid cap stock is touching bottom

but we did not seen any big correction in Rubfila and thats makes its interstening

I just started looking at Rubfila again in anticipation of today’s Q1 results and was astonished to see heavy selling pressure for the entire day, well before the disappointing results and acquisition announcement.

What is going on? Does this happen regularly? It is certainly the first time I am seeing this up close.

Rubfila International has decided to subscribe to 50% of the paid up capital of Premier Tissues India Ltd., a subsidiary of Ballarpur Inds. Premier Tissues is into all kinds of tissues / paper rolls & have a decent brand recall. Attaching their product brochure.

Brochure.pdf (1.3 MB)

This could be Rubfila’s attempt to get into the B to C segment through this acquisition as currently it is only into B to B. Premier Tissues did Sales of about 53 crores in 16-17. Going by the fact that Tissue paper is the fastest growing segment in the paper Industry, this could potentially have a major bearing on the Co. going forward. Attaching the AR of Premier Tissues for 16-17.

Also attaching a recent report on the Indian Paper industry highlighting the fact that Tissue paper segment is growing at a CAGR of 15.5%

Paper Industry - Investec.pdf (2.8 MB)

What is however not clear is as to why Rubfila is acquiring only 50% stake in the Co. Perhaps it is the first stage of the transaction, or perhaps it will bring in fresh funds into the Co., & thereby increase its stake. Whatever it is, it will pay to keep a close watch on the developments here as they unfold over the next few months.

3 Likes

There are three promoters in Rubfila viz, Patel family which came in as promoters by way of buy out, KSIDC and Malaysian. In Sept 17, patels had 39.33%, KSIDC 6.33% and Rubpro Sdn. Bhd., Malaysia 18.66%. Coming to Sept 18, Patels increased to 48.09% while KSIDC was down to 6.05% and Malaysian down to 13.82%.

So the Patels have in fact been increasing their holdings.

2 Likes

Ur views now on this stock?

Today’s announcement that the promoter of the Co. Mr. Ruchit Patel has acquired 56,20,427 shares of Premier Tissues India ltd. means that the acquisition of Premier Tissues is complete. Rubfila had about a year ago acquired 50% of Premier Tissues. The balance has now been acquired by Rubfila’s promoter, it appears in his individual capacity.

Premier Tissues is into Tissue paper, which is the fastest growing segment in the paper industry. It has created a brand called Premier & is quite popular. This could materially change the investor perception of the Co. The link to the Premier Tissues website: https://www.premiertissues.com

The Co. is also in the middle of its expansion of its regular business of rubber threads as it setting up six production lines in a phased manner. The promoters have also been increasing its stake gradually,

3 Likes

Rajeev,

Seems you are tracking for quite some time Co., so few Qs -

- At what price Premier T 50% bought by Promoter/Ruchit? Why not Rubfila itself bought?

- As per 12th July’19 meeting 45 lakh warrants/shares issued to Promoters without reference to any price. Any idea what price?

Bharat Patel, himself is an Investor and not disclosing critical information. Get doubts on his intentions or may want to recover from his earlier losses on account of other minority investors…![]()

Thanks.

In addition to the investment in Premier Tissues, the Co. further invested an amount of Rs. 11.94 Crs to purchase a 100 odd acre plot of land in Tamil Nadu where it is doubling its production capacity by adding six more production lines for manufacturing latex rubber threads with installed capacity of 15,000 MT in a phased manner.

The Co. is also setting up a paper manufacturing unit of 20,000 MT p.a. This is in addition to the 50% stake in Premier Tissues Ltd., which owns another 10 Hectares (25 Acres) of land & 1 Lakh sq ft of built up space.

The Co. continues to be debt free & all these investments are being made from internal accruals as well as fresh capital from the promoters by way of warrants. The previous tranche of 400,000 warrants were converted @ Rs. 47.50. The pricing of the fresh warrants issued is not evident to me, but will have to be done at the SEBI approved formula. The promoter increasing stake in the Co. is a positive. Besides, the retail investors are free to pick up shares at a 30% discount to the promoters previous conversion price.

One negative for me is the lack of information that the Co. is willing to share with its share holders. There are no insights in the AR for the investment in Premier Tissues & when the investment will start contributing meaningfully to the bottom line.

Other than that, the stock appears to be valued attractively.

3 Likes

Latest warrants are at 42.50 if my memory serve me right

Falling crude prices would make spandex an attractive alternative to rubber threads.Hence most of the growth in the market might be captured by spandex

Does rubfila have plans to make spandex?

A more pertinent question for near term valuations is,what are the margins of Premier Tissues and can we expect the margins to increase?

Rubfila came out with a decent set of consolidated Q4 numbers with an EPS of Rs. 3.25 for the year. The Co. has declared a dividend of 24% (Rs. 1.20 per share), with a dividend payout ratio of about 35%. What is heartening is that the paper unit has started contributing to the earnings. Besides, as the Co. owned only 50% of the Premier Tissues (paper unit) in the year gone by, only half of the profits were accounted for. The current year will see the entire 100% being accounted for as Premier Tissues has now become a 100% owned subsidiary.

The Paper unit is still in infancy & in the process of being scaled up from internal sources & fresh equity being brought in by the promoters at 30 to 40% premium over its current market price, & the current year should see revenues from the paper unit match those of the rubber threads unit. It is known that the tissue paper segment is the fastest growing in the paper industry. The Co. sells under the Premier brand which is quite well known.

This debt free Co. is available at book value with a total market cap of only 150 Crs. & a dividend yield of 3.75% & looks pretty undervalued.

3 Likes

I just came to know about this company and i went through your post. its a great find for me atleast. Just goes on to show there are so many companies which are leaders in their segments but we are unaware unless we go through Valuepickr meticulosuly. The use and reach of Rubfula products are quite vast and with their capacities being commissioned (Dindigul factory) surely this will start reflecting from this quarter.

3 Likes