RPSG May have 25-30% holding in IPL Team.

2 Likes

Register conf call: https://www.bseindia.com/xml-data/corpfiling/AttachLive/e4699172-0dd4-40b5-80ca-8770c777d024.pdf

recently uploaded by the company. Promotes itself as a growing FMCG company with four major brands.

- Too yumm

- Evita.

- Naturali.

- Dr. Vaidya’s.

No mention of the IPL franchisee/ Mohun Bagan, Souledstore (which is indeed a seperate entity), Herbolab, Bowlopedia etc.

edit: I just went through the presentation again. It makes me feel as if the company wants to be focused on FMCG. Their previous intentions of being a a company that gives rise to unicorns seem missing.

4 Likes

Some clarity regarding IPL team holding has come.

‘A subsidiary of the Company, namely RPSG Sports Private Limited has been incorporated wherein the Company is holding a 51% stake and the balance stake is held by private and unlisted company of RP-Sanjiv Goenka group.’

4 Likes

- Is the subsidiary 100% held by RPSG Ventures?

- Will this subsidiary also include complete holdings of Mohun Bagan football club and RPSG Mavericks?

- Is there a retail brand of sneakers, clothing and perfumes that RPSG intends to monetize? Like Thesouledstore?

But, I have also started seeing some warning signs.

https://www.rpsg.in/business

The website has been updated and RPSG Ventures is now under ‘consumer and retail’. So, this means that the promoters are only using it to help finance their other acquisition and businesses and this will be only an FMCG company in the long run.

PS: Disclaimer.This is my assumption.

APA Services Private Limited is a subsidiary of RPSG ventures which holds both Mohan Bagan and RPSG Mavericks.

You may need to refer to http://www.rpsgventuresltd.com/

FMCG is a vertical of RPSG V. The same is clear from other reports. Like segment results published on Exchange -

Currently, it is like a Holding Company. But in long run, need to watch…

Thanks.

2 Likes

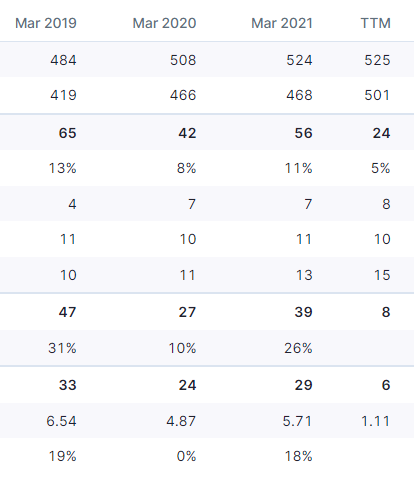

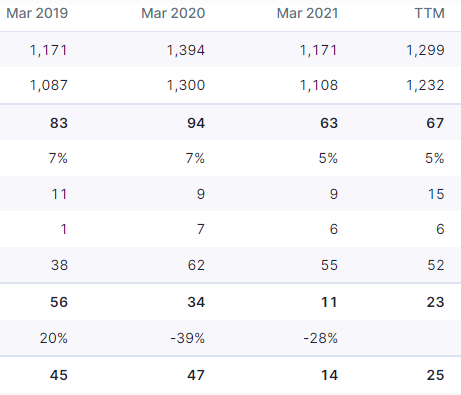

Have recently started tracking the company, and one thing which irked me is the numbers of Guiltfree Industries. Despite the company spending so aggressively on Ads and distribution, the sales have nearly halved in FY21 while other FMCG and packaged foods business have done quite well.

The above loss amount is huge, and despite all the investments the revenue are not budging. Am I missing something here?

3 Likes

It remains to be seen how RPSG fares in the coming quarters. I do not see cohesion in their capital distribution.

I am a big fan of their products, likely covid is a reason for the decline, since a lot of the snack consumption likely happens outside the home, just look at DFM or Prataap in similar biz. They have a wide variety and are at a good price point, have been hoarding their products since they have been available at discount sales recently on all grocery platforms. These sales seems to be over now.

Disc: not invested

1 Like

If covid was the reason then they definitely lost market share to Diamond, DFM, Lays and other players as all of them have posted growth in FY20 and FY21.

Just look at the overall industry scenario here, not arguing about market shares etc.

DFM, margins% and bottomline

Prataap

How do you know Lay’s figures?

3 Likes

Does anyone has any idea on fund raising?

2 Likes

Results seem to be pretty good in all respect.

3 Likes

12:46 onwards is where they talk about the IPL venture.

Edit:

IPL:

Different way of looking at IPL. Huge value creation opportunity. Expect valuation of 2 billion in 5-7 years.

Economics have changed for the better since made the bid. Broadcast rights will go at significantly higher sums than was anticipated.

Investment in year 1 - 500 crores.

Years 2-6 - 250 crores a year

No further investment after.

This is less than 2000 crores for an IPL franchise.

Chennai Super Kings is valued at 7600 crores

Look trophies and vanity investments at 25/30. Only fools look at vanity investments at 60.

1 Like

Edit:

Sponsor interest? Outside people or RPG group itself?

Each sector takes an independent call. Independent negotiations between LSG and company management. Upto them to decide. Would give preference to own companies, but if someone comes with a better deal, then them.

Response has been good. 26 cr population of UP is a huge market. Overwhelming interest. Almost all spots closed. 1/2 open. Announcements will come soon. MyCircle11 jersey sponsor.

Media rights this year and next 5 years?

Sense is there is huge interest. Could see rates higher than earlier anticipated. But not for me to say.

Business of sport and valuation behind it is undergoing a shift. Getting higher valuation is not a big deal or surprise.

What about recovering investments with sports valuations going up or just a frenzy? (wasn’t about LSG but a general question, ipl rights, etc.)

Don’t look at contribution from each individual investment, but the full package. Not just IPL rights, but popularity and eye balls it adds.

Other sports teams as a business?

Matter of time before football comes into the spotlight. TT investment was low to begin with. Marginal losses. There might be some broadcaster interest going forward. But it’s about building brand and creating ecosystem for sports.

Media business. Acquisitions - open magazine, fortune india, editorji. What is the vision for media business? Digit overtaken prints on spend. Views and plans on ecosystem?

Slowly and steadily increasing presence in the space. Looking for international brands. Will expand digital presence. Not in a hurry. Will do it cautiously, steadily but definitely. Though digital is growing, but print is a viable media for the foreseeable future.

Retail space? “Dont want to be another future”. What is your strategy? Retail expansion in future?

Will add significant square footage to operations. Increased out of store sales hugely (phone delivery, online, etc.). This business has doubled over 12 months and will grow this aggressively. Don’t want to be reckless. Will grow in select geographies. Bengal - biggest retailer. UP - scaled up to 34 stores. Coastal Andhra - biggest retailer. Mumbai - natures basket has huge presence. Focus is on few geographies. Expect higher sales and footfalls in physical stores after COVID

SAREGAMA

Rebuilt itself completely - technology, approach, outlook, etc. Lot of innovation with product delivery digitization. Huge repository.

Carvaan - Great success. Launched Karaoke version last year. More versions coming soon. Focusing on audio rights. Have the biggest banners - Dharma, Bhansali, etc.

#1 in Telegu, Hindi, Bhojpuri and Tamil. Focusing on regional music strongly.

Films - 17/18 films on OTT. Deliberate strategy to focus on budget films. 30/35 days. Appeal to audiences of particular regions. Lot of films specific to North East, Hindi heartland. Subjects/themes/ideas that focus on specific regions. Get very strong eyeballs.

Does IPL deal go beyond business?

Need to be passionate about a business. If you/team isn’t passionate or don’t have competency and efficiency, will not succeed. You don’t invest 7k crores for personal pleasure or vanity. Wouldn’t have invested if didn’t make business sense. If broadcast rights go at 50K crores. Net outgo will be lower than 2200 cr.

3 Likes

Not sure if this has already been posted earlier:

3 Likes

Lucknow IPL team is not doing well. Does anyone know the the RPSG holding size in IPL team?

Even if team does well company will still make losses

2 Likes