I’ve been investing for a couple of years, entirely in Mutual Funds until recently. Since the last month I have started investing in the stock market and am on my way to build portfolio. This is what it looks like at the moment (overall investment very low at the moment)

What do you folks think? Currently in the red, but since the total investment amount is very low right now, I’m okay with that in the short term

Some of the companies I’ve been thinking of adding:

Housing Finance Companies - Govt push for affordable housing seems to be massive. Confused about the company to buy into. PNB and GRUH seem over-priced but growing fast. Indiabulls and Dewan seem better priced. Need to analyze details such as NPA, average ticket size etc. Would anyone have a source where I can analyze and take a decision? (Leaning towards DHFL)

Wonderla - Good management, decent numbers, great prospects

Something in the FMCG space - Everything seems overpriced (ITC, HLL) or not that great prospects-wise (Bajaj Corp)

Logistics - Exploit the GST space. Plus with the ecommerce boom, companies like Flipkart, Amazon may not make money, logistics should see a sustained boom

What would you recommend from a diversification perspective? I’m not very knowledgeable on Metals, Chemicals, Oil and Gas so likely to stay away.

Why do you say PNB is overvalued? I beg to differ here as I would value it based on P/BV multiple instead of PE. Here it trades at forward P/BV of 3 whereas Gruh and Canfin trade at 10 and 5 respectively. Their ROE and ROA ratios are bound to improve as operating leverage is going to kick-in.

Yes, you are correct about PNB. My calculation was on Current P/BV and PE ratio. Going by these PNB is a bit over priced - P/BV of 9 and PE of 48.

Btw, could you share the forward P/BV ratios of the different Housing Finance companies? I’m open to considering PNB as well. Looking to gather information that would help me make a decision here.

My picks in NBFCs are PNB, DHFL and Indiabulls. I’m not going to invest in FMCG at this point of time as they are growing only at less than 10%. I like the Wonderla story as well but have not done enough research on it. Logistics is a good bet, my picks are TCI express, Tiger Logistics or VRL

Cross-check with http://www.ratestar.in/company/pnbhousing/540173/PNB-Housing-Finance-Ltd-217757. I find it better than screener, mostly updated.

Your allocation to IT sector is around 30%. I doubt if Indian IT companies will be able to quickly adapt to the new challenges in IT industry. Pharma and IT may take longer to playout (2+yrs) and hence I would allocate more for NBFCs/Banks. Just my opinion.

No offense, but I think most of your picks are either deep value or value traps. Only a long timeline of holding will reveal the same to you. The most important point is will you be patient enough to hold on for so long while markets are on a roller coaster?

These companies are well followed by investors and they are undervalued for a reason, what do you know better than these investors ??

My opinion… it easy to find undervalued picks. But the important thing is to find undervalued picks which markets are ignorant about and which has some underlying catalyst to trigger the rerating within 2 years of holding. So if nothing happens within 2 years you can cash out.

I too was holding IT stocks like eclerx, infinite because of undervaluation, but sold as it will take time to rerate.

In HFC , Indiabulls housing is a good pick , the main advantage is it has developed its own technology back end to cover tier 2,3,4 cities which will drive growth while keeping costs low.

Thanks for your inputs. I agree, a lot of the companies do appear to be undervalued by the investors in spite of being closed tracked. Regarding these investments in the IT and Pharma space my rationale is as follows:

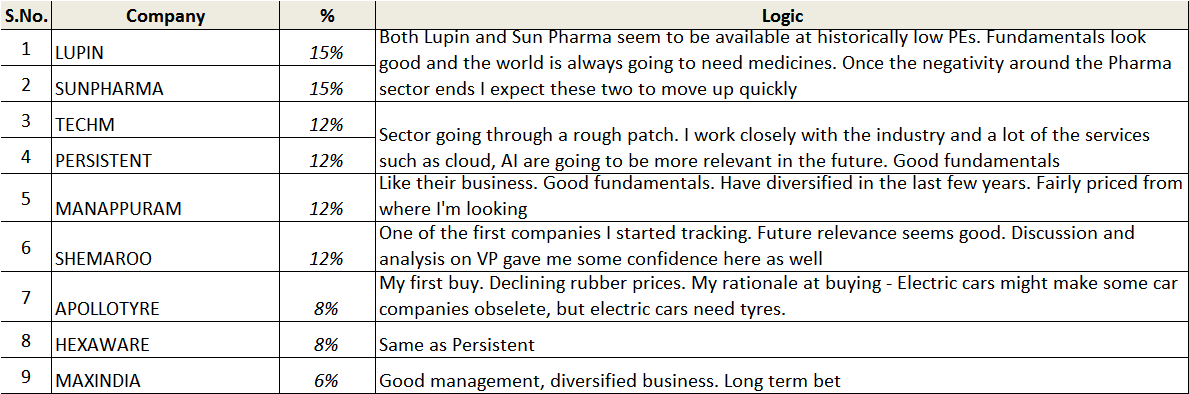

IT: I work closely with companies in this space and it’s evident to me the need for their services is only going to increase in the future. Almost every company is looking to move to the cloud, demand of AI based software, machine learning algorithms is increasing. Persistent and Hexaware are especially interesting in this regard. Tech Mahindra likewise. Pharma: These are the two big pharma companies in a sector that seems to be going through tough times. The numbers seem good, management is very capable. External factors like rupee appreciation, USDA, protectionist stance by the US etc. are impacting it negatively. They’re also available at PEs that are nearing historic lows.

So while the bulls seems to be raging elsewhere, these two sectors seem to be on a bear run while the fundamentals seem intact. I do expect them to be re-rated in a 12-24 month period. I could be wrong of-course

Regarding HFCs - yes, Indiabulls is a good pick indeed. I’m leaning towards both Dewan and Indiabulls. Indiabulls does seems to be plagued a bit by promoter issues which makes me slightly vary.

Great choices and picks, but if you just started your portfolio, slow down on the buying and adding. It seems like a great idea to go into individual companies, but you are starting when the portfolio has the Nifty PE at the 23-25 range. Of course, if you look at the bullish Forward Looking PE of Nifty it will show you at 15-17 (undervalued). Typically, TTM Nifty PE is the best source to look at but timing a down move is not a science with the PE ratio. So, if I were you, then do SIP buying slowly into the HFCs, Pharmas, Real Estate, Cement, IT and some Small Caps. And, these will be great sectors for the next 1-2-3-4 years. But, remember that one cough / cold by Trump and we are all correcting (worldwide).

Yes, I have started recently and there are very small investments. My most standards you could even call them tracking positions.

Agree, PE does suggest an over-bought market so my investment amounts are low and accumulating slowly. Typically I would buy companies that are prices lower than the 50 day moving average and increase my holding with every subsequent 3-5% fall (as long as fundamental are intact)

I’m research HFCs over the week or so and might be investing in a couple shortly. What’s your pick among HFCs?

Hi Roy,

I would like to know why nothing from Banking sector is been chosen. India has a long way to grow and banks will definitely play a big part in it. Private banks like LVB , Federal bank and Karnataka(none of these are a reco to buy) are good value buys for long term. You should look into them.

One thing I would like you to do is hear out a speech by prashanth jain of HDFC, https://www.youtube.com/watch?v=uk6r8KlsO-I in which he tells you why pharma and IT companies performed , its mostly because dollar has gained from 45 rs to 70 rs and now it seems the trend will reverse , so if that plays out then Pharma and IT will take a long time to recover as even if they get more work the payment will be in dollars and profits will be subdued.

Whenever the INR gains against the USD the capex intensive companies benefit .The theme that can work is Infrastructure(not real estate), cement companies , travel aids(vip’s) etc…

Max India covers the health sector and once they start to unlock value it should be a good long term play.

Yes, I’m aware that Finance is missing from my portfolio. Partly because I’m still evaluating my picks from the sector. I have shortlisted a couple from of HFCs and I’m looking to pull the trigger in the coming week or so. I’m looking at a couple of private banks too.

The rupee is gaining over the dollar and the trend may well continue for a bit more. But in the longer term there is nothing that convinces me that we won’t revert to USD = 70INR scenario. I remember post 2008 when the dollar was falling, a lot of folks call it the beginning of the end of dollars superiority. By mid 2011 we at 40 INR for a dollar. Purchasing things from amazon.com at that time was a great bargain :-). But dollar gained again and it’s likely to gain again once the dust settles and people realize that the US economy is as strong as it was before.

Pharma and IT may be depressed for some more time. But fundamentally these two sectors should do well in the longer term. I could obviously be wrong and I will be re-evaluating from time to time.

I agree completely on the benefit to capital extensive companies. Infra, cement along with other related sectors (tiles, household electricals, sanitaryware) will all do well. I’m on the lookout to slowly add from these as well

Thank you for taking out the time to share your views