Royal Orchid Hotels is a group of 3,4,5 star hotels with major presence in Bangalore with pan india ambitions.Company had come out with IPO in 2006 at valuation of around 400 cr and raised 100 cr from investor. Total revenue is around 58 cr at time of IPO and company was operating around 490 room keys in Bangalore and Mysore then. Since then companies expanding into various cities of India through build, lease and managed contract which is common in India. Due to liquidity issue company has to go through debt restructuring in 2013 and sale some of its newly build hotel properties in hyderabad and ahmedabad to delevarage its balance sheet and since last 3 years company has reduced its consolidated debt from Rs 300 cr to below 100 cr currently and plan to further reduce the debt my sale of land parcel in Mumbai. Currently now company is focusing on management contract model for expanding its pan india presence.

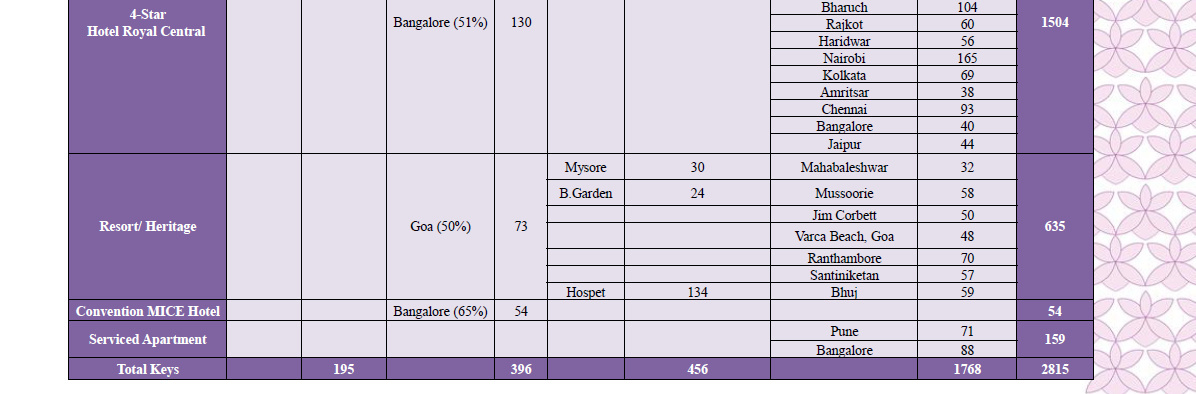

Company total number of room keys under various categories as per Q2 2016 17 investor presentation.

Company plan to reach around 50 hotels and 5000 total room keys in next 1 year. Hotel industry since last 8-9 years is going through tough time however supply of new branded hotel is decreasing since 2014 and since 2015 occupancy rate is improved to more than 60% pan india and last quater occupancy for royal orchid is 68%. Recently company has paid dividend of Rs 1 after many years and posted turn around result in q3 2016 17. In recent concall management sound bullish about medium term prospects for the company. Current stock price is Rs 89 and market cap is around 250 cr and considering land asset

which company plan to dispose off net debt is less than Rs 50 cr. In current overvalued market it seem reasonable bait considering strong brand image, ownership of around 500 3,4,5 star rooms after excluding for jv partner share (it cost around 50 lakh to build per room for 3,4,5 star hotel on average). So at current valuation we are getting other assets in almost minimum valuation. For valuation comparison recently Le meredian hotel (Mac Charles India) with 200 room key is bought for around 600 cr valuation by Embassy Group giving valuation of around 3 cr per room.

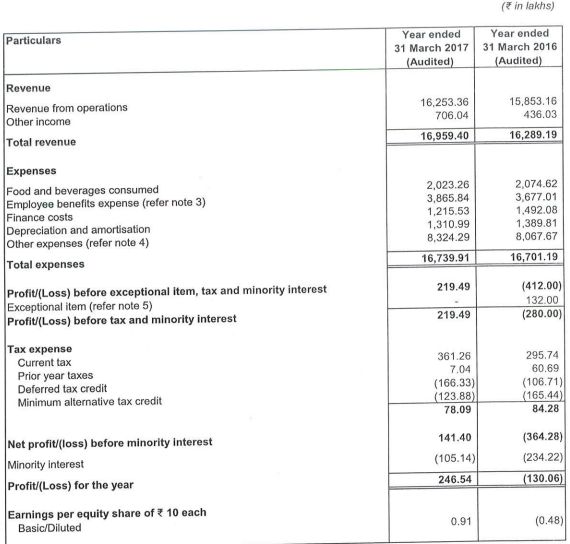

Since last 4-5 years topline is stagnant as average room rent and occupancy level in hotel industry is subdued due to over capacity and company focus on asset heavy model of building new hotels in hyderabad and ahmedabad among others which has backfired. In fy 2016 company has revenue of 158 cr with opm of 13% with improved occupancy level opm can move upto 30% and benefit can pass on to bottomline if hotel industry cycle revives.

Pros:

(1) Promoters has more than 3 decades of experience in hospitality industry with IIM predigree

(2) Company has good brand recall in Bangalore and other localities

(3)Website of company is good with online booking facilities. Company also have hotel management training institute in Bangalore to train manpower

(4)As occupancy level improves per room realization may improve which can cause increase in topline and bottomline

(5) Strong govt push through Incredible india, e-visa and other campaigns to improve tourist inflow likely to benefit the company

Cons:

(1) Hotel industry is cyclical in nature with last two quaters Q3, Q4 contributes significant portion of topline and bottomline

(2) As it is discretionary in nature so global recession, weather related disruptions,law and order related issues, political issues affect hotel industry negatively

(3) Upcoming GST may be negative for hospitality companies and particularly 3/4/5 star hotels

Disc: Recently i have taken position in this share at around Rs 86

As per some recent development company has already sold its hyderabad and ahmedabad hotel and delevaraged its balance sheet and reduced debt from around 300 cr in 2012 to less than 100 cr currently. Also company has ready land in Mumbai and Dar-e-slam and looking to dispose off at good valuation. Currently company is focusing on management contract based hotels only for expansion.

Amit i am recent entery in Royal orchid and plan to hold it for 2-3 years or my expected return expectation is met i.e. 3-4 times from current level. Hotel industry is cyclical in nature but in every industry business cycle time comes when it has to trade above their replacement cost else no body is interested to open any new hotels so when that time comes usually stocks are fairly valued. My general understanding is hotel industry in general among few pockets in this market where it is still undervalued and Royal orchid hotel in particular is available at reasonable valuation. If anybody has to setup a new hotel of royal orchid kind it should cost atleast 600 - 800 cr while still this company is available at enterprise value of around 350 cr. This is my simple thesis for buying this stock. In past management has committed some mistakes but it seems it is on path of recovery.

High operating leverage . Profits should explode once occupancy goes to 75-80%

In addition they have land in Powai which they might dispose off. The area of the free hold land is 4664.90 sq meters which is worth > Rs. 100 Cr ( @ Rs.25 k / sq/ft)

Sir can you comment on the valuation and business sense of The Byke Hospitality (Valuepickr thread). I think it is overvalued with respect to other Hotel chains but it is on the path to churn most of the profit from Hospitality sector’s turnaround. Only thing is that it does not own many properties but uses long term lease property for their operation.

sir it would be helpful for us. Thankyou in advance.

Good numbers on standalone basis, no doubt! But they have been struggling on consolidated level from past so many years. FY17 PAT was 2 cr at consolidated level. Mkt cap is 390 cr, so a lot of good news has already been discounted.

What p/e can market assign to this good 4/5 star hotel chain with an asset light model with a decent BS?

Dear @Mridul Their consolidated numbers are a mystery to me as well. They have subsidiaries and JVs in India and abroad but I haven’t found financials for individual property, not even a geographical breakdown. The current quarter will rationalize p/e to an extent but its not undervalued anymore as it was 6-9 months back. And future p/e in my opinion would depend largely on the tailwinds of the industry which is expected to do well.

Do you know which properties contribute towards standalone numbers and which all properties come under thge umbrella of consolidated numbers? They operate in 4 verticals - Owned, leased, JV, managed.

Well I found something interesting which I had no recollection of. In AR 2017 under “Form – AOC –I” , they have shared details of Subsidiaries, JVs & Associates.

What will be the impact of Revised GST rates on Royal Orchid Hotels? They have a mix of 4 and 5 star properties. Rates revised on the lower side for 3,4 start properties F&B.

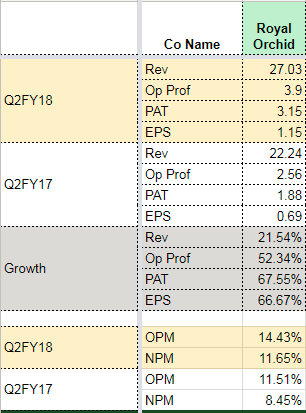

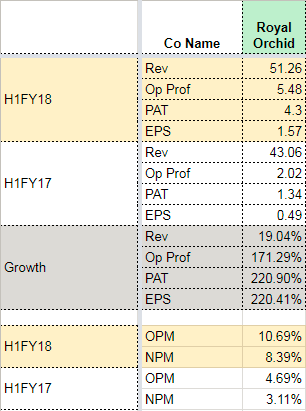

Discussion Financial Result of 2nd quarter of 2018 and first half of financial year 2017-18

o This half year company had done very good job comparing previous year. Market also turnaround.

o Company has done Growth of 22% in revenue in Current quarter and in profit company growth was 52 %.since last year.

o Last year this quarter occupancy ratio was 58 % now it is has grown substantially to 76-77 %.

o On this year company has 42 hotel, last year total room counted was 3269 and company expecting to cross 50 hotels in this financial year .

o Today it is the 11th largest hotel in the country in terms of room now.

o Company is targeting very good growth in future also however debt is very much in control .

Q&A

Could you help me to understand the strategic partnership between your company and UK based hotels , How it will work?

o This is a group of around 240 hotels where we they will marketing our hotels and we here will market there hotels . So this is not a partnership it is more a marketing strategy that will help us in future for increasing occupancy.

How will the demand is setting up in current quarter and help us in understanding the ARR trend rate for the last quarter and how you will setting up in current quarter ?

o Company was having 3400 rooms last year and 3500 rooms this year so the ARR movement is small however there is a substantial movement in Occupancy. So there is far difference between ARR and Occupancy ratio . These two quarter are seasonal for Hospitality sector so there will be better results.

Can you help us understanding Management contract business and what kind of revenue and profitability we generate from management contract business this quarter ?

o In management contract business we got revenue of 3 Crore this quarter and same quarter of last year it was almost 2.70 Crores whereas company cost was stagnant . We have seen substantial growth in EBITDA margin QOQ it increase 24 % and half yearly 21 %.

What kind of room addition we are targeting for the current and next year ?

o This year company already have 3269 and there will be addition of about 3-4 hotels this year adding 300 rooms this year. Next year company is targeting about more than 1000 rooms.

Did company has certified certain property ?

o Around 700 rooms has been identified on which we are working and remaining are in pipeline as there is lot of negotiation going on.

o Now people are coming to us for managing their hotels , earlier company was going to them so management contract business is very critical and it will shoot on .

Kindly update us about your situation of land in Tanzania ?

o Company has taken out land for sale but right now there is not much movement there. Real estate in India as well as globally is slow down and we are more optimistic about selling our Bombay property. We hope we will get the right buyer and efforts are going on for both the land.

o This year company should crack it as far as Mumbai is concern . We are very hopeful that this year it will materialise .

Standalone turnover has gone up by 20 % over 20% ,the cost line has also move up in similar range 19-20 %.while the bottom line has perform very well the cost line has moved in a single way nature , Could you understand me how this costline will behave in the next few quarters ?

o A new law of minimum wages came so we had to implement that . So that hit the cost.

o Second reason was we have to keep our hotel well managed for a better performance. Some of the hotels in Maharashtra the electricity cost has gone up the rate has been increased by the government.

o Third reason was we had done some servicing in some of the hotels in last month

o So that’s why you are seeing increasing the cost. But going forward there will not be such substantial increase in cost. Going forward the cost trend will be 7-10 % only.

How your subsidy property in Jaipur and Goa had performed, and are we now growing at the consistent basis the PBT level ?

o There is a very good trend on the consolidation basis also , EBITDA grown 15 % on consolidated basis. In the current quarter itself we have done break even.

o First quarter there was a loss and we have done a consolidated profit in current quarter itself. We had also recruit some of the loss that we had done in first quarter. Going Forward also we will be in consolidated profit .

In this quarter we have a stand alone EBITDA of say for 6.5 Crores . So what was the consolidated EBIDTA now we are clocking on this quarter ?

o On standalone the EBITDA was 6.8 Crores and on consolidate it is around 7.98 Crores for current quarter. For half yearly it is around 12.5 Crore on consolidated bases last year it was 8 Crores .

Did we have reduce some debt or we are still same ?

o Yes debt has come down and on consolidated bases it has come down very much and we are focus on it reducing the debt burden only.

What we will do from the money that we will generate from selling Tanzania land , Did we use it for Debt repayment or utilisation of it ?

o We have to take opportunity if it does not come then we will pay debt and become debt free company. In the radar right now nothing but if it happen then yes .

Can we assume that revenue from the land will be above 100 Cr ?

o No it is not like that we are expecting nearly 50-53 Crore from the Bombay property and the market are not very active but we are hopeful to get at least that much.

What about Tanzania land valuation ?

o I have to go there and meet some prospect investors and then I will be able to answer that .

In some large cities does the post GST sales has impacted how is the RSC prices for the prospects ?

o Most of our hotels are in 7.5 % bracket Our earlier rate of tax was 21.5 % now the rate of tax is 18 %

o We are giving RSC prices including GST prices

o We get GST input credit itself

o Most of our rates are below 7,500 brackets.

In terms of ARR in terms of corporate side can u give that ?

o We have not seen that much improvement in the ARR and reason for this is many of foreign traveller are decreasing in our hotel . So tie up with Uk hotels will help us to Cater that and may be we will see some valuable results and get out of them.

What is the reason for the increase in debtors days and how wold you see it going forward, it was 33 days and now it 50 days ?

o Debtors days will be in the range of 30-35 days only . This happens because of main flow of business always happen in December only so debtors day is more right now but September month was very good for us so you will see it decreasing again in the coming quarter.

Can you give break up of rates of own hotels versus management contract hotels, How is your arrangement in the management fee percentage ?

o Complete breakup is given in investor presentation. ARR of our owned hotels is 3800 rs and ARR of managed hotels is 2800 rs. Sharing percent is normaly 2-3% of turnover and 6-8% of the gross operating profit as management fees from this companies.

How you see demand supply in some of the key markets like Bangalore , etc where we are operating ?

o There has been exposure of supply in most of the markets in india for the last few years.

o For the last two year the supply has slow down whereas demand has gone up.

o So we do expect there will be more demand and supply coming future years. So when boom will come people wake up setting up their hotels but it take 3-4 years to setting up an hotel in India. So we do expect bull run in the next 2-3 years. In the hospitality industry in India.

o In Bangalore there has been robust demand going us because of it good environment and people love to be here you can see huge development going on in Bangalore as airport is developing very well by adding phase-2 and phase-3 as well

Out of total business how much does we get form platform like Make my trip and Ibibo, how much we get directly and indirectly coming from these platforms ?

o Normally from our OTS we are getting 20-25% of business and rest Makemytrip and Go ibibo enjoy large share . May be 2/3 business come from these platforms and balance will come from other OTS. Balance business we get from Corporates which is large share of business we have offices across the country , we do have chains these contribute substantial amount of business. Then RSP where we have contract with business also give good business and our loyalty program we have lot of repeat time along that. So that is how we get our business.

Corporates would be above 50 % of the business for us ?

o 70-75% would be leisure business and remain 20-25 % would be corporate and other way round from city hotels.

What can be the maximum occupancy ratio we can reach as combined Because in the regional hotels we have week days and there is a little slag in the business hotels. So what is the highest occupancy we can see from here on ?

o In leisure hotels occupancy of 70-75 % can be achievable whereas in business hotels 75-80 % can be achievable . So I think we are very much there now.

Is this same case with other competitors ?

o See this report has been published by independent agency and we are ahead of our competitor at many places . We monitor it on regular basis.

As we are already at 75-80% occupancy so what will be the ARR you are expecting now ?

o We do expect 10 % growth rate in the next half year and 10 % in next year so that should continue.

Booking season is going on so howz this season going on ?

o Booking going on good, Now what happen is people are booking in the last minute itself . So last minute booking has expand very substantially rather then in advance.

What kind of marketing revenue we are targeting in coming year ?

o It is more of visibility so I would not able to answer it too early . This will impact our Leisure property and there is a huge demand in India for leisure property. So I am not much optimistic from this , it is just a platform form which we both get commission from each and other.

Are you open for any JV (Joint Venture) for small hotels in India to make it a bigger group , Is there something like that ?

o We are open for opportunities but right now there is no such plan ready.

You had mention of decrease in interest rates in previous concall so does it happen and could you give me the figures ?

o Yes one of our loan was at interest rate of 13.5 % that as come down to 8.5 %. Other two loans which we have in Jaipur and Bangalore we are in urge of declining interest rates by 2 % there also which will impact in coming quarter. We had also get better ratings from banks for paying loan on time.

What does really change the environment and this turnaround happens. Do you see this sustainable or is this for short term ?

o The golden years were 2006 and 2008 and probably that will never come back and at the same time industry has gone through a very very long cycle from 2008 to 2017 because of recession at that time you see one after another market was collapsing but India has domestic market also So our property has done well. Our Goa property has get very much business from Mumbai and Delhi and there is huge demand and today in India people are spending to going out . At the time of Lehman crises amny more crises also done and this hotel industry was doing expansion at pre post Lehman crises . We also trap in the debt So our revenue at that time come to 100 Crores from 380 Crores . So we had also sold our one hotel at Hyderabad and we have the guts to take that step and save the company. Today the hotels where debt is huge and repayment time is short term that will face crises. So whole picture get played we get debt we get 10 years of repayment and debt repayment is the major turnaround of the company so of course the industry is having demand even at that time hotel cost has gone up but in our case our cost has not gone up we have tight control on cost. In management contract business also many companies have come and gone but we still survive and we will because of our cost control.

Do you see margins in upward moving trend or still the same as we are ?

o Of course in upward trend you had seen in our first quarter was not so good second quarter is better and coming quarter will be much better then previous one.

Any big impact of GST ?

o No there is no big impact of GST may be in two properties there were two or three cancellation of wedding because they were not having cash and we have to pay cash to all arrangements that we do . GST has done positive impact on our business not negative impact.

We have a Five star property at Jaipur How this property has performed in the first half ? We have two land parcels right now one is at Mumbai other is as Tanzania , Is there any piece on the block which will help us in business ?

o Last year Jaipur first half Jaipur property revenue was 8.35 Crores this year it is 9.90 Crores So there is a substantial growth in the revenue as far as the EBITDA is concern last year EBITDA was 1.62 Crores this year it is 2.72 Crores So there is substantial improvement in the EBITDA also. But ARR has not gone up they are flat because of occupancy we have seen growth in EBITDA. There are no land piece on block only two are there that you told .

If we talk about the last cycle this might be premature but What was the typical learning from your past cycle and there will be typical flow of capital in the industry how you see capital allocation in the company ?

o Earlier what happen in our company was bank were giving only short term loans on this industry which we have we get 8 year loan as the Jaipur hotel we get 8 year loan and a Hotel takes 3 year to build that means your repayment start before the revenue coming. So you are already in the financial stressful situation. Now what happen that government has realised that it is not going to work because it take 3 year to build and 2 year to be stable So now the loan are coming from the banks are 15 year loan so your get long repayment period. So now things are changing and there is a very good opportunity in the metro cities and we will operate in asset light model company .

When you talk about previous experience and future expectance what kind of ARR you look at ?

o Normally in the past we have seen 7 % increase in ARR over a period. And that Lehman crises cant be predictable so now we have moved on a very linear line and now company will not get in that past situation again so we are optimistic on ARR .

Are we looking at leasing our assets ?

o Yes we don’t mind if any good opportunity come we will lease our assets. We have disscussions going on for leasing but nothing now for disclosure.

Participant seems to be very low what are the reasons right now and going forward what is going to change to improve the metrics ?

o In asset light there are fix cost like management cost of the company you have certain fix cost which are mainly staff and marketing and this take some time to break even which has happen now. So from now whatever management contract we are going to sign the revenue from that will be going to quarter nine So cost will only increase step wise when you add in hotels and to hire someone to take care of that hotel Otherwise for one or two hotel vice-president itself take care of it.

You said that we will see 10 % capital utilisation this year and another 10 % in next year and we are adding about 300-400 rooms this year and another 1000 rooms next year so are you including tax in the capital utilisation ?

o We are not going to do capital utilisation these are going through management contract only .