Change of Chairman’s post

Mr Chandrakant Gupta replaced by his son.

Change of Chairman’s post

Route mobile CEO said in an interview/news article dated 30 Nov that they are eyeing 2 acquisitions in the areas of conversational AI and a virtual contact centre (with due diligence underway). articles says that they are expected to be in range of 250-300 cr valuation and will be a mix of cash and stock.

I see many mobile based apps are using biometrics based authentication. Current example of apps which im usind like Paytm, Kotak securities, citi bank.

This will reduce the volume for OTP based authentications for players like Route. Views are invited

A good article to understand business model of ROUTE MOBILE.

Ravi Dharmashi of Valuequest superb presentation on Route Mobile at IIC 2020.

Edelwiss Coverage Route Mobile - Initiating Coverage - EDEL - Dec-20.pdf (1.5 MB)

Technical experts on this topic, kindly guide on how this may affect Route Mobile business in future?

Route Mobile is the first Asian player to go live with clients for RCS messaging - HDFC Bank and Motilal Oswal. It is also in discussions with HDFC Life for the same…

Latest Investor presentation for Sinch in case someone would like to understand competition and sector better.

https://investors.sinch.com/static-files/4edcc778-5c11-4fbe-abfb-2b10041e9f24

Can be compared and contrasted with RMs presentation

Thank you @kkarimyusuf for this comparison.

I am copy-pasting the 6 month charts of both Synch and RM

It is astounding to see the clear correlation between these two !

This implies that one clearly needs to have a global perspective to get a more wholistic assessment on route mobile ( I guess it is obvious, but this chart really highlights this obvious point)

@Admins : Please delete this post if the chart is not allowed on this thread.

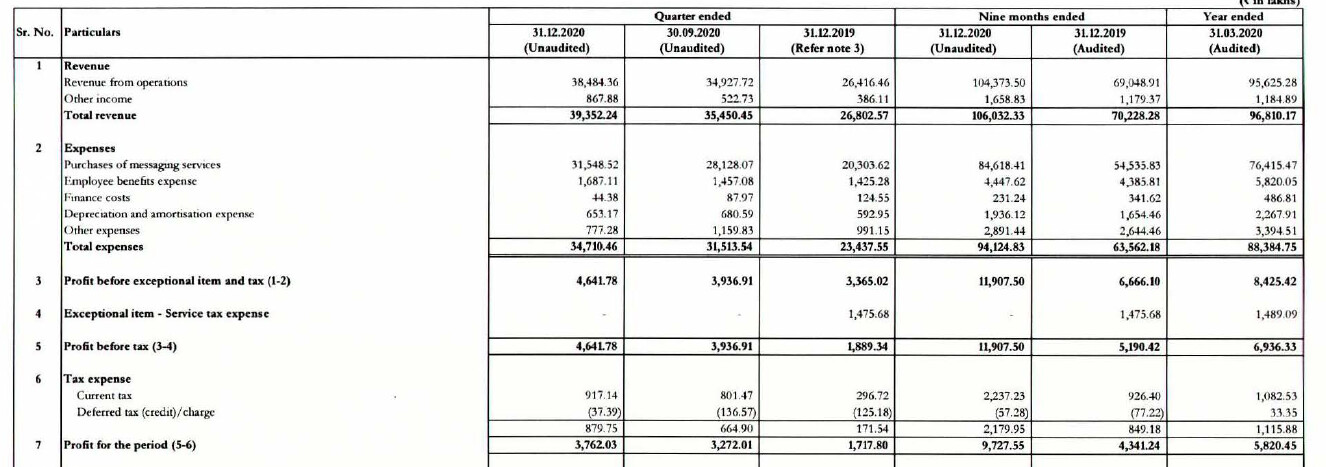

**3Q great set of numbers. At this rate company should be able to do upwards of 134crs in FY21. **

Stock at P/E of 52x FY21 v/s Tanla at 28x v/s Affle 96x and Indiamart at 82x

Missed the concall today. Any notes which can be shared?

Disc: Invested

can we listed to the recorded concall webcast?

Please find the link for the Conf Call for Route Mobile Q3 Results-

Few notes

a. Integration with Apple Business Chat is in process and will be completed in next few months

b. Solution for Whatsapp, Viber, Telegram is already in place. (Will need to see the usecases)

c. 1-2 Acquisitions are in pipeline for Customer Experience as a Service(Will need to see the use cases)

d. Margins will expand with the integration with OTT solutions like Whatsapp, Viber, Telegram compared to SMS platform

e. DTT charges were waived off for few Enterprise customers for this quarter. It will be charged from next quarter

very informative, helpful. thanks!

Recent interview by the CEO on bloomberg quint.

Highlights :

Disc: Invested

I think management is talking about 25-30% or over 30% Gross margin and not EBIDTA margin.

So margin profile will change from ~20% to 30%

While most notes are captured, trying to get key margin drivers as Q3 it was below topline growth

All in all lots of positive triggers lined up

Mgmt kept pushing the point that heading to CXaaS( customer exp as a service), from Current CPaaS.

As long as operating leverage is reflected in nos with decent topline growth - good story to play. Q3 was a miss on margins but Q4 will be key.

Invested.

My notes from the Q3 call (attended partly) and had to leave midway owing to work constraints

Drop in operating margins YoY owing to 2 issues

o DLT issue – did not pass on the DLT charges cost to clients. Benefits of which should accrue in due course as per the mgmt…

o Some clients in UK impacted owing to lockdown.

Decision of not passing on DLT charges: Helped win a few new clients already. These clients to whom they didn’t pass on the charges in Q3 are willing to pay DLT charges this qtr onwards. Intimation was on short notice in Q3

Company is bullish about RCS and on a lot of new networks adopting RCS in near future.

Mgmt has been eyeing couple of companies for inorganic growth opportunities – likely to be product and technology benefit led acquisitions. Announcement likely to happen soon

Next generation products in the pipeline include MIDaaS (Mobile Identity as a Service), GBM (Google Business Messaging)

o MIDaaS can help address SIM swapping issue

On Sinch completing acquisition of ACL Mobile: Doesn’t imply an increase in competitive intensity for Route

9M free cash flow (unaudited): 190 Cr. Cash on books (unaudited): 440 Cr

@nityanandparab - Believe you have updated the link for Q2 call.

Disc : Invested