PE has two sides.

Highe PE is generally considered only due to price increasing beyond logical limit.

But there is a denominator too. High PE is also due to temporary decrease in earnings due to many temporary reasons. So We first needs to find out if high PE is due to increase in price or due to decrease in earnings. And if its due to decrease in earnings, then we have to analyse if its temporary decrease or business model is crumbling. With this understanding, can you verify whether above High PE are pertaining to which reasons?

5 Likes

I agree that in some cases PE is high due to temporary phenomenon such as margin contraction or consumer slowdown.

What triggered above post is while I was going through the list of companies in my watchlist that can be considered as good quality business, in most cases valuation seems to be stretched. I don’t mind paying extra premium for quality but even after that I don’t feel confident enough.

For example last year I have taken shelter under PSU due to better MOS and dividend while growing at fair rate, I thought looking into IT as it is underperforming for a while but no companies available at under 20 PE in that case as well.

Again I know PE is not the only parameter but in case such as IT PE and Div yield is usually a good indicator when you can consider adding them in portfolio and what worries me, as I mentioned in the above post, is that people are becoming very confident about paying a 70 PE for businesses like Kalyan Jewellers

For example, in case of LTI mindtree , PE is 39 but if its earnings arr depressed from last 2-3 quarters compared to earlier period, then Its PE is not reflecting the correct picture. May be real PE is less than 20 but due to depressed earnings ,its showing 39. Just check its earnings compared to earlier periods and PEs too

Thank @Mudit.Kushalvardhan for your inputs and I completely agree with your points.

LTI, MapMyIndia and even Affle in IT, Varun bev in FMCG, Polycab in cables and few other companies are growing and that justifies the PE.

Again PE was included because it is an easier parameter to gauge compared to sales/mcap and opportunity size etc.

It’s just that the increasing number of IPOs, QIPs, and the overall market mood, where almost everything is priced to perfection, coupled with very high returns in Mid/Small caps, worries me a bit.

I understand that it’s difficult to time the market, which is why I’m not selling my existing positions. However, currently, I am a bit cautious about adding new positions with very high conviction, so for now, I won’t add anything all at once

1 Like

Hi

There are so many cos that are cheaper and growing at good rates than what you have mentioned. I will just share 3 examples from my own folio where trailing PE is <15 and last 3-year EPS growth was >15%. Now I dont know what next 3-year growth will look like.

Godfrey Phillips: 14x and 22% growth

Chamanlal Setia: 10x and 31% growth

Geekay wire: 12x and 59% growth

If you just run this query on screener you will find 426 results. So there are plenty of opportunities, the only question then is if you are looking at the right place.

Good luck with your investing journey and do share you ideas ![]()

Cheers

Harsh

11 Likes

Thank you so much @harsh.beria93 for your input, I love your portfolio’s thread and keep looking for ideas from there.

Got interested in Rice companies as there are mainly 3-4 major brands out there and most of those trading at reasonable valuations. Yes, I am looking at Chamanlal and KRBL (aware about CG issues)

Just going slow and reading more companies in detail. I can stay invested only if I have enough confidence in my holdings and feel confident about it.

2 Likes

What about LT foods? Its numbers are better than KRBL and seems better placed as major business is exports. Just one query: Reason for fall from Rs.90 to Rs.19 between Jan 2018 to Aug 2019? What happened during this time to have such a steep fall? Also ROCE is less than 20…But at 15 and increasing trend.

Yes looking into it.

Apart from all the information available on valuepickr, if we do Dupont analysis to summarize

- KRBL operates at higher margin

- Chamanlal has better efficiency

- LT foods uses financial leverage better

LT foods and Chamanlal trading almost at ATH while KRBL is ~ half compared to ATH due to CG issue.

Not able to understand lower valuations for these companies in spite of strong brand and higher market share.

Still not convinced though to take position in any of these but tracking it closely

1 Like

Update – Jun’24

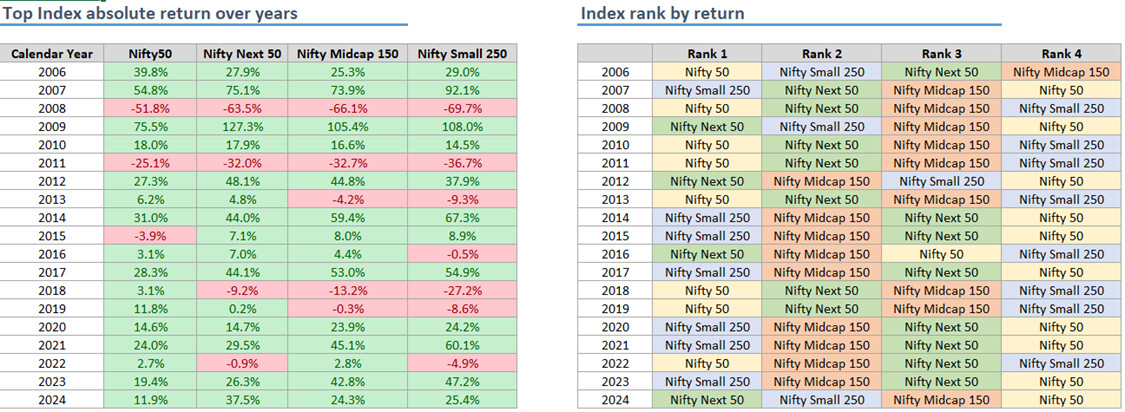

Nifty is still positive, but its performance has lagged in four out of the last five years. All other indexes have given returns of more than 25% in most recent years

Looking at some other data :

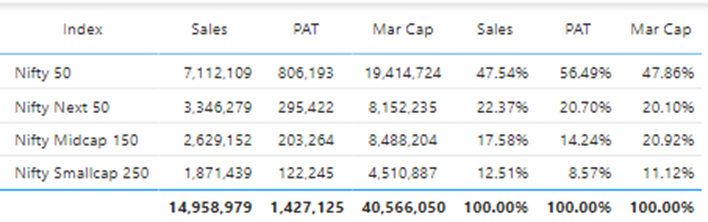

If we consider the top 500 companies, Nifty’s contribution to PAT is 56.49%, but its share in market capitalization is 47.86%. The midcap segment looks stretched, followed by the small cap segment.

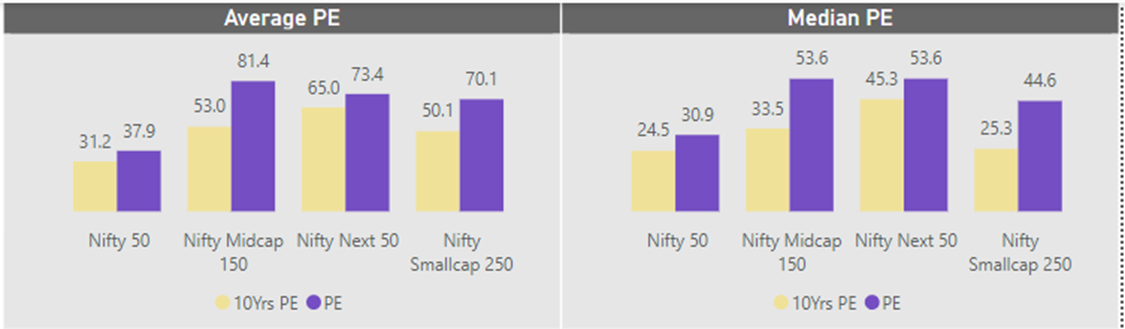

From the perspective of PE, midcap and small cap are again higher compared to their historical PE. If we consider the median PE, it is 53.6 for midcap and next 50, whereas it is 44.6 for small cap.

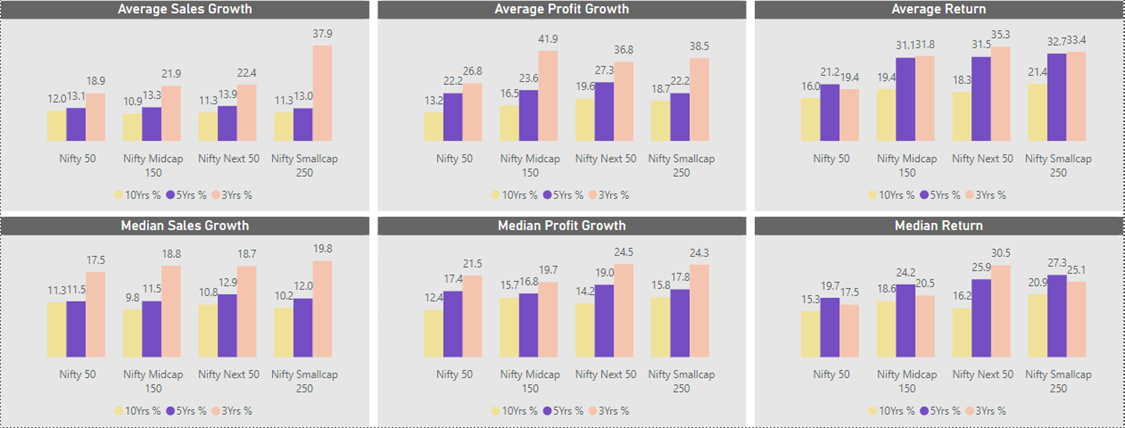

Now looking PE with growth

Growth has been better in recent times, leading to higher PE ratios. However, Nifty has mirrored the return of growth. Therefore, Nifty offers better prospects compared to other indexes when considering both growth and valuation.

Allocation :

| Category | Percentage |

|---|---|

| Stock | 21% |

| Equity MF | 12% |

| Debt MF | 42% |

| FD | 6% |

| Gold | 3% |

| Cash | 4% |

| Other | 13% |

I wanted to go a bit defensive, so I am almost out of Next 50, Mid and Small cap.

I sold all mutual funds except Nifty 50 and PPFAS Flexi Cap, and for now, I’ve parked the money in a debt fund

Equity Portfolio:

| Invested Price | Current Price | Allocation | ||

|---|---|---|---|---|

| 1 | NSE:ITC | 240 | 434 | 16% |

| 2 | NSE:HDFCLIFE | 567 | 607 | 13% |

| 3 | NSE:ICICIGI | 1,243 | 1,860 | 16% |

| 4 | NSE:HDFCAMC | 2,082 | 4,221 | 12% |

| 5 | NSE:KOTAKBANK | 1,757 | 1,845 | 10% |

| 6 | NSE:MUTHOOTFIN | 1,017 | 1,803 | 4% |

| 7 | NSE:SUNDARMFIN | 2,336 | 4,587 | 4% |

| 8 | NSE:NAM-INDIA | 273 | 661 | 4% |

| 9 | NSE:CDSL | 1,026 | 2,319 | 4% |

| 10 | NSE:JYOTHYLAB | 231 | 472 | 3% |

| 11 | NSE:GLS | 699 | 911 | 3% |

| 12 | NSE:CMSINFO | 398 | 521 | 3% |

| 13 | NSE:HCLTECH | 1,385 | 1,517 | 6% |

| 14 | NSE:BIKAJI | 552 | 708 | 2% |

| 15 | NSE:BECTORFOOD | 1,281 | 1,432 | 2% |

Average up in core portfolio where some stocks corrected during election result day.

Added:

Glenmark life science :

Business : High ROE and ROCE business

Growth : Decent growth of 14% in the last 3 years

Valuation : ~8k market cap and 15 PE with 3.5% div yield

Balance Sheet : No debt and 2.4K reserves

Holding : Promoters holding ~82%, with individual shareholders decreasing over the years

CMS Info :

Growing topline ~15% and bottom line ~29%

Decent margin of more than 25%

Very good management, growing in different areas and focusing on service

Trading at a reasonable valuation of 17PE, 6k Mcap, growing steadily. Lower valuation due to concern around the cash management business as cash in the economy is reducing

Hangover of promotor sale is over, now owned completely by institutions, showing strength in the market and not correcting much.

HCL Tech:

Short to Medium term bet.

Usually, when a stock reaches ~3.5-4% div yield, It offers reasonable safety and decent returns.

Bikaji :

Added as part of core portfolio, with plans to add more going forward.

Plan to add FMCG, IT to the portfolio as it is heavily tilted towards financials.

Preference for packaged food is increasing, and Bikaji has a good portfolio expanding into various categories.

Like the management as they are targeting slow and steady growth, with possibilities to enter into QSR space like Haldiram.

At more than 50 PE, it looks a bit expensive. But added at 7 times to sales. Given the long runway, I am okay to pay more and will add in small tranches.

Mrs bector:

Almost similar thesis as Bikaji

Exit:

Amara Raja : Booked profit in Amara Raja, technically it is poised very well. But honestly, I don’t understand the business in detail. I have no idea whether it will win in the battery wars. I added because of safety when the price was around 600.

I needed to raise some cash, so I sold it as I want to hold businesses where I have confidence and better understanding of the business.

Did some transaction in between but kept on profit booking and added it into core portfolio.

Mistake :

Exited from some stocks too early such as Cochin Shipyard, Rites, REC etc. Those were bets keeping in mind of margin of safety and Div yield. Booked profit after ~2x but I had no clue back then how crazy things could go. Again , I don’t have too much regret of it as those were the short/medium terms bet as replacement of FD.

What worked:

Even after booking profits here and there, I managed to stay in the market and build a core portfolio.

Plan for next half of the year:

After COVID, all we have observed is that buying ignored stocks will eventually lead to gains. We have not seen any sizable correction. Many promoters are selling out, the quality of IPOs coming to market is questionable, and relatives are calling me saying they are investing in power/manufacturing funds. These are a few things that keep me cautious for now

I would like to invest more in stocks/MF to the existing portfolio, but as I said earlier, I will add Mid/small cap when there is a broader correction in the market. Untill then, the plan is to be in Large cap and Debt fund. And keep taking small bets in between.

At the end thank you so much everyone for all your guidance and support.

@harsh.beria93 @basumallick @hitesh2710 @Donald @ranvir @hardik_shah1 @Investor_No_1 love hearing your thoughts on this forum.

and special thanks to @ayushmit for screener, being focused more on quantitative side, getting all these data through screener is just awesome.

7 Likes

DSP has launched ‘Nifty Top 10 Equal weight Index fund’, I am planning to move more into large cap though I would prefer holding most of my holdings, may be I’ll move incremental money into this fund.

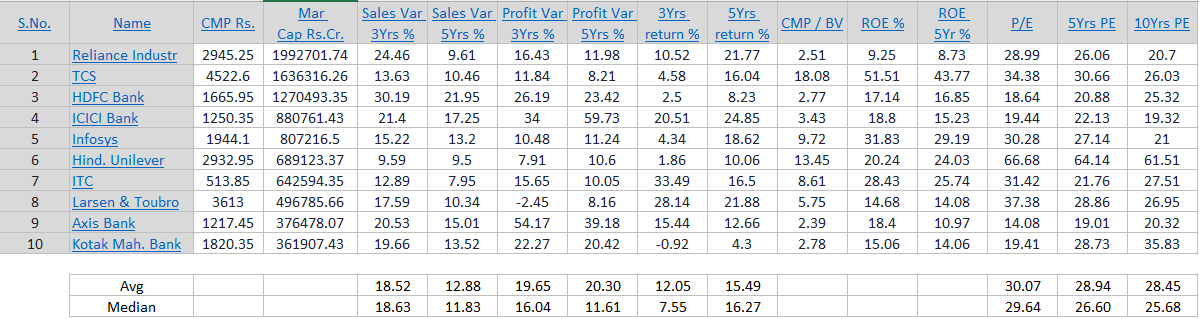

A very quick summary of key metrics of 10 stocks (Using Screener.in).

In terms of last 3 years, returns are lower compared to earning though PE is a bit on higher side compared to long term trend

1 Like

Update – Dec’24

Nifty is set to end on a positive note for the 9th straight year, and if we ignore the minor negative return in 2015, there has been no significant correction since 2011.

Allocation :

| Percentage | |

|---|---|

| Stock | 20% |

| Equity MF | 16% |

| Debt MF | 33% |

| FD | 7% |

| Gold | 4% |

| Cash | 3% |

| HANGSENG ETF | 2% |

| Other | 14% |

| Total | 100% |

*Other is NPS and PPF investment.

No major shift in overall allocation but within equity I have moved more towards large cap. Added more gold and Hangseng etf in portfolio.

Equity Portfolio :

| Sr. No | Ticker | Invested Price | Current Price | Allocation |

|---|---|---|---|---|

| 1 | NSE:ITC | 240 | 471 | 17% |

| 2 | NSE:ICICIGI | 1,272 | 1,990 | 15% |

| 3 | NSE:HDFCLIFE | 585 | 633 | 17% |

| 4 | NSE:HDFCAMC | 2,082 | 4,528 | 12% |

| 5 | NSE:KOTAKBANK | 1,758 | 1,805 | 9% |

| 6 | NSE:NAM-INDIA | 273 | 773 | 5% |

| 7 | NSE:BECTORFOOD | 1,315 | 1,785 | 3% |

| 8 | NSE:CMSINFO | 408 | 533 | 3% |

| 9 | NSE:JYOTHYLAB | 268 | 414 | 3% |

| 10 | NSE:GLS | 699 | 1,019 | 2% |

| 11 | NSE:GODREJAGRO | 806 | 770 | 3% |

| 12 | NSE:BIKAJI | 552 | 800 | 2% |

| 13 | NSE:ACC | 2,129 | 2,247 | 2% |

| 14 | NSE:KRBL | 279 | 310 | 2% |

| 15 | NSE:AARTISURF | 648 | 653 | 2% |

| 16 | NSE:LTIM | 5,663 | 6,717 | 1% |

No major changes in core portfolio:

Exit:

Sundaram Finance

No issues with the company, I wanted to reduce midcap exposure in my portfolio. Sold it ~4950, it was trading at ~5P/B, which is much higher than its median P/B of ~3. The stock had more than doubled with relatively low volatility. I’d love to add it again in the future if it corrects further.

Muthoot Finance

The thesis is almost similar to Sundaram, though it is still trading around its historical P/B. I needed to book profits in mid and small caps and move toward large caps.

CDSL

Capital market-related stocks have been performing well. The stock had almost tripled for me. While it was part of my core portfolio, I wasn’t entirely sure about my decision to sell. Generally, you would want to stick with your winners, and I didn’t have a strong reason to book profits. However, I thought it was a good idea to take some profits with the stock trading at over 60 PE, especially when the market is at an all-time high.

Addition :

ACC

Adani is serious about the cement business and aims to take the top position from Birla. ACC is available at a valuation of 44k crore, with 27k crore in reserves and trading at ~21 PE. Adani is expanding capacity and implementing backward integration, which should help improve margins. Key mutual fund managers have been increasing their stakes quarter-on-quarter.

Godrej Agro

To be honest, I don’t understand the business in detail, but it appears to be a value buy. The stock has crossed its 3-year high after being an underperformer for a long time, delivering almost no returns in the last 6 years. However, sales have doubled, the company is profitable, and promoters, FIIs, and DIIs are increasing their stakes. ACC and Godrej Agrovet replace Sundaram and Muthoot, where I expect decent returns with minimal downside.

Other

We know the reasons why KRBL is trading at a low valuation. If the management can turn around its Saudi business or build a good market for value-added products, the stock has the potential to deliver reasonable returns.

I have made a very small allocation to Aarti Surfactants. Again, I don’t understand the business in detail, but it is part of a big group and is a profit-generating company. It has the potential to grow significantly in the future.

Strategy:

I am still underinvested in equity, and within my equity allocation, I am moving toward large caps.

- Added DSP Top 10 Equal Weight Fund (discussed in an earlier post).

- Increased my gold allocation by adding Gold ETFs (since SGBs are not available at a discounted rate).

- Added the Nippon HANGSENG Index ETF as a speculative punt on China. The returns have been almost nil over the last 5 years. I’m aware of the issues associated with it, but recently investors such as Vijay Kedia and Shankar Sharma is talking about it.

Strategy going forward:

I will continue my SIP in index mutual funds, preferring large caps. Any additional funds will be allocated to debt, gold, and the Hang Seng ETF. I will start adding mid and small caps from my watchlist once they become available at reasonable valuations.

2 Likes

A quick update after almost a quarter:

Moved money from debt mutual funds to increase allocation in equity mutual funds and gold. Simplified my mutual fund investments by selling all mid and small-cap funds in January and reallocating almost everything into large-cap funds.

Through this process, I realized that I don’t want to frequently shift allocations in mutual funds over time. Instead, I prefer a consistent investment approach, making large-cap and flexi-cap funds more suitable for me.

| Percentage | |

|---|---|

| Stock | 20.77% |

| Equity MF | 23.96% |

| Debt MF | 21.44% |

| FD | 7.66% |

| Gold | 6.07% |

| Cash | 3.20% |

| HANGSENG ETF | 2.13% |

| Other | 14.79% |

| Total | 100.00% |

- Other is NPS and PPF

Current Mutual Fund Allocation

I am now allocating equal amounts to the following funds:

- HDFC Nifty 50 Index Fund

- Zerodha Large & Midcap 250 Fund

- PPFAS Flexi Cap Fund

- SBI Focused Fund – I like the fund manager’s style and the concentrated portfolio of a maximum of 30 stocks with international exposure. It has a long track record.

- Old Bridge Flexi Cap Fund – This will be my only small-cap exposure. I trust Kenneth Andrade’s expertise, as he invests in only 23-25 businesses, avoiding new-age high-growth stocks, IPOs and financials. Since I don’t have the skills to execute such a strategy myself, I am relying on his experience.

Equity Portfolio Updates

- No major changes in my equity portfolio.

- Booked profits in Glenmark Life Sciences.

- Increased allocation to all existing stocks, mainly NAM-India and CMS Info.

- Still not finding any major new opportunities, so I’m sticking with the stocks already in my portfolio.

Performance & Strategy for the Next Few Months

- Selling mid and small-cap funds and moving into gold and Hang Seng worked well for me.

- DSP Top 100, Nifty 50 Index, and PPFAS were my largest holdings, and they performed relatively well during this downturn.

- Increased my equity allocation by 8% in February and March compared to December last year.

- No further investments in gold, as I have already bought some physical gold and consider my exposure sufficient.

- Not in a hurry to go aggressive in stocks or equity mutual funds. I’ll continue my SIP. I will continue allocating small amounts during major dips. If no good opportunities arise, I will increase my debt mutual fund allocation.

3 Likes

Update – Jun’25

Result Update for FY25:

Midcap and Smallcap stocks still have a higher share of market cap compared to their share of profits.

Median valuations (P/E) remain elevated compared to historical averages, especially for Mid and Smallcaps relative to Largecaps.

When viewed in conjunction with profit growth, the median 3-year return is higher than profit growth across all indices , and the gap is wider for Mid and Smallcaps compared to Largecaps.

Portfolio Allocation:

| Allocation | |

|---|---|

| Stock | 20% |

| Equity MF | 24% |

| Debt MF | 24% |

| FD | 8% |

| Gold | 7% |

| HANGSENG ETF | 2% |

| Cash | 0% |

| Other | 15% |

| Total | 100% |

*Other is NPS and PPF

**Gold is Gold plus minor allocation in Silver

No major shift, but I moved some money from debt mutual funds to equity mutual funds at the start of the year during the correction, and booked profits in direct equity, mainly mid and small-cap stocks.

Equity Portfolio:

| Sr No | Ticker | Invested Price | Current Price | Allocation |

|---|---|---|---|---|

| 1 | NSE:ITC | 232 | 417 | 16% |

| 2 | NSE:HDFCLIFE | 587 | 778 | 19% |

| 3 | NSE:ICICIGI | 1,272 | 1,963 | 16% |

| 4 | NSE:HDFCAMC | 2,082 | 4,964 | 13% |

| 5 | NSE:KOTAKBANK | 1,758 | 2,171 | 10% |

| 6 | NSE:NAM-INDIA | 405 | 762 | 8% |

| 7 | NSE:JYOTHYLAB | 277 | 320 | 3% |

| 8 | NSE:CMSINFO | 412 | 478 | 3% |

| 9 | NSE:AARTISURF | 636 | 548 | 1% |

| 10 | NSE:KRBL | 277 | 344 | 3% |

| 11 | NSE:ACC | 2,042 | 1,822 | 3% |

| 12 | NSE:DALBHARAT | 1,784 | 2,038 | 2% |

| 13 | NSE:SBILIFE | 1,416 | 1,811 | 3% |

Over a 3-year time frame, I’m seeing decent outperformance against the Nifty 50 and Nifty 500 indices.

Though I’m not actively tracking it, my approach is simple: trying to invest in good companies with a long runway and reasonable valuations.

- No major change in the core portfolio, but I have further reduced exposure to mid and small caps.

- Booked profits in GLS, Bikaji, Mrs. Bectors, and LTIM. I want to reduce direct allocation to mid and small caps , valuation is the only reason for exiting these stocks.

- Added SBI Life, similar thesis as HDFC Life , and it was available at a very reasonable valuation (~2.42x price to IEV).

- To increase allocation to the cement sector, which is currently being ignored, I have added Dalmia Bharat.

Equity MF:

| Mutual Fund | Allocation |

|---|---|

| HDFC Nifty 50 Index Fund - Direct Plan | 44% |

| Zerodha Nifty LargeMidcap 250 Index Fund - Direct Plan - Growth option | 10% |

| SBI FOCUSED EQUITY FUND - DIRECT PLAN -GROWTH | 9% |

| Parag Parikh Flexi Cap Fund - Direct Plan - Growth | 27% |

| Old Bridge Focused Equity Fund - Direct Growth | 11% |

I will slowly rebalance it over time so that they end up having equal weightage.

Strategy for next few months:

- Not in a hurry to go aggressive in stocks or equity mutual funds. I’ll continue my SIP.

- I will continue allocating small amounts during major dips. If no good opportunities arise, I will increase my debt mutual fund allocation.

- In the long term, I plan to invest more in mid and small caps, as I already have a decent allocation to large caps through mutual funds. I’ll do this once valuations become reasonable.

1 Like

Sir rationale for choosing Dalmia bharat over others? Can you share your thought process?

I want to invest in businesses with decent capacity.

Dalmia’s cement capacity is ~49.5 MnT, which has doubled over the last 8 years and is now at par with Shree Cement, yet it is available at one-third of the market cap.

The company has maintained stable EBITDA per tonne over the years.

It has reserves of around ₹17,000 crore, while its market cap stands at ₹38,000 crore.

Punit Dalmia appears to be a capable promoter, with an educational background from IIT and IIM.

On top of all this, DI are increasing their stake, especially many fund managers I admire hold this stock in their portfolios.

Update – Dec’25

- Nifty is set to end on a positive note for the 10th straight year, and if we ignore the minor negative return in 2015, there has been no significant correction since 2011.

- Small caps are getting into interesting territory. Although the index is down only 6.4%, the damage is quite visible at the stock level. Many stocks have corrected by more than 50%, which has also been highlighted by Siddharth Bhaiya in the latest newsletter.

Portfolio Allocation:

| Dec’25 Allocation | Jun’25 Allocation | |

|---|---|---|

| Stock | 18% | 20% |

| Equity MF | 14% | 26% |

| Debt MF | 29% | 24% |

| FD | 8% | 8% |

| Gold | 9% | 7% |

| Cash | 6% | 0% |

| Other | 16% | 15% |

| Total | 100.00% | 100.00% |

- It has been a good year largely because of asset allocation. I booked profits in HNGSNGBEES and MAHKTECH ETF as they were trading at a 25 - 40% premium at one point. I also booked profits in Silver as it appreciated quickly and my target was achieved. Additionally, I sold some direct stocks and mutual funds to concentrate my holdings.

- Due to recent reshuffling and profit booking, equity exposure has reduced further, while cash, gold, and debt allocations have increased.

Equity Portfolio:

| Sr No | Ticker | Inv | Price | Allocation |

|---|---|---|---|---|

| 1 | NSE:ITC | 241 | 405 | 15% |

| 2 | NSE:HDFCLIFE | 587 | 748 | 16% |

| 3 | NSE:ICICIGI | 1,272 | 1,953 | 14% |

| 4 | NSE:HDFCAMC | 1,041 | 2,647 | 12% |

| 5 | NSE:KOTAKBANK | 1,758 | 2,162 | 9% |

| 6 | NSE:NAM-INDIA | 405 | 870 | 8% |

| 7 | NSE:CMSINFO | 399 | 345 | 3% |

| 8 | NSE:AARTISURF | 623 | 392 | 1% |

| 9 | NSE:ACC | 2,042 | 1,736 | 2% |

| 10 | NSE:SBILIFE | 1,416 | 2,017 | 3% |

| 11 | NSE:INDIAMART | 2,433 | 2,215 | 2% |

| 12 | NSE:SULA | 260 | 228 | 2% |

| 13 | NSE:UDS | 259 | 196 | 1% |

| 14 | NSE:CYIENT | 1,177 | 1,118 | 2% |

| 15 | NSE:URBANCO | 172 | 128 | 2% |

| 16 | NSE:HATSUN | 1,024 | 970 | 1% |

| 17 | NSE:ORKLAINDIA | 674 | 604 | 3% |

| 18 | NSE:BECTORFOOD | 244 | 237 | 1% |

| 19 | Jyoti Resin | 1,134 | 1,114 | 1% |

No major changes in the core portfolio, but I have started adding a few small caps. Hence, the tail looks longer than usual.

Over a 3-year time frame, I’m seeing decent outperformance against the Nifty 50 and Nifty 500 indices.

Exit

KRBL

- Invested as a short term bet to park some money when the margin of safety was high. Booked profits after corporate governance concerns and the real estate investment announcement.

Dalmia Bharat

- Invested as a short term opportunity when the margin of safety in the cement sector looked attractive. Booked profits as I want to focus only on high conviction businesses.

Jyothy Labs

- Exited as part of portfolio reshuffling to make room for more FMCG names and faster growing categories.

Addition :

Hatsun, Mrs. Bectors, Orkla India

FMCG has been ignored for some time, and valuations have cooled off a bit. These are defensive small-cap plays with strong brands.

Orkla India

- Pros: Strong brands, unorganized-to-organized shift, export opportunity, clean balance sheet, strong parentage

- Cons: Competitive market and slowing growth; numbers may be inflated for a few years post listing

- Invested as a play for nominal growth along with dividends over time.

Mrs. Bectors

- Re entered after correction. The investment thesis remains unchanged. It also acts as a proxy to QSR growth, with investments in new facilities and decent growth visibility.

Hatsun

- On my watchlist for a long time. Strong management and brands. Premiumization is driving growth. The stock has not corrected much and is showing relative strength.

All these FMCG bets are long term holdings, with an expectation of low double digit returns and relative stability.

Other Key Holdings

Cyient

- IT is currently out of favour. Cyient is led by strong promoters and has corrected nearly 50% from the top. It is now available at reasonable valuations with a decent dividend yield.

- Growth remains a concern, and recent acquisitions have not yet delivered results.

- Cyient Semiconductors provides optionality.

- At ~21 PE and ~2.3% dividend yield, I expect low double digit returns with a reasonable margin of safety.

IndiaMART

- Unlike the above, this is a faster growth bet. The company generates strong cash flows and is deploying capital into acquisitions.

- Mr. Dinesh Agarwal is actively involved and well known in the startup ecosystem. This resembles an Info Edge like model, where the core business funds optionality bets.

- After initial euphoria, the stock corrected due to MSME concerns and now trades at ~24 PE, despite profits nearly doubling over the last four years.

Low-Conviction / Optional Bets

Sula Vineyards, Updater Services (UDS), Urban Company

These are small positions and not high-conviction bets for me. I may exit them over time.

Sula

- A category creator, but growth is slow and the market size is limited. Management has acknowledged that returns may take time.

- Regulatory challenges persist, and the cash conversion cycle is high.

- On the positive side, brand strength, wine tourism, and promoter involvement offer some comfort. After correction, it trades at ~₹1,900 crore market cap with ~₹560 crore in sales.

Updater Services

- Invested based on qualitative parameters. Business growth is good, valuation was attractive at ~12 PE, with no debt and decent ROCE.

- However, recent auditor feedback has raised concerns, and I may exit.

Urban Company

- Solves a real consumer problem and enjoys category leadership. Strong brand recall and expansion into new categories like water purifiers. Entry was immediately post listing; in hindsight, patience would have helped. Holding a small position for now.

Equity Mutual Funds

- I generally avoid frequent reshuffling in mutual funds and continue SIPs. However, I consolidated holdings this time.

- Exited Nifty 50 and Zerodha LargeMidcap 250 and replaced them with Zerodha Multi Asset Passive FoF to consolidate passive exposure and gain indirect exposure to gold and debt.

- Exited SBI Focused Fund due to discomfort with recent strategy (Adani exposure and IPO participation like Lenskart). Now holding only three equity funds.

| Sr no | Mutual Fund | Allocation | Comment |

|---|---|---|---|

| 1 | Zerodha Multi Asset Passive FoF - Direct - Growth | 14% | Will increase allocation through STP and reinvest my previous index fund’s amount |

| 2 | Parag Parikh Flexi Cap Fund - Direct Plan - Growth | 53% | |

| 3 | Old Bridge Focused Fund - Direct Growth | 33% |

Strategy Going Forward

- No changes to core holdings

- Portfolio will continue to be dominated by debt funds (mainly PPFAS Dynamic Asset and HDFC Corporate Bond Fund)

- Gradually increase equity exposure via SIPs and STPs, no rush to deploy lump sums

- Focus on selective small-cap additions

- No further gold purchases, adequate allocation already, plus indirect exposure via the multi asset fund

Finally, thank you very much for all the guidance and support through the ValuePickr platform @harsh.beria93 @basumallick @hitesh2710 @Donald @ranvir @Pragnesh @Worldlywiseinvestors . Wishing you a wonderful New Year and continued success.

7 Likes