I had a doubt regarding the use of Return on Capital (Non-BFSI). What does it really say about the business?

Shouldn’t we focus on cash efficiency rather than book value capital efficiency?

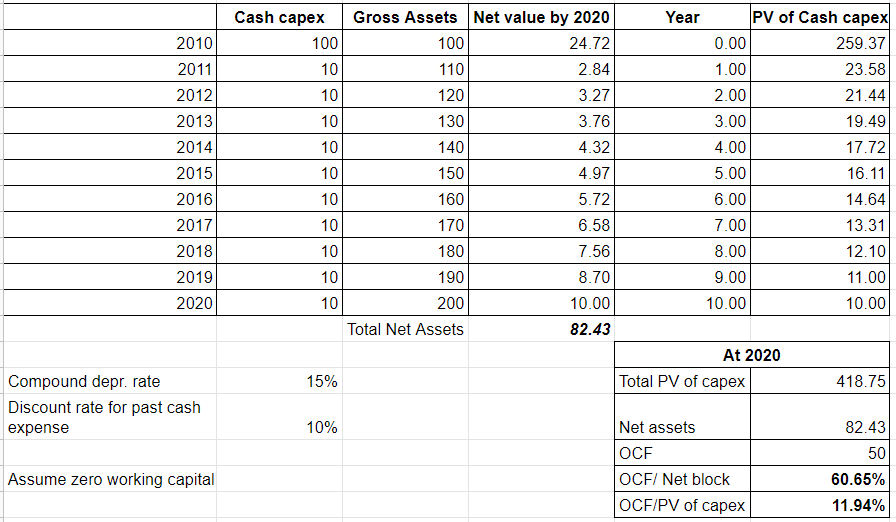

For eg.

Company A does a capex worth 100 in 2010. Every year, it does a maintenance capex of 10 from 2011 till 2020. Assume the compounded depreciation is 15%.

Assume Zero/Negative working capital.

Let’s say the operating cash flow for the year 2020 is 50.

Also, I have considered the time value of past cash expenses by bringing them to Present Value by an interest of 10%. (I don’t know why we usually don’t consider this)

At 2020, the Net Assets come to Rs 82. Considering OCF of 2020 for simplicity, the Return on Capital is 60%.

At 2020, the PV of Cash expenses comes to Rs 419. Considering OCF of 2020, the cash yield is 12%.

Think of it as a simple business (Assets financed by Shareholders Funds and Retained earnings); no debt(For simplicity assume Current Assets = Current Liabilities and ignore them altogether)

Now focus on what Cash Yield gives you; It provides a return rate, for this year, on total cash you have burned (#invested) in the company. It is more of an economic term than a financial one. It essentially compares the return on the money that year vs investing it anywhere else (think of it as opportunity cost of your money; depending on your risk If you had invested the same amount of money in mutual funds yielding 12% for the last 10 years, at 11.94% this year (2020) you are at par; if you would have otherwise invested in corporate bonds at 8%, you have gained significantly)

With me till here… Here is the deal; without knowing the OCF of business for the remaining last 9 years, I have no clue whether the investment was a wise one or not. All I can say with absolute certainty is that this year was on par with MFs. So Cash yield has very little correlation to business performance unless I know it for the whole 10 years.

Coming to ROCE, which is the returns on capital employed, in this case of our simple business with no debt, all the capital deployed in the business would be by the equity holder, a.k.a you. As a equity holder you would use retained earnings or your own funds to deploy capital (doesn’t matter since both are equity holder’s money, so for the sake of simplicity we assume it is a new firm, entirely financed by share capital).

Now coming to the firm in question; you would notice that this firm is adding 10 in capital investment (replacement capex each year); and the depreciation is 15%. So for the first year you were operating with INR 100 of Assets, the second year with INR 100 - 15 + 10 = INR 95 of assets and so on and so forth with Net assets decreasing every year. If the firm was able to maintain the same level OCF (leaving aside the complexities of removing incremental capex from OCF) in the last 10 years, your ROCE would have increased from 50% in 2010 to 60% in 2020.

But an ROCE of 60% is exceptional you would say. Not true, cyclical firms or trading firms with low asset base can show exceptional ROCE in a year and then be under the weather for next decade. If predictable business like FMCG, FMIG, Consumer durables show this characteristic, it is a great business indicator. Even then you would have to take in account broader economic conditions to make sense of fluctuating ROCE numbers. With the complex financials many companies have including multiple layers of financing, wildly fluctuating CA/CL and varying incremental capex the process can be daunting, but worth it.

Regarding ROCE all I can say with certainty is that everything else remaining same (or reasonably same, make what you will of it); an improving ROCE shows better business output in terms in that year on year you are making more bang for your buck.

I think you’ve got either the calculations wrong or the concept wrong. You have actually calculated the ‘FV of Cash Capex’, not ‘PV of Cash Capex’. Be that as it may, how can you compare the sum of all the FV of Cash Capex against the OCF of only a single year (The final year)? What happened to the OCF for all the 10 years prior? What about the FV of OCF for all the 10 years?

If you still want to do this convoluted method of calculation, this is the correct formula:

Yield = Sum (FV of OCF for all 10 years)/Sum (FV of Cash Capex for all 10 years)

If you want to do it on a single year basis, it would be:

Yield = OCF (2020) / Net Assets (2020)

The sole problem with Operating Profits to Operating Cash Flow conversion is Working Capital. Since you have assumed no Working Capital, Operating Profits = Operating Cash Flow and both Profit Yield and OCF Yield should be the same. The other component is Taxes, which should anyway be reduced from both Profits and OCF, unless there are Deferred Tax / Unpaid Tax, which will increase/decrease OCF by that amount.

The problem I find with using ROCE(or ROE) especially for bulky capex done periodically is that post the bulky capex, let’s say 5 years down the line, the equity component reduces drastically due to accumulated depreciation of 5 years and that inflates the ROCE/ROEs.

What I intended by this is that how much worth of cash in today’s value (2020 in this case) have I spent till now for the past 10 years. I may have got the terms wrong.

Don’t we measure yields annually?

This is the main culprit. Let’s tweak this example a bit so that I can understand it better. Let’s do a capex of Rs 100 today and the nature of the capex is such that it will give positive cash flows only after year 5 (I still produce and sell stuff at zero working capital but I don’t have margins initially.)

After 5 years from capex, I get an OCF of Rs 20. My net assets have come down to 50 due to annual depreciation of Rs 10.

My return on capital for that year is 40%.

My cash yield would be 20/(the cost of doing that capex today) = 20/160

= 12.5% (considering 10% cost of capital)

That is the nature of Capex. It’s exactly like investing. It is giving up money now to earn more money in the future. So if you measure returns at the time you gave up money and at the time you are getting most of it back, the results will be very different. Looking at a single year’s RoCE or any return figure would be misleading.

Yes, so then that would be a terrible Capex which didn’t produce anything for 4 years. That one Capex you should not have done at all. Of course, I’m saying this generally but it ultimately depends on the sum of PV of ALL cash flows produced from that specific Capex.

Yes, and that disconnect is because you are using a Capex that is capable of producing cash flows for many years in the future, but only considering the cash flow of a single year to measure returns.

Usually a large Capex happens once in 7 or 10 years. That is the only time returns will get distorted. Otherwise over time, even measuring a single year’s RoCE / returns should not be a problem. You may read this document written by Varadha ji on similar lines: