Thanks for sharing your views, Naman! I agree with you on many points. I am trying to develop a better understanding of this company.

Could you share the mistakes made by Mahindra EPC and Jain Irrigation? Infact, it would be interesting to know why did Mahindra acquire the company. Please share if you have some knowledge of this.

Have you heard if the promoters plan to move the company to the main board (NSE)? After 3 years of IPO, there isn’t any compulsory market making for shares on SME exchanges and then most of the stocks hardly trade. I am concerned that the shares may become almost untradable if the company does not migrate on the board (NSE).

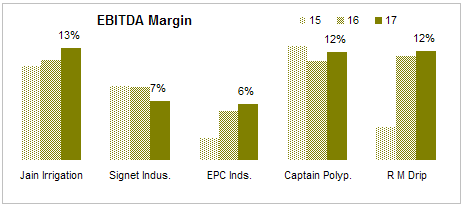

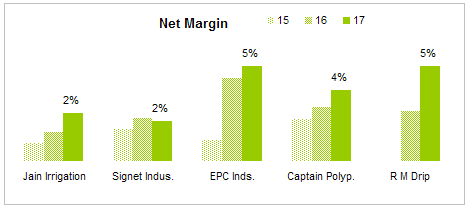

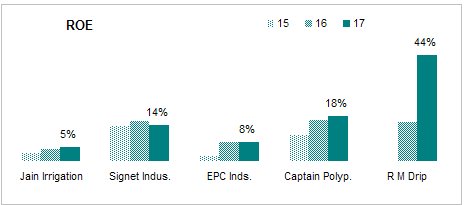

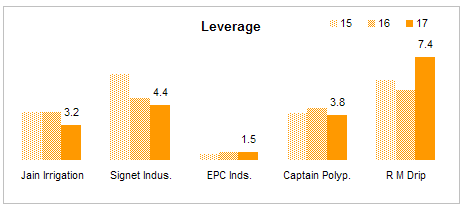

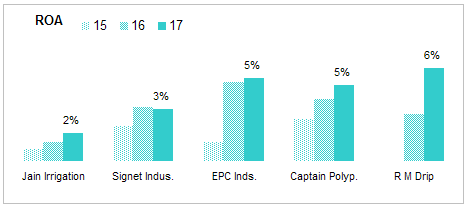

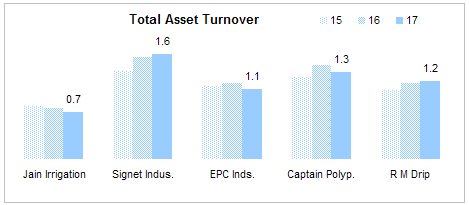

I just looked at financials of Captain Polyplast. Their net margins have been in the range of 2.5% to 3.5% for the previous three years, which I consider to be low. So, all major companies (Jain, Mahindra, Captain) seem to be working on low profit margins for like forever. The low profit margins in this industry would imply that Return on Equity would be high only at high amounts of financial leverage. Over long periods, this strategy would prove to be risky, especially for the smaller firms.

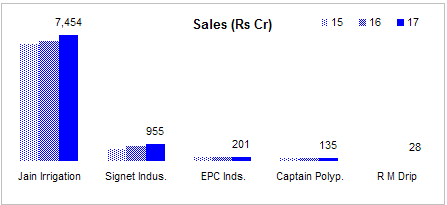

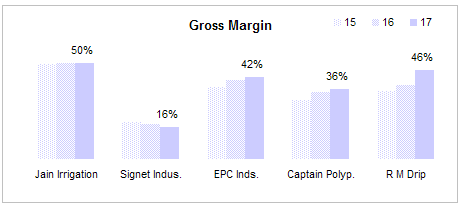

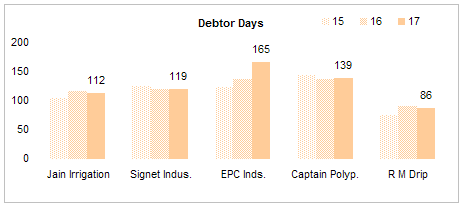

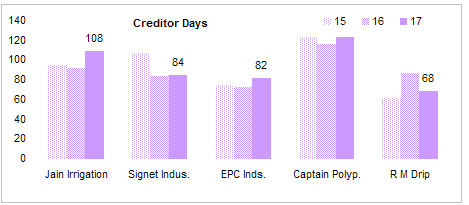

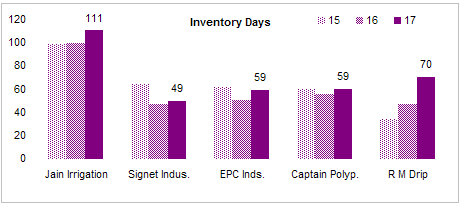

Intrestingly, the interest cost for Captain Polyplast is ~7 crs, but the total debt is only ~20 crs. The effective interest cost comes out to be 35%, which is too high. I did not delve any deeper. I was concerned that they could be underreporting debt by managing it down temporarily at the time of reporting of the balance sheet. The financials of Captain Polyplast made me think why is it that the material cost of RM Drips has been lower by 15% of revenues when compared to Captain Polyplast. Infact, the Material Cost / Revenues of RM Drips is lower than the bigger brand names like Mahindra too. It is not clear as to how they are selling at a much lower price than the bigger names. They must be selling at substantially lower prices since they have doubled their revenues once again in FY17 while others (Jain, Mahindra, Captain) have reported a marginal decline.

Also, the P&L statements suggest that the price of raw material has fallen over the previous 2 years and the benefits of about 10% to 15% have been retained by the manufacturers. If the prices increase by 10% now, then it would wipe out all the profits if the increased costs are not passed on to the customers. Even if one large player decides to absorb the cost increase to garner market share, then other competitors would find it difficult to pass on the cost increase.

The company seems to be growing fast and the operating leverage can help generate fabulous returns for the investors. But, the doubts seem to persist in my head.

Views/Criticism solicited!