I appreciate the rules of the Forum. The company came to my notice when I was looking for companies in Technical Textiles field. Appears that the company is in right industry and if they can execute the plans well, we may see decent appreciation in share price which is currently less than Rs.30

I found the following positives about the company

Management change:Yes new MD since 2012;

Industry tailwind: Yes belongs to technical textiles;

Quality products. Yes 20% exports and marque clients like Asian Paints Kansai Nerolac, JK White, Jain Irrigation etc. in domestic market;

Share holding: management stake increased; about 21% is held by small investors;

High ROCE: more than 28%;

Growth rate: more than 30%

Low equity: 57.98 lakh shares

Valuation: about 20 crore.

Trend. Appreciated more than 100 % since Mar 2016 The negatives noticed about the company are

Low volumes and could be difficult entering and exiting the stock

No dividend paid after 1998, hope fully this may change once cash flows improve

Not much is known about the promoters.

All the above information is taken from publicly available sources.

This is the copy of the post I placed in Emmbi Industries thread on 5 November. Since it is relevant here I am reproducing my post.

“Recently I was listening to the first quarter earning call transcript of

Emmbi Industries. The CEO was referring to the vast opportunity and the

high growth rates being enjoyed by the companies in technical textiles

industries. This prompted me to look for some well placed companies in

the sector, apart from EMMBI. I came across two very interesting

companies belonging to two different segments of technical textiles, One

is Fiberweb India Ltd, which has recently come out of BIFR. The company

has wiped out all the accumulated losses after settlement with the

creditors. It has informed the exchanges that production upto March 2017

is already booked. As large orders are being received beyond the

available capacity, the company has taken some facilities on lease. I

could not verify the trustworthiness of promoters. Hope that no issues

were there on that count.

Another interesting company I came across was Rishi Techtex.

Promoters:

The CEO was at the helm of affairs for about two years. Since then

there was marked improvement in financial parameters including ROE/ROCE.

The negative aspect I noticed was low promoter stake. However,

promoters have increased their stake over the years.

Products: The

company is mainly into packaging and agriculture related products.

Company claims that it is market leader with 50% market share in agri

nets with KRISHINET brand. It exports about 20% of its production.

Presence of exports gives confidence about the quality and market

leadership gives pricing power to the company. The industry is at

nascent stage and a long way to go. Market cap of the company is less

than 25 crore leaving lot of scope for appreciation. As i could not find

a separate thread for these companies I posted here as all these

companies belong to technical textiles industry. I hope I am not

violating any guidelines. I have invested about 2% of my portfolio in

these stocks and my views may be biased. Invite comments of the fellow

boarders. Thank you.”

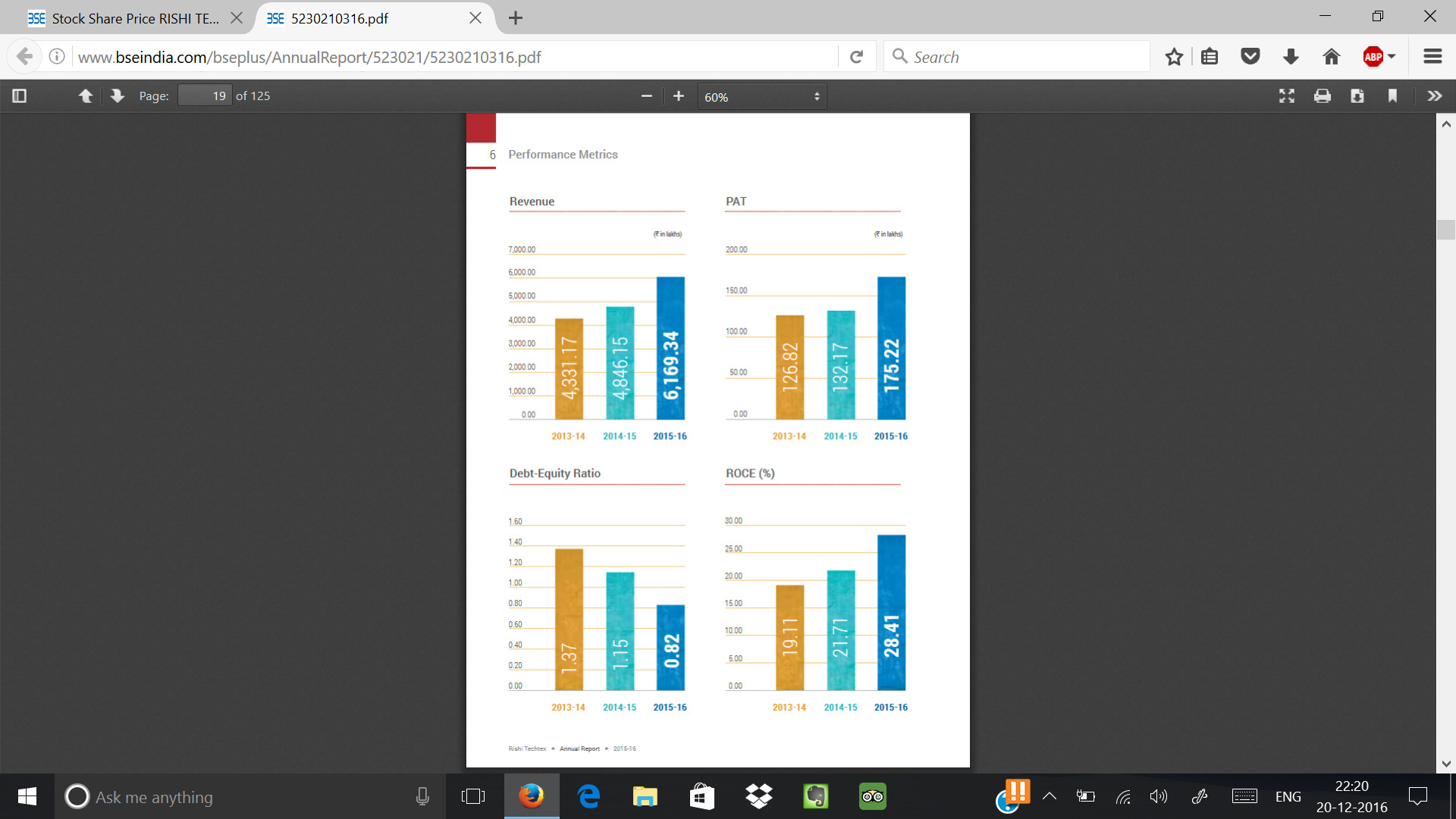

The company also has taken approval in AGM for issue of 10 lakh shares to non-promoters through private placement at Rs.22 per share for meeting working capital requirements. This issue and conversion of warrants will increase the total shares to 73.91 lakhs. Though there is equity dilution by about 27%, the benefits of availability of working capital may be visible in the subsequent quarters. The September quarter was a bit disappointing on revenue front but the profitability was increased which is a welcome sign. The flat revenue Q on Q may be due to seasonality and reduction in material cost. The year on year figures are pretty impressive. Going by the optimism shown in the statements in AR, 2016-17 figures should be pretty good. As the Industry is at nascent stage and is growing, next few years should be good for the company. The company has increased sales from Rs.43.31 crore in 2013-14 to Rs.61.69 crore in 2015-16, the profits have increased from Rs.1.27 crore to R.1.75 crore and the debt equity ratio was reduced from 1.37 to 0.82 . This has improved the ROCE from 19.11% to 28.41% during the above period. In the six moths FY 2016 the profits are up by 38% and the Balance Sheet is improving. If the company can perform this way the market cap of the company which is at just Rs.21.40 crore (on fully diluted equity) can improve substantially. Consistent performance for a few quarters changes the perception about the company and generate interest among investors. Declaration of dividend will go a long way in bringing credibility to the numbers. I hope that these things will play out over next few quarters and years. However, we need to keep a watch on the developments. The low liquidity in the stock is to be kept in view while taking investment decision.

The promoter integrity and trust worthiness are the issues to be kept in view, I did not find any adverse reports in this regard.

Comments and constructive criticism will help in bringing out any adverse issues which are not visible apparently and are welcome.

The ROCE figures are taken from the Annual Report of the company for 2015-16. I think it has to be EBIT/Capital Employed and the company might have taken average capital employed. The screen shot of the relevant of page in Annual Report is posted below:

The company has run up too fast in too little a time. Though I am nuatral on the company at present valuation, I exited the company to accomodate another company with better ratios i.e. Vivid Global on which I have more conviction and I do not want to increase the number of small caps in the portfolio. Since I am the initiator of the thread I thought I should disclose this.

Although the sales and net profit of RISHI Techtex is increasing, still the ROE is less. Further, the company is also reporting regular profits, but not paying out tax or dividends. I will suggest to study the stock carefully before investing.

I did attend the AGM on 20th of September. I did have a discussion with MD. I was extremely impressed with his down to earth and candid approach.

Key highlights of my discussion with Mr. Abhishek Patel:

Current Business:

No complex products being made by the company

They have a niche in a commoditized business

PP/HDP is the main raw material used

There are only few organized players

Huge awareness need to be created about technical textiles

Response to the customer needs are very important

Trying to move up the value chain and produce high margin products

Bags are low margin high volume product

Agri will have slow growth, about 5% every year as awareness need to be spread

Product mix: Shednet -50% Packaging – 50%

They have BIS certification from Shadenet

Wall putty needs a special packaging

Company’s focus for future:

Marketing is the main thrust area for the company currently.

High margin products are the focus. Efficiency has improved significantly compared to the past.

At present Gujarat is the main market.

New dealers are being appointed

They are expanding in East India for further growth.

High Interest loans:

Current loan is at a high interest rate. Working on bringing it down by 3-4% by this year end.

Expansion Plans:

All capex done. No expansion plan as of now

Capacity utilization is only 65%. Don’t need capex for next 18-24 months for the current growth.

Will lease out land for further expansion when needed.

Competition:

Two major competitors are Tuff ropes/Tuflex.

Fishnet from Garware is very good

R&D :

3 members R&D team currently which will be increased to 6

One agriculture scientist will be added

Mostly Textile Engineer/Chemical Engineer hired for R&D job.

One patent is in progress. The idea is to ensure the organized players away from producing the patented products.

Misc:

Chinese machinery is the cheapest and German machine is the costliest (5 times). German machine is un-viable in India.

China has huge capacity in technical textiles. Each of their six factories is almost equivalent to the entire production in India.

No direct conflict with Rishi(others) group although they share the same office

Open for foreign collaboration

DeMo and GST impact:

Demonetization has impacted the company in a big way. Most of the purchases used to happen in cash by farmers.

GST also had big impact on the company. It is still going to be few quarters before things get back to normal.

Post GST their products have tough competition in export market especially the gulf countries

Disc: Invested. No trading in last one month. I might have missed or misinterpreted some of the points. Please take them as just a broader discussion point.

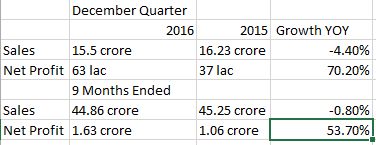

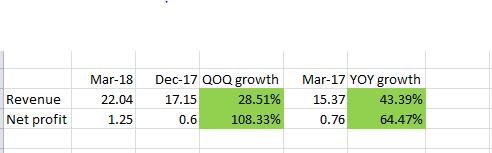

It was a flat year.

The borrowings have jumped from 7.4 cr to 12.41 cr. There is also a note from auditors and the management clarification regarding a trade receivable of 3.91 crores.