Apart from Microsoft and Mubadala, Twitter is also reportedly in talks with Jio.

https://www.nytimes.com/reuters/2020/05/28/business/28reuters-reliance-investment.html?partner=IFTTT

Apart from Microsoft and Mubadala, Twitter is also reportedly in talks with Jio.

https://www.nytimes.com/reuters/2020/05/28/business/28reuters-reliance-investment.html?partner=IFTTT

Reliance is selling the PPEs to the government at around ₹650 per piece. This is a significant drop from the nearly ₹2,000 per piece import cost that the nation was incurring earlier.

RIL is using high grade polypropylene to produce the equipment lending it more opacity while keeping it light weight. In addition, Ethylene Oxide is added to the material for improved sterilization. The material and manufacturing processes follow the ISO and BIS standards acceptable in India.

Although under paywall, this is a lovely article on reliance with a vivid description of its history.

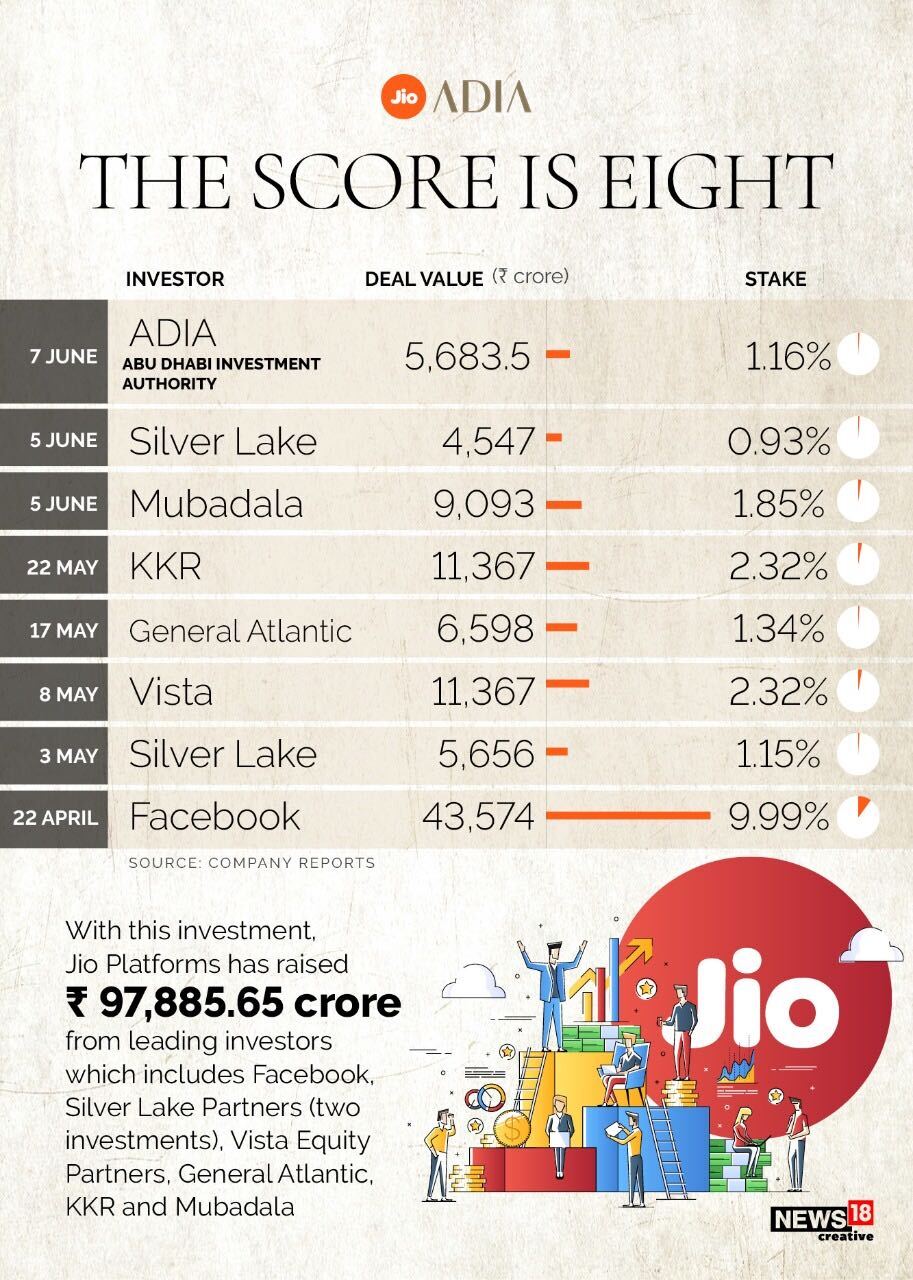

It will give them 1.85 per cent stake in Jio Platforms.

Mubadala owns electronic chip manufacturing company Global Foundries and has stake in several technology companies like AMD.

It has an investment portfolio across several fields, including petroleum, renewable energy, aerospace, satellite communications, agriculture, healthcare, metals and mining.

Commenting on the aggregate investment brought by Silver Lake, Mukesh Ambani, chairman and managing director, Reliance Industries Ltd, said Silver Lake and its co-investors are valued partners as his company continues to grow and transform the Indian digital ecosystem for the benefit of all Indians. “We are pleased to have their confidence and support, as well as the benefit of their leadership in global technology investing and their valued network of relationships, as we drive the Indian Digital Society’s transformation. I would like to emphasise that Silver Lake’s additional investment in Jio Platforms, within a span of five weeks during the COVID-19 pandemic, is a strong endorsement of the intrinsic resilience of the Indian economy, which will surely grow bigger with comprehensive digital enablement.”

Reliance Industries said on Sunday it has received its eighth investment for Jio Platforms with the Abu Dhabi Investment Authority (ADIA) signing up to buy 1.16 per cent stake for an investment of Rs 5,683.50 crore.

“I am delighted that ADIA, with its track record of more than four decades of successful long-term value investing across the world, is partnering with Jio Platforms in its mission to take India to digital leadership and generate inclusive growth opportunities. This investment is a strong endorsement of our strategy and India’s potential," said chairman and MD Mukesh Ambani.

Reliance Jio is subsidiary of RIL, hence no dilution of RIL on account of these sale… This is some what unlocking the value for RIL shareholders…

The rights offer of RIL is dilution but again it is for shareholders only… The way it was subscribed, it speaks about immense faith of shareholders in the business…

Going forward Digital and Retail can be value accreditation for RIL shareholders…

“Key challenge has been around the delivery as covid-19 has created issues on delivery fulfillment as well as timeline,” said Jefferies India Pvt Ltd in a report dated 8 June, wherein its channel checks indicated that JioMart ordering via Whatsapp has stopped in the past two weeks. Jefferies India added that most retailers have been informed by Reliance Retail that operations will start soon and the shutdown is only temporary.

With curiosity, I placed orders through jiomart website to different addresses - one in a state capital and the other a district headquarter. In both cases, partial refunds are given citing non availability of products. Delivery was delayed.

During the same period, Amazon Pantry which was serving only in state capital has also started delivering in district hq. Amazon Pantry is making inroads into small towns silently while the Jio-Mart is going gung ho in the media and utterly failing to win the customer confidence.

What I think personally is, Jio-Mart is a new entrant in retail and should be given time to optimise efficiency.

OTOH, Amazon has been operating in India over a decade and hence in a stronger position.

Comparing Jio-Mart in it’s infant stage to a bulwark of Amazon isn’t fair to be fair.

I remember when Amazon started, many products weren’t available in BIMARU States and many products didn’t have COD, where Flipkart had a stronger foothold. Things have completely changed now.

With all the hype and gush of investments, what I find fascinating is the total lack of discussion among the pundits about the execution risks around the so called tech platform that apparently everyone wants to buy into. RIL has shown no indications yet of any sustained innovation - something that is very dearly needed if one is indeed valuing Jio as a digital company.

What has RIL succeeded at so far? - Building and monetizing heavy asset plays, one needs capital to start any of the businesses that RIL has gotten into after senior Ambani made it big. Rich promoters usually tend to invest into businesses where capital is an entry barrier, you rarely see them getting into segments where innovation and agility are more important than access to capital. For a rich man capital is easier to access than to build capabilities and skills that they do not have.

However once the digital infra is built, monetizing that and cementing value proposition while competing with new age ideas is a different ballgame and calls for a different set of skills. This is where one sees the innovation culture across the new age companies that are dominating the online/digital space today. These businesses call for promoters to hire smart people and to give them a free run to express themselves, rather than concentrating all power and decision making with the promoter. Becoming a tech giant is not easy, it is a different game compared to the one RIL has been playing over the years.

I have the highest regard for RIL’s vision and ability to think and dream big. Execution however needs to be finely evaluated before one hops onto the bandwagon basis pure possibilities. All these large PE’s have no other option but to back such behemoths since it is not easy to deploy money at such scale in India, we retail investors on the other hand do not have that problem. We can take our time, evaluate progress and then hop on rather than trying to be too early in the game like a PE who just does not have the luxury of nibbling once in a while.

Zygo I usually like your deeply informed takes on VP but I couldn’t disagree with you more here.

0 - While you say jumping on the bandwagon and wait for execution, an investor into RIL gets all the businesses and not just Jio and RIL is valued at the same level today as it was before these transactions happened and the media attention on Jio surged.

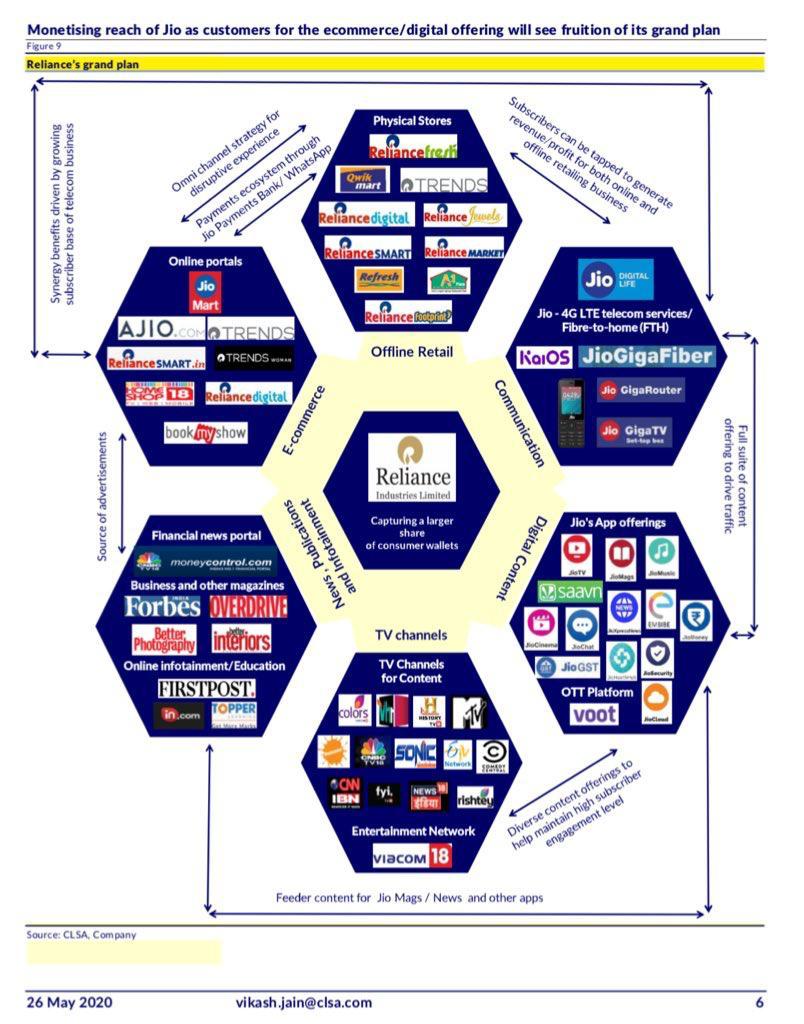

1 - The tech platform is not some castle in the sky - this already exists within Reliance. One can debate about the quality of their apps but I personally find Saavn, Moneycontrol, BookMyShow and MyJio the best in their categories in India already.

The graphic below is a good representation of the existing ecosystem and possible synergies

2 - The Whatsapp - JioMart partnership will clearly leverage the strengths of Reliance on execution (huge Reliance retail network plus kiranas already signed up with Jio POS). The front end may be through WhatsApp or a standalone Jio app but this is a small part of the puzzle - one doesn’t use Amazon or Flipkart because their apps are great but because of pricing, product selection, service quality etc.

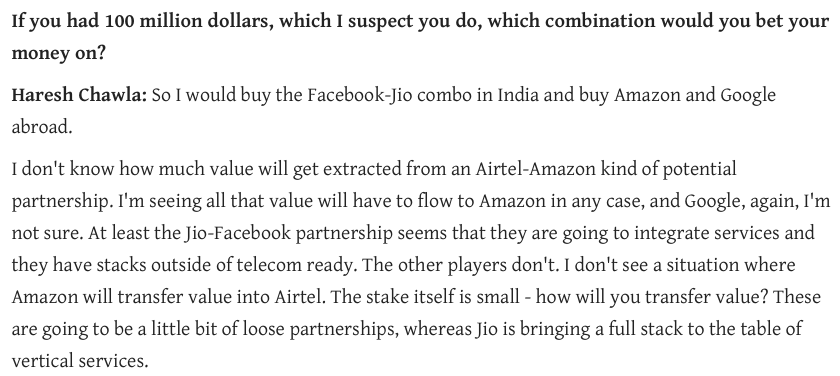

3 - Why are you assuming that these investors have no where else to go? Why invest during a global pandemic? There are enough pure play tech companies in India for them to burn money hand over fist like they have in the past. Facebook never does never minority deals - why did they value Jio at 2.5x the price they paid for WhatsApp? Jio’s user base (=WhatsApp in India), predictable and growing core telecom earnings, and ability to build / acquire the tech platform surely has value? When we think tech we are only looking at Jio’s consumer apps but what about their ability to service Indian businesses through broadband + enterprise apps (Microsoft) + data centers? Just look at FB - their value today is driven by Instagram and WhatsApp neither of which were built by FB.

If a newly debt free Reliance dominating multiple sectors, priced at <25 earnings, where the promoter is putting in 25,000 cr alongside the best set of institutional money in the world is “hype”, then I don’t know which Indian stocks are investable! There are much better reasons to reject Reliance like petrochemical weakness or ethical issues but in a market where much weaker companies are valued 2x - 3x higher I wouldn’t say Reliance is hyped at these levels.

Disc - invested & biased

I agree with what @zygo23554 mentioned on tech platform. What Jio has currently is collection of 100 apps only few of which are successful (JioSaavn, BookMyShow etc). With almost zero cross platform data exchange and use. Yes Jio has been very successful telecom company and will surely be able to leverage wireless data + broadband + enterprise servers.

And market is correctly valuing them as largest telecom + retail + legacy petrochem business. But don’t believe all the jargon on tech platform. It’s just not in DNA of RIL and creating and monetizing one is not same as creating Jio with 3.5L cr investment.

Tell me one innovation / disruptive app on technology side that RIL has created successfully in last few years? They have bought a few like BookMyShow and Saavn. Buying stakes in bunch of apps is PE investing not a tech platform.

My experience was different though. I ordered a few things from a Tier-2 city and got the things delivered on the same day evening. Amazon pantry sourced the products from nearby Tier-1 city and delivered 2 days later. I had the same experience with Reliance digital. Both Jiomart and RDigital range of products is small compared to Amazon.

Difference of opinion is always welcome, else we all risk living in an echo chamber. We would rather have our thought process questioned/taken apart by a fellow investor rather than by the market (very costly) ![]()

That said, I don’t think we have opposite views here - in fact I do not have a view on RIL at all. My knowledge and understanding of how tech platforms are built and scaled up is not up to the mark, it will take quite a bit of ground work to be able to comment on the probability of success of the Jio platform. Since I don’t understand the business well in the first place, me offering views on valuation would be useless.

I have no doubt that Jio will be a leading player (if not the leading player) in the years to come when it comes to telecom, broadband services and user base. They may do well in the retail business too. However, what I do know is this - building a tech platform off which an ecosystem of apps/data exchange is built is different from building a good telecom user base. It calls for a different kind of vision (mostly forward looking) on how consumer behavior could evolve over time and how does one build a tech stack that is robust enough and flexible enough to be integrated into this experience. The big telecom players in the US had a big captive user base too but none of them were able to monetize that the way new age companies were able to. While the attraction of “owning the infrastructure that drives data consumption of any sort in India” is no doubt there, this thesis is much more prone to disruption than other brick & mortar businesses that RIL has been running so far.

The skeptic in me just wants to point out that there aren’t too many voices out there that are asking some of these questions. I would want to understand certain things well enough before making up my mind on whether the hype is justified. Creating an ecosystem that can become the backbone of most data/commerce services takes a high level of skill and constant calibration, these might have to be brought in externally if they aren’t present in the current lot. In a business segment that is constantly evolving/getting disrupted, front loading heavy investments can hurt if the execution is not spot on. What if all investments are made over the next 2-3 years and unit economics change for the worse after 5 years for whatever reason?

Going by the media hype, RIL dominating digital consumption in India for the next decade appears to be a given. What if this narrative does not turn out to be accurate? They may dominate telecom and the data consumption infra but what if they get the monetization model wrong? What if the regulator steps in and prevents RIL from monetizing this to the extent possible?

Once again, I do not have a view on this - this is surely not my area of strength. I am just pointing out that there are many perspectives and possibilities to consider before buying into the prevalent media narrative

Hey, I agree to your view points, just one thought to add. Maybe you already have that in perspective but wanted to bring it to the fore. FB when invested in Jio platforms did invest in a pure play tech company. Their 100% capital went into a pure digital tech firm, the one of its kind, in a growing market like India. I wish as a minority investor, i had that tremendous opportunity. While, we as RIL investors have our capital distributed. Curious to know what is your current rationale to remain invested in RIL - is it the digital part or retail or both of these or the entire RIL as a whole? Thanks

I think it’s best to be invested at the same level where the promoters are. Right now Jio is basically a telecom firm and the digital platform comes from combining different parts of RIL. In future if they are separately listed and you want to avoid a holdco discount situation, it may make sense to be directly invested only in Jio or Retail

RIL partly paid-up shares will list on Monday(June 15,2020).

NSE Circular:https://archives.nseindia.com/content/circulars/CML44626.pdf

BSE:https://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20200612-1

Re: Execution, my best guesstimate is that Reliance will follow the strategy of

Currently the default Internet connectivity is through wireless and high speed wired connectivity is limited to certain parts of metros. Wireless infra is not capable of handling large volume of HD data content. This interview gives a good idea of recent trends. Talking Point With Former Bharti Airtel India CEO Sanjay Kapoor - YouTube

Converting premium users from D2H / Cable to fibre internet for daily video consumption (News, Sports etc). The demand for TV shows, Movies, Music is anyways shifting to On Demand play / subscription model instead of scheduled runs. The premium segment is where most of the value lies esp in capacity to pay. Fibre also has inherent advantages such as no cuts in rains, ability to handle interactive content and fungible with usage on other media like Mobiles, Laptops through routers. If there are 2-3 TVs in a house, you don’t need 2-3 Fibre connections.

Bundling of services in Jio Prime. Disney is an aggressive partner with everyone for bundling and Jio-Hostar bundling is already available.

Yesterday I saw an article which said Jio has also started offering bundled package of Amazon Prime with Jio Fibre

One would ask the question that why would a Disney or a Amazon want to bundle itself with Jio, esp in the long run. My answer to that is in the long run, it is very unlikely that an average user would pay for 4-5 OTT subscriptions at the same time. For eg: most young men would chose a Hotstar (for sports) and a year long subscription of Netflix/ Amazon prime. Very few would subscribe throughout the year to the likes of Zee, Alt Balaji etc. But for the OTT, bundling ensures that subscription is guaranteed for a longer period, a situation akin to a hotel pre-selling it’s inventory a year in advance at cheap prices to regular customers like airlines and corporates.

Not to forget, they can also bundle some other apps like Jio Saavn, Jio Cinemas, Jio Mart Preferncial access, Jio cloud etc.

Upto this stage, Reliance may not face big roadblocks in execution.

Paralelly they will try to grow Jiomart into a grocery retail delivery business. This is the big unknown where they will have to compete against established players and strong models like that of Dmart. Another point is how much cash can a listed company burn with investors to satisfy with every quarter numbers.

In terms of a Revenue model, one can’t expect purely a rise in Arpus or augmentation of revenues from bundling or Jio Mart to drive a revenue CAGR of 15-20% pa sustainably for long periods of time. Even if the partnership with Whatsapp is successful, the revenue potential of Whatsapp is far higher than that of Jio. The next logical step would be to be a payment gateway, but that’s a space which is extremely competitive and facing regulatory headwinds on pricing.

Hence at the moment, an investment in Reliance right know is a play on the trigger of Jio being a master services aggregator with an Optionality trigger of Jio Mart or Jio Payments being successful.

Execution capability can perhaps be considered as untested in the latter two.