I do apologise beforehand as this is not a super detailed DD. I

I found an interesting company by the name of Rico Autos and decided to write down my first thoughts out.

Rico Auto Industries Ltd.

Website BSE: 520008 NSE : RICOAUTO

Sector - Auto Ancillaries | Gruesome, Cyclical business.

Elevator Pitch - Slump in auto cycle, cheap valuations, depressed margins and ROCE which can turn up disproportionately.

Business Overview

- We manufacture and supply world class high precision and fully machined components & assemblies - both Aluminum and Ferrous - to leading OEMs across the Globe for Electric Vehicles, Electrified Vehicles and ICE Engines.

- Our multiple, flexible, fully integrated production facilities are equipped to offer a complete spectrum of services from Designing to Development of Tools, Casting and Precision Machining and Assembly of Components. Thus making us a Preferred Supplier to the EV & Hybrid Vehicle Market.

- Aluminum casting, Ferrous casting, Machine and assembly, Dies and molds, Engineering and R&D.

- The company began supplying EV businesses in 2019. Well poised to take advantage of the EV trend. From 2021 AR -

Variant Perception

- Currently the autos are in a downcycle, we might be poised for a cyclical uptick, with valuations cheap and market at a trough a clear upside can be capitalized upon.

- Eventual stabilization in RM prices, leading to better margins

- Margins should reach 11-12% a 400 bps point increase for about 3-5 quarters out from here.

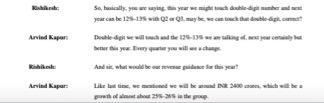

- A revenue guidance, on a conservative basis of 2400 crores from 1860 crores from FY22.

- Valuations at a cyclical low as it trades with a market cap of 711 crores. Once margins hit 11-12%, a 0.5x P/S is not unreasonable.

- Currently business does a ROCE of 6%(Taking CE of Gross block + NWC) which can rise as per my estimates to 12% on the back of higher sales/capital employed and OPM.

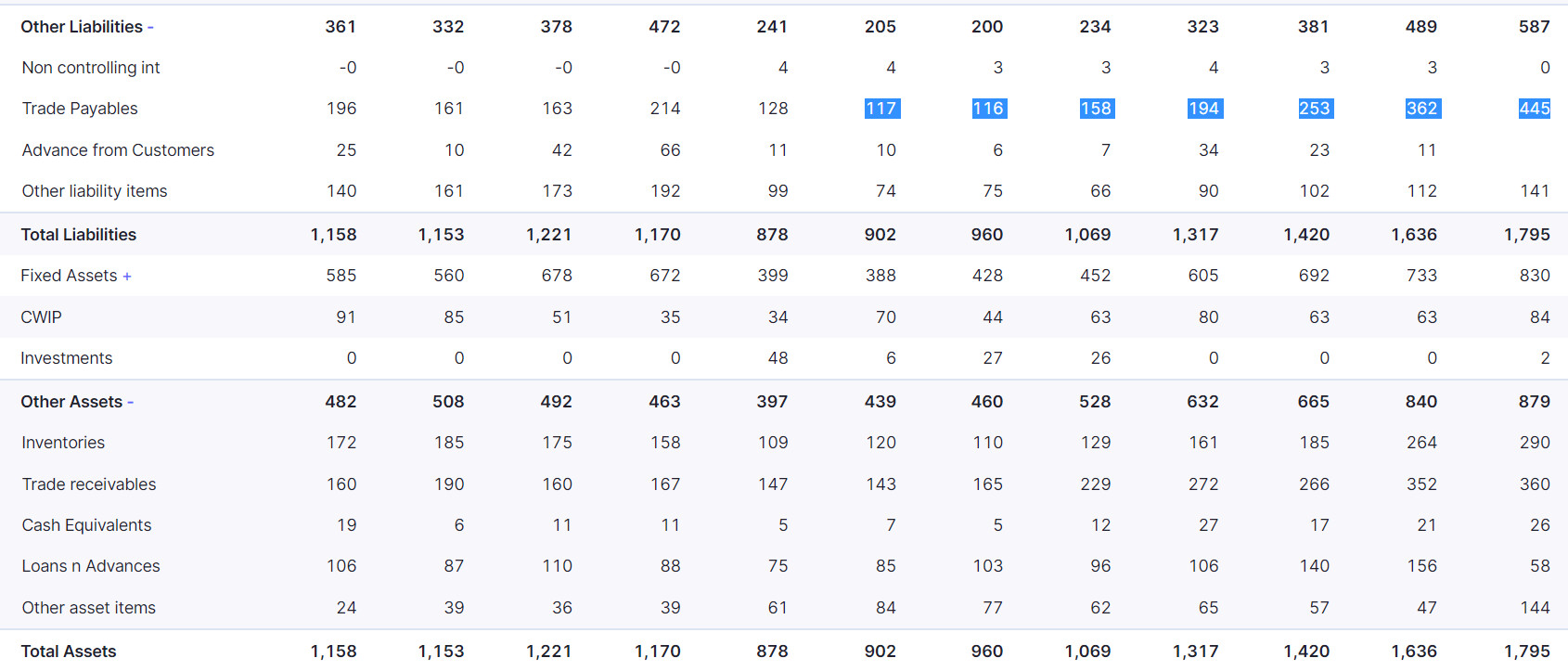

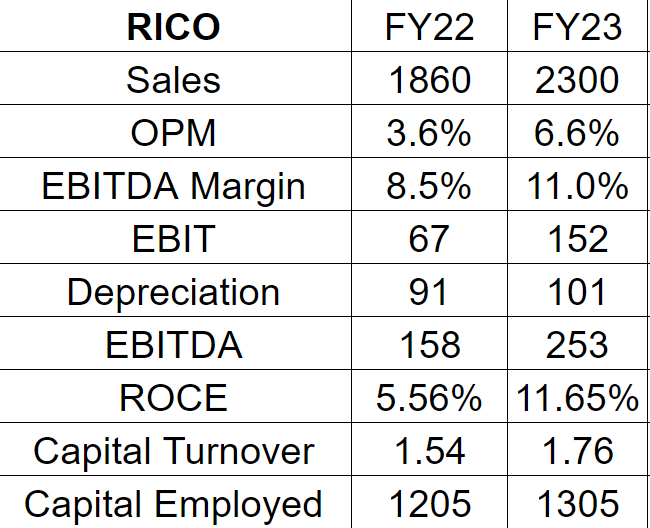

Numbers

The 2nd is my rough estimate of where ROCE’s can head from here.

Business trades 0.3x P/S which I believe is undervalued.

Risks

- Company is suscepitble to RM costs(which is the reason for stressed margins). Commodity prices may remain elevated which can lead to bad margins and low ROCE.

- Business is highly cyclical in nature as end users are Auto OEMs which are dependent on the auto cycle of India.

- Company makes most of its revenue from a few big clients such as TVS, Hero etc. Like other auto component suppliers it is susceptible to losing a client which can make visible dent in revenues.

- It is a small cap business with 0 institutional holding. While this is not a business risk, it does mean that the demand for the stock may be low.

- Company has a Debt profile of 400+ crores which while can be maintained, still poses a minor risk. Interest and depreciation are large cuts in the P&L here.

- Low ROCE, gruesome business, if the auto cycle goes worse company will be in tough liquidity position.

- An element of NPM deleveraging not due to unit econ of the business but moreso due to the high Interest and Depreciation costs, a small drop in OPM can magnify the drop in NPM.

Disc - No holdings.