Just wondering, if somebody had a chance to look at Revathi Equipment, one of the companies of Renaisance Group. Seems to be on a turnaround path with improving returns. Operates in the niche drilling equipment market with Coal India as one of the customers.

Couple of things that are worth nothing about Revathi

1). TheRenaisance Group(Abhishek Dalmia) bought 40% of the companyand another 20% from thepublic in 2004. Since then they have increased the networth ofthe company from 87cr to 131cr.

2). The company fundamentals have improved both in terms of EBITDA Margins and PAT margins with 2009 as the worst year.

3). ROE, ROA have significantly improved as well over the last 2 years, as well as flow ratios have improved as well.

4). Trades at a PE of 3.45x and EV/EBITDA of 3x (consolidated) level.

5). Trades at near book value

Now the negatives -

1.beaten down as it is in the EPC construction and mining sector.

2). The company has gotten into real estate which always makes me uncomfortable

3). Don’t have data from before 2005 to see how the company had done before the Renaisnce group acquired it.

Am still researching about the company business, comments welcome !! Also, anybody who can work out the numbers (can’t seem to find data before 2005) would be helpful, so we can compare.

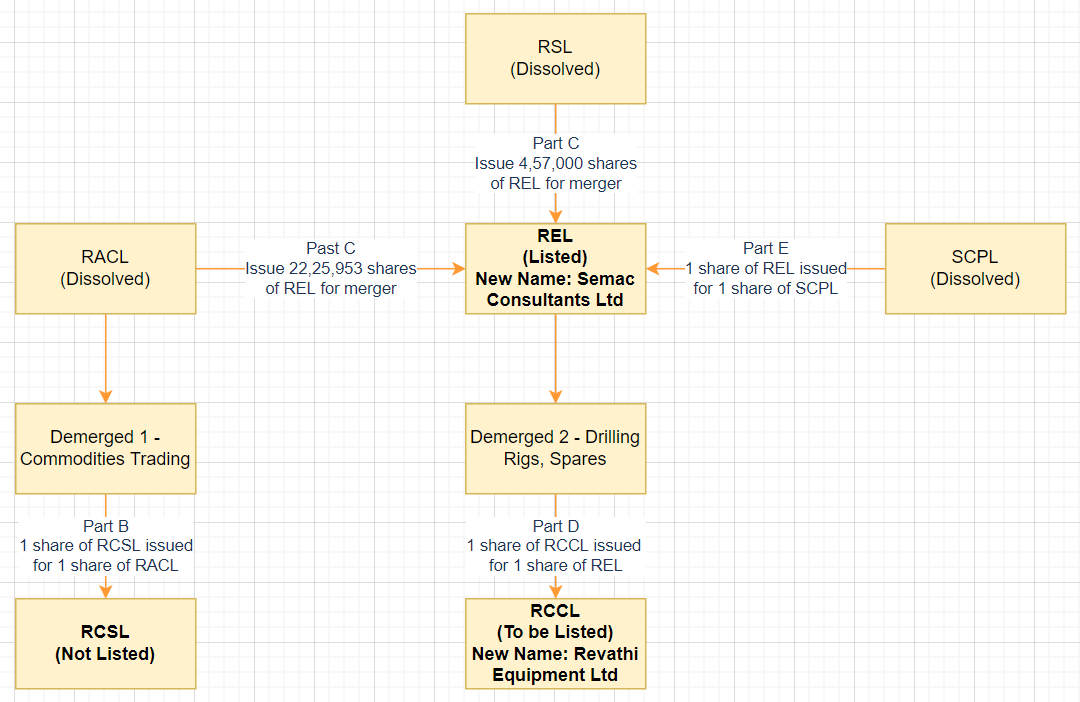

A demerger, merger Scheme happening in Revathi Equipment,

Shareholding Pre and Post Scheme - Link:

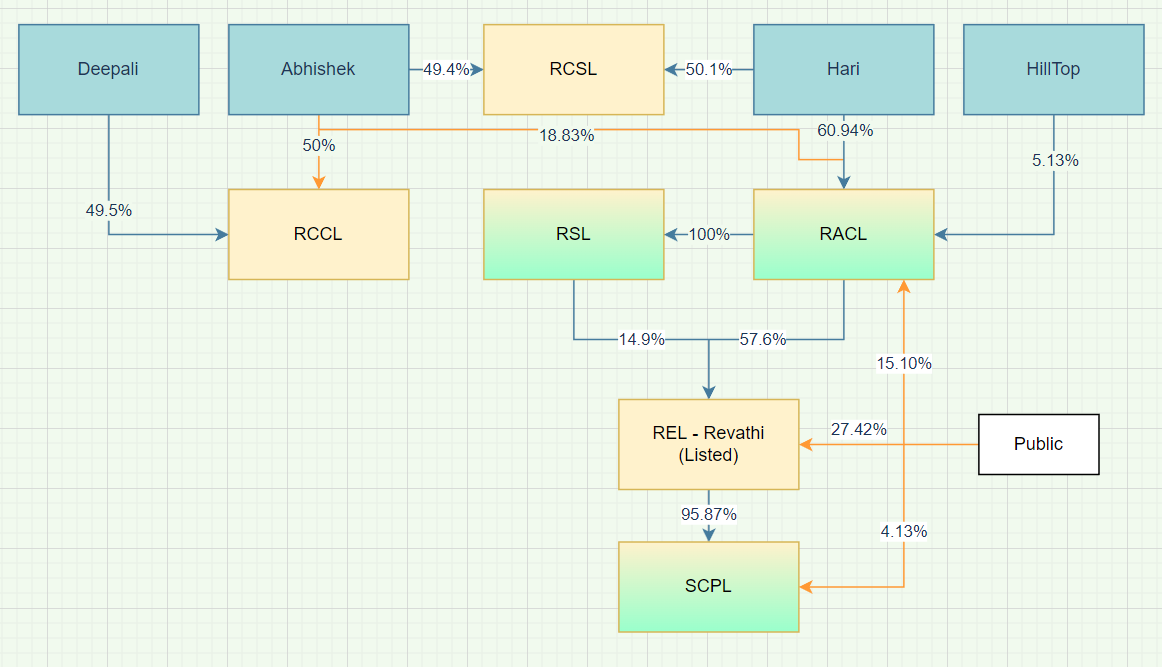

Shareholding Before Scheme:

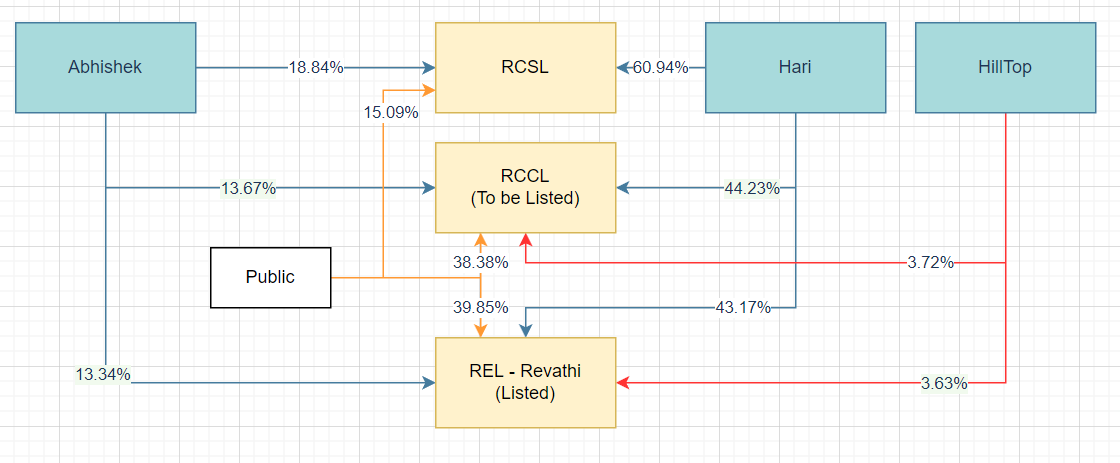

Shareholding After Scheme:

Merger- Demerger Visualization:

This is a complex Scheme and might take >12 months to complete with the listing of RCCL. RCSL its not mentioned it will be listed. Hope the company gives a better picture on this Scheme with their own details.

6 Likes

Hi Ashwin, thanks a lot. The structure pre and post was quite complex to understand at once.

I understand that you are actively tracking Revathi, wanted to know whether you find some arbitrage here or growth opportunity post the demerger. I started reading their AR, they are expecting good growth going forward. Would love to know about your view

Tough to say. Abhishek Dalmia takeover of Revathi 15+yrs back had a lot of promises, but none has fructified. Most ARs seem to convey information that are not in sync with Actual info, so will base my opinion on actual past performance. Engineering Design services i.e. SEMAC, since that bought has not really grown much. Go abck 10 odd years when they purchased it and compare to last year performance. You might find more slips from the company. Need to be cautious on this one, i am not betting big on the demerger, just a tracking position.

1 Like

Looks like AGM is kept in outskirts of Coimbatore (Physical). No VC AGM this year.

Snippets from AR 23- Porter Gyaan

Chairman speech says PAT of 32 Crs this year whereas consol PAT is 19 Crs. Looks like they are running parallel books of accounts. Guidance of 15% ROCE with 15% earnings growth

1 Like

Is anyone tracking this comapny? They recently got listed again as seperate drill business (Demerged from semac) and numbers looks quite interesting with good margin expansion.

1 Like