The thing is discussing/analyzing each other’s retirement planning gives new perspective to implement them in our own planning. I was entering the retirement data in an Excel based model and was flabbergasted to know the end result.

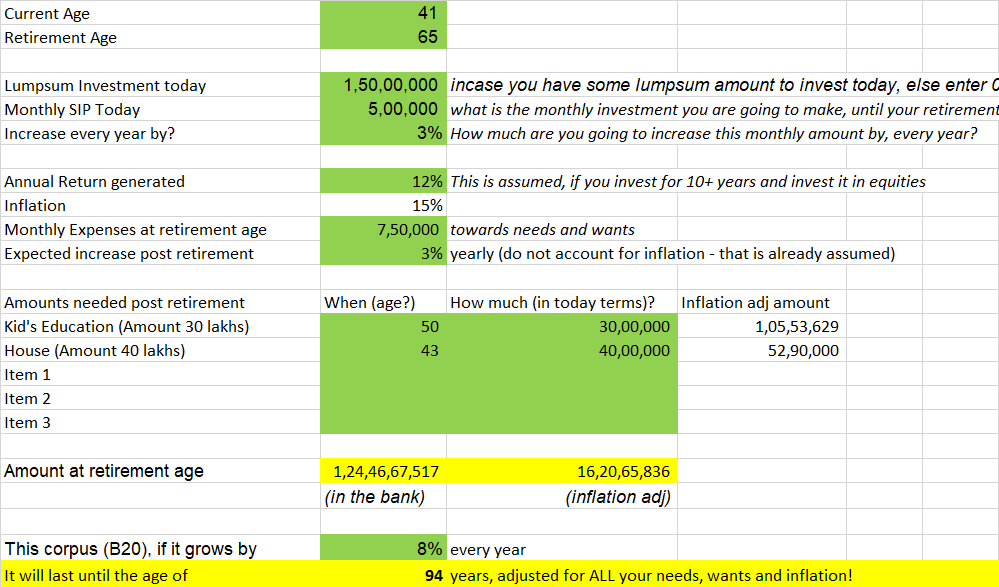

Here is my the data:

Logic for few data:

Inflation I have taken as 15%. As per RBI it is 6%, but any family man knows that it is 10% to 12% since last 10 years. Infact for medical, real estate, education it is around 20% and more.

I have taken monthly expense at age of retirement (25 yrs from now) as 7.5 lakhs. This is equal to today’s Rs 40,000 monthly expense compounded with 15%. (Plz dont tell me 40k is big monthly expense amount)

Post retirement, investment portfolio should be of debt so taken 8% return.

What I am really surprised is that inspite of fairly ok savings and considerable amount of SIP every month, I would JUST be able to make the investment corpus enough for my life expectancy of 95 years!! I dont think I have exaggerated myself as one with lavish lifestyle. All the input parameters are of middle class family. And other returns assumptions are also average I think.

Any thoughts/suggestions??